Divorce after 50, often called gray divorce, has moved from a cultural curiosity to a measurable retirement risk. In these cases, shared assets are split in half, joint claiming strategies dissolve, and the runway to rebuild before retirement shrinks. With this in mind, new survey data quantifies something most households avoid thinking about.

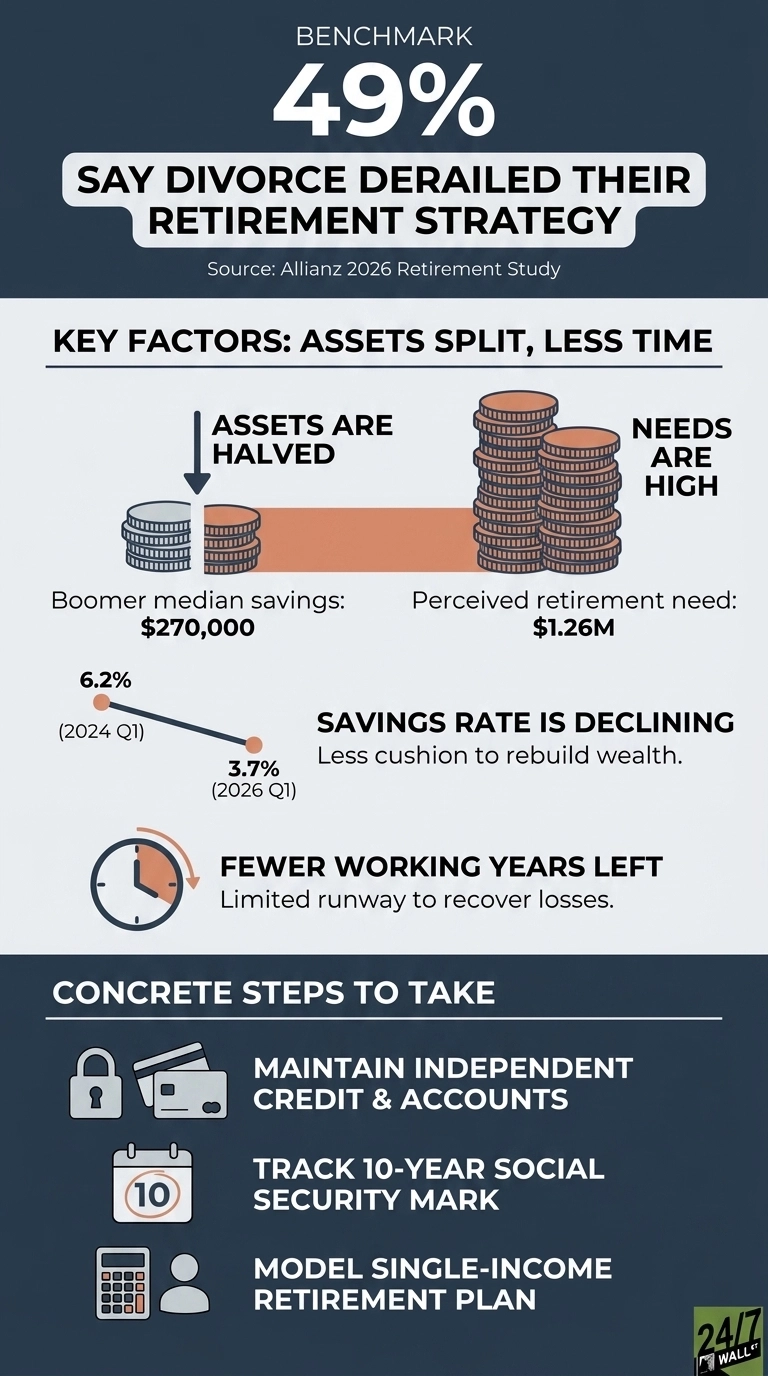

According to the Allianz Center for the Future of Retirement 2026 Annual Retirement Study, 49% of Americans who have gone through a divorce say it derailed their retirement strategy. Among those still married, 59% believe a divorce would seriously impact their ability to retire as planned.

The study surveyed 1,000 individuals aged 25 and older with household income of $50,000 or more (single) or $75,000 or more (married), or investable assets of $150,000 or more, conducted in January 2026. The headline finding is direct: gray divorce is rising among Americans aged 65 and older.

Why The Timing Is The Real Problem

A divorce at 60 carries structural financial consequences that a divorce at 35 typically does not. The Allianz framing captures it: “Shared assets, joint retirement strategies, and fewer working years to rebuild make gray divorce uniquely disruptive. For many, it’s not just an emotional shift but a major financial detour.” The underlying figures bear out that framing.

Start with the asset base: Fidelity’s Q3 2025 retirement analysis put the average Baby Boomer 401(k) balance at $267,900, and the median household retirement savings at $270,000 for Boomers in the Transamerica survey. Split that balance in a divorce, and each side walks away with roughly half. Northwestern Mutual’s 2025 Planning & Progress Study found Americans believe they need $1.26 million to retire comfortably, with Gen X estimating $1.57 million. The gap between a halved balance and the perceived target is sizable.

The Joint Strategy Unwinds Too

Asset division is the visible piece. The less visible part is the unwinding of every joint plan built around two people staying together. Social Security claiming strategies built around one spouse delaying to 70 while the other claims earlier collapse, as survivor benefit calculations change. Pension elections that assumed a joint-and-survivor payout may no longer apply. Housing costs that were shared are duplicated.

Social Security’s own protections have limits. A divorced spouse can claim on an ex’s record, but the marriage must have lasted 10 years or longer, and the claimant must be unmarried at the time. For couples who split before that threshold, the spousal benefit disappears entirely.

A Thinner Cushion To Land On

The broader savings picture makes rebuilding harder. The U.S. personal savings rate has fallen from 6.2% in the first quarter of 2024 to 3.7% in the first quarter of 2026. Per capita disposable income is $68,359, and the University of Michigan consumer sentiment index registered 49.8 in April 2026, a level the index treats as recessionary. The cushion that would help someone in their late 50s rebuild after a divorce is thinner than it was two years ago.

Inflation, even at a moderate 2.1% annual pace, compounds against fixed retirement income. For a newly single 62-year-old splitting a $270,000 balance, the post-divorce portfolio must cover the same lifespan with half the principal and none of the economies of scale that came with sharing a roof.

Planning For The Scenario Nobody Wants To Model

Most retirement plans assume the marriage holds. The Allianz data suggests that assumption deserves a stress test. Allianz notes that financial professionals can help clients build retirement strategies that account for unexpected changes, including separation, by offering guidance on asset division, retirement account adjustments, and rebuilding a financial foundation after a split.

A few practical considerations follow from the data. Keep an independent credit history and at least one retirement account in each spouse’s name, which, given the IRA limits of $7,500 for 2026, makes this approach accessible to most households. Track the 10-year marriage threshold for Social Security spousal eligibility before any separation decision is finalized. Model the retirement number on a single-income basis at least once, even in a stable marriage, so the gap between a joint plan and a solo plan is visible before it must be lived.

Gray divorce is rare relative to the broader population, but the financial fallout is concentrated and severe. The data documents what happens when a retirement plan built for two must work for one.

Contact [email protected] for any questions or corrections.