Palo Alto Networks (PANW): Q3 FY25 Earnings LIVE

Live Updates

Next Quarter Guidance

| Metric | Guidance | YoY Growth |

|---|---|---|

| Revenue | $2.49B – $2.51B | +14% – +15% |

| Non-GAAP EPS | $0.87 – $0.89 | ~+10% |

| Next-Gen Security ARR | $5.52B – $5.57B | +31% – +32% |

| Remaining Performance Obligation (RPO) | $15.2B – $15.3B | +19% – +20% |

-

Revenue guide is strong and consistent with historical trends — shows confidence in deal execution post-Q3.

-

EPS guide is solid, but lower than this quarter’s $2.79 — likely due to timing of deals, higher SBC (share-based comp), or investment cadence.

-

RPO and Next-Gen Security ARR both point to sustained multiyear commitments, especially in Prisma and Cortex products.

Valuation anchored

After this report, PANW is trading at roughly 35x FY25 EPS, near the median of large-cap security peers. The Street rewarded the beat, but the stock’s muted after-hours response shows that execution isn’t the issue — conviction in the long-term model is.

To break out of this reset valuation range, Palo Alto needs to deliver more than revenue and RPO strength. It needs accelerating billings and confidence that platform wins (especially in SASE and SOC automation) will materially bend the top line and margins.

PANW Cleared the bar — but didn't raise it

With billings up just 3% YoY and guidance implying steady rather than accelerating growth, PANW cleared the lowered expectations bar — but didn’t raise it. This may keep the stock rangebound until next-gen ARR gains translate into visible margin leverage or top-line acceleration.

Full-year revenue guidance was nudged slightly higher to $10.15B–$10.18B, and EPS guidance was reaffirmed at $13.77–$13.80. That’s a positive signal after February’s surprise reset — but for many investors, it’s still not enough.

Earnings snapshot

Key metrics from just released earnings report:

| Metric | Q3 FY25 | YoY Change |

|---|---|---|

| Revenue | $2.87B | +15% |

| Non-GAAP EPS | $2.79 | –2% approx. |

| RPO | $11.3B | +23% |

| Total Billings | $2.52B | +3% |

| Next-Gen Security ARR | $5.1B | +34% |

Cloud and AI Strategies Need More Monetization Detail

In prior quarters, Palo Alto emphasized Prisma Cloud, Cortex, and the broader consolidation thesis as key long-term growth levers. This quarter reinforced that messaging, but did little to quantify near-term monetization from AI-enhanced capabilities — an issue we flagged earlier today.

RPO strength shows customers are committing to long-term contracts, but investors want more visibility into immediate ARR impact from Cortex XSIAM and Prisma SASE. AI was mentioned frequently on the call, but similar to last quarter, the monetization path remains implied rather than measured.

For PANW to win back high-multiple support, the next 1–2 quarters will need to show more billings leverage tied to those AI-driven solutions. For now, execution was solid — but the bar for a breakout remains tied to deal velocity, not just deal size.

What is pushing the stock lower right now

This quarter offered a partial redemption for Palo Alto Networks following February’s surprise guidance cut. As previewed, analysts were braced for a rebound — and PANW delivered with better-than-expected revenue, EPS, and particularly RPO growth (+23%), which suggests multiyear deal momentum is intact.

That said, total billings growth of just 3% remains a sore spot. In our pre-earnings setup, we noted that deal timing and delayed conversion would remain critical areas to watch. Those concerns are only partially resolved, and the stock’s muted after-hours reaction reflects this mixed message: the platform strategy is working, but not accelerating as quickly as bulls had hoped.

Strong Beat, Soft Billings Guide Reignites Volatility Risk

Palo Alto Networks reported Q3 FY25 revenue of $2.87 billion, beating analyst estimates of $2.49 billion and representing a 15% YoY increase. Non-GAAP EPS came in at $2.79, also ahead of the $2.86 consensus but slightly down year over year, as expected due to deal timing and mix shifts. GAAP EPS was $1.32, in line with expectations.

The standout: Remaining Performance Obligations (RPO) grew 23% YoY to $11.3 billion, signaling strong demand. However, total billings rose just 3% YoY to $2.52 billion, a continuation of the slower near-term growth rate that rattled investors last quarter.

Management raised full-year revenue guidance to $10.15B–$10.18B, up slightly from prior estimates, and reaffirmed non-GAAP EPS of $13.77–$13.80. Shares were volatile after-hours as the market digested strong top-line results alongside continued softness in billings acceleration. Right now the stock is down 4.2% after-hours.

How the stock performed after recent earnings reports

| Quarter | EPS Actual | EPS Est. | Surprise | Stock Reaction |

|---|---|---|---|---|

| Q2 2025 | $1.75 | $2.05 | –$0.30 | –14.8% |

| Q1 2025 | $4.63 | $4.35 | +$0.28 | Flat/Modest Up |

| Q4 2024 | $3.64 | $3.31 | +$0.33 | +7.5% |

| Q3 2024 | $4.75 | $4.15 | +$0.60 | +6.9% |

Sentiment Still Divided

PANW’s sharp post-Q2 selloff (-15%) triggered a flood of analyst downgrades, but sentiment has slowly rebounded. The stock is now up over 20% from its lows, reflecting buy-the-dip optimism around long-term cybersecurity demand. However, institutional positioning remains mixed: short interest is modest at 2.7%, but options activity has skewed toward downside protection over the past two weeks, with elevated put volume near the $190–$200 strikes.

Analyst targets have narrowed: the median is $216, with bears anchored around $156 and bulls holding firm near $235. Revisions have trended slightly negative, with multiple brokers noting uncertainty around federal bookings cadence and AI monetization.

Rebuilding Credibility

On last quarter’s call, CEO Nikesh Arora took full responsibility for the guidance shock, stating PANW was “leaning into platformization” but “misread the timing.” The company emphasized its three-platform strategy (Strata, Prisma, Cortex) as the long-term growth engine but admitted customer consolidation is happening slower than expected.

Management walked back aggressive top-line expectations but leaned on NARR (Net Annual Recurring Revenue) growth and cloud security attach as medium-term validators. AI was name-dropped frequently — especially for SOC automation — but lacked direct monetization claims. Analysts pressed hard on billings visibility, and Arora’s tone was notably defensive but firm on the long-term roadmap.

“We still believe the transformation is necessary. But we may have pushed harder than the customer was ready for.”

Eyes on deal flow

Palo Alto’s February quarter reset raised major questions around the timing and visibility of federal and large enterprise deals. Management emphasized longer deal cycles but reaffirmed long-term billings strength. The company’s shift toward platform consolidation — combining cloud security, SASE, and threat detection — remains its core strategy, and any updates on Prisma Cloud or Cortex XSIAM adoption will be central to the bull case.

In recent investor commentary, PANW has pointed to AI as an accelerant for security operations, with emphasis on automated threat detection and response. However, investors will want clarity on how these tools are driving ARR or upsell velocity — not just demos. Expect focus on next-gen firewall momentum, renewals, and any traction from federal or international segments post-guidance cut.

Palo Alto Networks (NASDAQ: PANW | PANW Price Prediction) enters earnings up +21% over the past month and +7.5% year-to-date, reflecting renewed optimism following a surprise guidance reset last quarter. Analysts expect EPS of $1.32 GAAP / $2.86 non-GAAP on $2.49 billion in revenue, which would mark a 12% YoY decline in revenue and a near-40% drop in EPS compared to last year’s $4.75 blowout Q3.

The company has beaten EPS in 3 of the past 4 quarters but missed sharply last quarter, sending shares down –15%. FY25 EPS consensus is $13.72 (non-GAAP), slightly below FY24, and investors are focused on a second-half reacceleration. A soft quarter could reinforce bear concerns that AI-led cybersecurity tailwinds are overstated.

Cybersecurity in the Crosshairs of AI and Budget Cycles

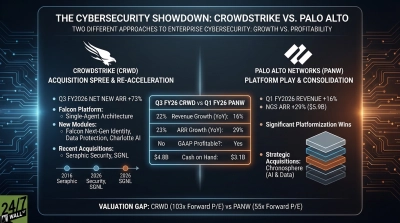

The cybersecurity sector continues to straddle two opposing forces: sustained long-term demand from cloud, AI, and zero-trust adoption, and near-term budget rationalization across enterprise and government customers. Peer results have been mixed — CrowdStrike beat and raised, Fortinet issued cautious commentary, and Zscaler warned of elongating deal cycles.

Palo Alto’s exposure to federal and large enterprise deals means it’s particularly sensitive to macro-driven delays. The broader security market remains in transition from platform consolidation (XDR, SASE) to AI-enhanced threat detection, and investors want clarity on whether those shifts are monetizing today or still aspirational.

Contact [email protected] for any questions or corrections.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 24/7 Wall Street