Retirement is a goal most Americans share, but reaching it comfortably requires planning that starts long before you hand in your badge. Finance expert Suze Orman has spent decades distilling that planning into actionable guidance. Here are the six principles she returns to most often.

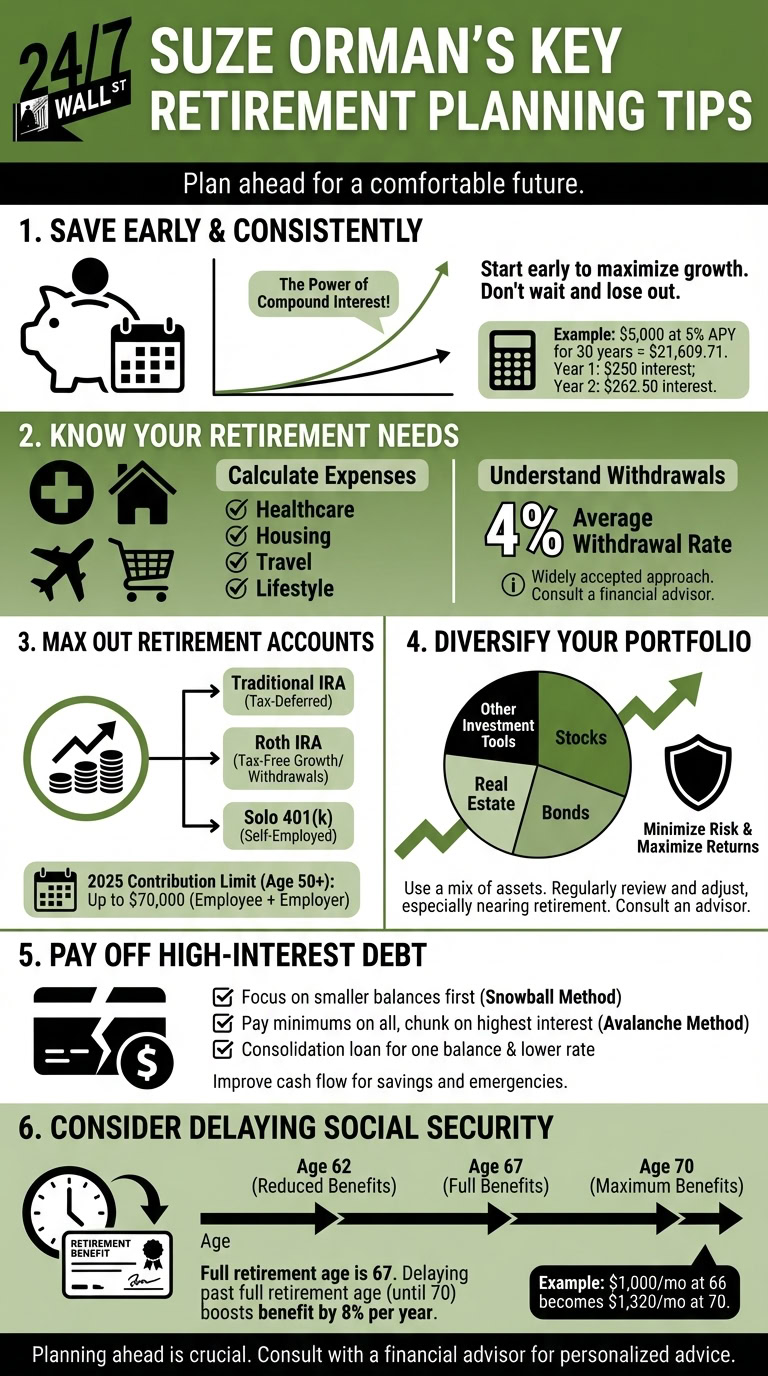

No. 1: Save Early and Consistently

The single most powerful tool available to retirement savers is compound interest, and it only works if you give it time. Every year you delay getting serious about saving is a year that compounding cannot work in your favor.

Consider a simple example: put $5,000 into a savings account earning 5% annually, and in year one you collect $250, leaving you with $5,250. In year two, that same 5% now applies to the larger balance, netting $262.50. The growth accelerates from there. Leave the original $5,000 untouched for 30 years at that same rate, and the account grows to $21,609.71 without a single additional deposit. Starting early turns modest contributions into a significant nest egg over time.

Orman’s broader message is consistent: as she wrote in a 2025 post on her website, “The earlier you start, the better prepared you’ll be to enjoy the retirement you deserve.”

No. 2: Know Your Retirement Needs

Your spending in retirement depends entirely on how you plan to live. A globetrotting retirement looks very different on paper than one spent close to home. Whatever vision you have, projecting those costs realistically is the essential first step.

One widely used starting point is the 4% annual withdrawal rule. The idea is that drawing no more than 4% of your portfolio each year gives you a high probability of not outliving your savings. That figure is a helpful baseline, but individual circumstances vary, so consulting with a financial advisor before committing to any withdrawal strategy is strongly recommended.

No. 3: Max Out Your Retirement Account Contributions

Tax-advantaged accounts are among the most efficient vehicles for building retirement wealth. A traditional Individual Retirement Account (IRA) lets you invest on a tax-deferred basis, and contributions are often deductible from your taxable income. A Roth IRA works in reverse: contributions come from after-tax dollars, but growth and qualified withdrawals are tax-free. Your financial advisor can help you weigh which structure fits your situation best.

For the self-employed, the Solo 401(k) offers especially generous limits. In 2025, the combined employee-plus-employer contribution cap sits at $70,000 for those under 50. Savers aged 50 to 59 or 64 and older can add a $7,500 catch-up contribution, pushing their ceiling to $77,500. Participants aged 60 to 63 benefit from a higher “super catch-up” of $11,250 under SECURE 2.0, raising their total to $81,250. For 2026, the base cap rises to $72,000, with the standard catch-up increasing to $8,000 for those 50 and older. Orman’s core advice on this front is straightforward: maximize these accounts before directing money elsewhere.

Even if you have access to a workplace 401(k), Orman recommends the Roth option when available. As she has said publicly, contributing just enough to a traditional 401(k) to capture any employer match, then directing additional retirement savings into a Roth IRA, is a tax-smart combination worth considering.

No. 4: Diversify Your Portfolio

Spreading your investments across multiple asset classes is how you reduce the risk that any single holding derails your retirement timeline. Orman recommends blending stocks, bonds, and other assets such as real estate to smooth out volatility over the long run. Stocks provide the growth needed to outpace inflation; bonds offer stability when markets swing. The right balance shifts as retirement draws closer, which is why Orman consistently urges savers to revisit their allocation regularly and to work with a financial advisor as the target date approaches.

No. 5: Pay Off High-Interest Debt

Carrying a credit card balance into retirement is a serious financial hazard. Interest rates on revolving credit card debt frequently exceed 20%, and Orman has noted that paying that kind of interest while trying to live on fixed income creates a significant and unnecessary burden. The goal is to enter retirement debt-free, or as close to it as possible.

Three approaches can help. First, tackle the smallest balances first. Eliminating them frees up cash flow that can then be redirected toward the larger, higher-rate balances. Second, make minimum payments on all accounts while putting every available dollar toward the balance with the highest interest rate. Third, consider a debt consolidation loan to roll multiple balances into one, which can simplify repayment and may free up room to start building an emergency fund.

On the emergency fund front, Orman is notably conservative: she recommends keeping eight months of living expenses in a dedicated savings account, separate from checking. That buffer protects retirement investments from having to be tapped during an unexpected financial setback.

No. 6: Consider Delaying Social Security

For anyone born in 1960 or later, full retirement age (FRA) is 67. Claiming at exactly that age locks in your standard benefit. Waiting longer is where the real upside lies. According to the Social Security Administration, benefits grow by approximately 8% for each full year you delay past FRA, up to age 70. For a retiree with an FRA of 67 who waits until 70, that translates to a 24% larger monthly check for life.

Orman has long advocated for delaying Social Security as a cornerstone of retirement income planning. Her more recent guidance, however, acknowledges that working until 70 is not realistic for everyone. If stopping work in your early or mid-60s makes sense for your situation, she now suggests a “bridge strategy”: draw from IRA or 401(k) assets in those early retirement years specifically to avoid tapping Social Security early, preserving the larger future benefit. A part-time income in those years can reduce how much you need to withdraw from savings during the bridge period.

One firm rule: do not delay past 70. The 8% annual credit stops accruing at that point, so there is no financial reason to wait any longer. On the other end of the spectrum, claiming as early as age 62 permanently reduces your monthly benefit, a reduction that compounds over a long retirement.

Editor’s note: This article was updated to correct the 2025 Solo 401(k) contribution limits, clarifying that the $70,000 base cap applies to all participants and that savers aged 50 and older can contribute up to $77,500 (or $81,250 for those aged 60 to 63 under SECURE 2.0 rules), with 2026 figures also added. The Social Security section was revised to reflect the FRA of 67 for those born in 1960 or later, note the accurate 24% total benefit boost from delaying to age 70, and incorporate Orman’s more recent “bridge strategy” guidance on using retirement savings to delay Social Security even after leaving the workforce.