Micron Technology (NASDAQ:MU | MU Price Prediction) has emerged as a key player in the artificial intelligence (AI) ecosystem through its high-bandwidth memory (HBM) chips, which provide the high-speed data processing essential for training large language models and running inference tasks.

These chips enable AI accelerators from companies like Nvidia (NASDAQ:NVDA) to handle massive datasets efficiently, positioning MU as a vital supplier amid surging demand from data centers. In its fiscal Q4 earnings report last month, MU delivered revenue of $11.3 billion, up 46% year-over-year, with adjusted earnings of $3.03 per share beating estimates, and guidance for record Q1 2026 revenue of $12.5 billion.

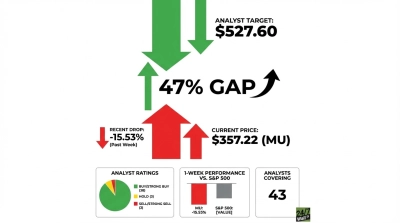

Yet, the stock dipped sharply afterward, falling over 7% in the days after, despite the upbeat results. Now, Wall Street is catching on. A wave of upgrades has hit, including Morgan Stanley‘s shift to overweight with a price target hike from $160 to $220 per share, and Itau BBA Securities just initiating coverage with an outperform rating and a $249 per share target — near the high end of industry estimates.

These follow boosts from firms like Rosenblatt, which raised its target to $250 per share, signaling broad recognition of MU’s AI-fueled potential.

Why MU’s AI Memory Edge Makes It a Must-Buy

Micron’s strength lies in its DRAM and HBM leadership, where AI demand is creating a supply crunch. HBM3E chips had been fully booked through 2025, but now with its HBM4 chips, which offer even greater performance, Micron is expecting to see greater growth and profit.

Data center revenue declined 22% year-over-year in Q4, even as its cloud memory business saw a massive threefold increase. The shift highlights a strategic change Micron undertook to focus on high-margin, high-performance memory for AI infrastructure, where spending is projected to exceed $200 billion annually by next year.

MU’s role in powering GPUs positions it for sustained growth as fiscal 2025 revenue hit $37.3 billion, a 49% jump. Management forecasts retaining its edge in HBM4 chips with any market losses occurring between its rivals in the space.

Undervalued Means Opportunity

At a forward P/E of just 10 and trading at a fraction of Wall Street’s earnings growth rate projections, MU trades below its peers despite faster EPS expansion. Analysts project earnings will double in fiscal 2026 to $16.59 per share.

Free cash flow more than doubled in Q4 to $803 million, helping to fund HBM capacity expansions without diluting shareholders. Compared to NVIDIA’s 52x P/E, MU’s valuation is overlooking its market dominance and geopolitical edge as the sole U.S.-based HBM producer, reducing tariff risks.

With consensus targets averaging $190 per share — implying modest 3% upside — analyst high-end forecasts at $250, the market is underpricing MU’s $59 billion 2026 revenue projection, a 43% increase. As management is looking for margins to exceed 50%, Micron presents investors with a compelling valuation.

Key Takeaway

Micron Technology stands out in the AI market with its HBM innovation, offering 30% better power efficiency and 50% higher capacity than rivals, making it indispensable for energy-hungry data centers. While Samsung and SK Hynix dominate with 60% combined share, MU’s 21% slice grows fastest, backed by U.S. manufacturing that dodges supply chain vulnerabilities.

True competition is limited — only these three scale HBM production amid $130 billion market forecasts by 2033. Buy MU for its undervalued growth as AI tailwinds mark it as a discount bin stock.

Contact [email protected] for any questions or corrections.