The AI gold rush has created winners and losers, but the market hasn’t fully sorted them yet. While everyone chases AI exposure, some household names are getting swept up in hype despite questionable positioning. These five stocks deserve scrutiny.

5. Salesforce (CRM): Software AI vs. Infrastructure Reality

Salesforce has woven AI into its CRM platform, promising productivity gains and automated workflows. The fundamentals look solid: 38.6% earnings growth year-over-year, 24% operating margins, and bullish analyst consensus.

But revenue grew just 8.6% year-over-year while earnings surged 38.6%. That gap screams margin expansion and share buybacks, not organic AI-driven growth. The company trades at 29x trailing earnings and 17x forward earnings, commanding a premium for AI features bolted onto existing software.

Salesforce benefits from AI as a productivity tool, but it’s not selling the picks and shovels. The stock has cratered 31% over the past year while the AI narrative supposedly strengthens. That’s the market telling you something about who actually captures AI economics.

4. Netflix (NFLX): Defensive Moves Disguised as Growth

Netflix reported earnings on January 20, beating estimates with $0.56 per share against expectations of $0.55. Revenue hit $12.05 billion, topping the $11.97 billion consensus. The company crossed 325 million global subscribers.

The stock fell 5% in after-hours trading.

Why? Lower-than-expected guidance for Q1 2026 and the full year. Netflix announced an $83 billion all-cash acquisition of Warner Bros. Discovery, a defensive play against subscription fatigue rather than an offensive AI move. The company is ceasing stock buybacks to fund the deal.

Netflix has no meaningful AI infrastructure business. Its AI applications are internal: recommendation algorithms and content optimization. Those are table stakes, not competitive moats. The Warner deal signals management sees consolidation as the path forward, not AI-driven expansion. Full-year 2025 EPS of $1.97 was flat compared to 2024’s $1.98.

3. Tesla (TSLA): Autonomy Promises, Profitability Problems

Tesla trades at 285x trailing earnings on $95.6 billion in revenue. The bull case rests entirely on Full Self-Driving and Optimus humanoid robots delivering massive future profits. The problem? Earnings declined 37% year-over-year while the stock commands a $1.4 trillion valuation.

Polymarket traders assign 48% probability to Tesla closing below $415 by January 23, with only 2% odds of breaking above $460. Gary Black, a prominent Tesla bull, recently noted FSD adoption rates remain disappointingly low despite years of promises.

The NHTSA has a February 23 deadline for a Full Self-Driving probe covering 2.9 million vehicles. Elon Musk just announced Tesla will restart the Dojo3 chip project after calling Dojo2 an “evolutionary dead end.” That’s iteration risk, not execution confidence. Meanwhile, Musk spent last week publicly feuding with Ryanair’s CEO about potentially buying the airline.

2. Apple (AAPL): Consumer AI, Not Infrastructure AI

Apple trades at 34x earnings with a $3.8 trillion market cap. The company generates massive profits: 27% net margins, 32% operating margins, and $416 billion in trailing revenue. But where’s the AI infrastructure play?

Apple’s AI story centers on on-device processing for iPhones, iPads, and Macs. That’s consumer AI, not the data center buildout driving NVIDIA’s 66% earnings growth. Apple doesn’t sell chips to other companies or operate cloud infrastructure at scale. It’s a beneficiary of AI consumption, not AI production.

The stock is down 9% year-to-date. Revenue growth of 8% doesn’t justify a 51x price-to-book ratio. If you believe AI infrastructure is where the money gets made, Apple is the wrong bet.

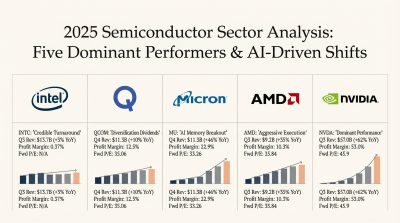

1. Intel (INTC): The Turnaround That Isn’t

Intel has surged 147% over the past year, climbing from $19.67 to $48.56. The turnaround narrative is seductive: foundry investments, CHIPS Act funding, sold-out server CPU capacity, and an Ohio fab showing “healthy progress.”

Look at the fundamentals. Intel trades at 809x trailing earnings. The company earned $0.06 per share in 2025, down from a $5.47 peak in 2021. That’s a 95% earnings collapse over four years. Operating margins sit at 6.3%, profit margins at 0.37%. Q3 2024 delivered a catastrophic $0.46 earnings miss.

Fast Company reported on January 20 that Intel has “scaled back its rhetoric on AI PCs, acknowledging that consumers are not as interested in these enhanced features as the company initially hoped.” The Ohio fabs won’t be operational until 2030-2031. Meanwhile, NVIDIA posted 33% gains over the past year with 107% ROE and 53% profit margins. AMD gained 96% with 60% earnings growth.

Analyst consensus? Thirty-three “Hold” ratings versus just five “Buy” ratings. The average price target of $42.44 implies downside from current levels. RBC Capital summarized it perfectly: “awaiting concrete evidence of gross margin improvements and successful foundry execution before adopting a more optimistic stance.”

Intel’s turnaround is a hope, not a reality. The stock has run 147% on promises while competitors deliver results.

The Real AI Winners

If you want AI exposure, follow the infrastructure. NVIDIA gained 1,224% over five years with a forward P/E of 24x. AMD’s PEG ratio of 0.50 suggests growth at a reasonable price. These companies sell the tools everyone needs.

The stocks above? They’re either late to AI, selling features instead of infrastructure, or running on hype that fundamentals don’t support. Sometimes the best investment decision is knowing what to avoid.

Contact [email protected] for any questions or corrections.