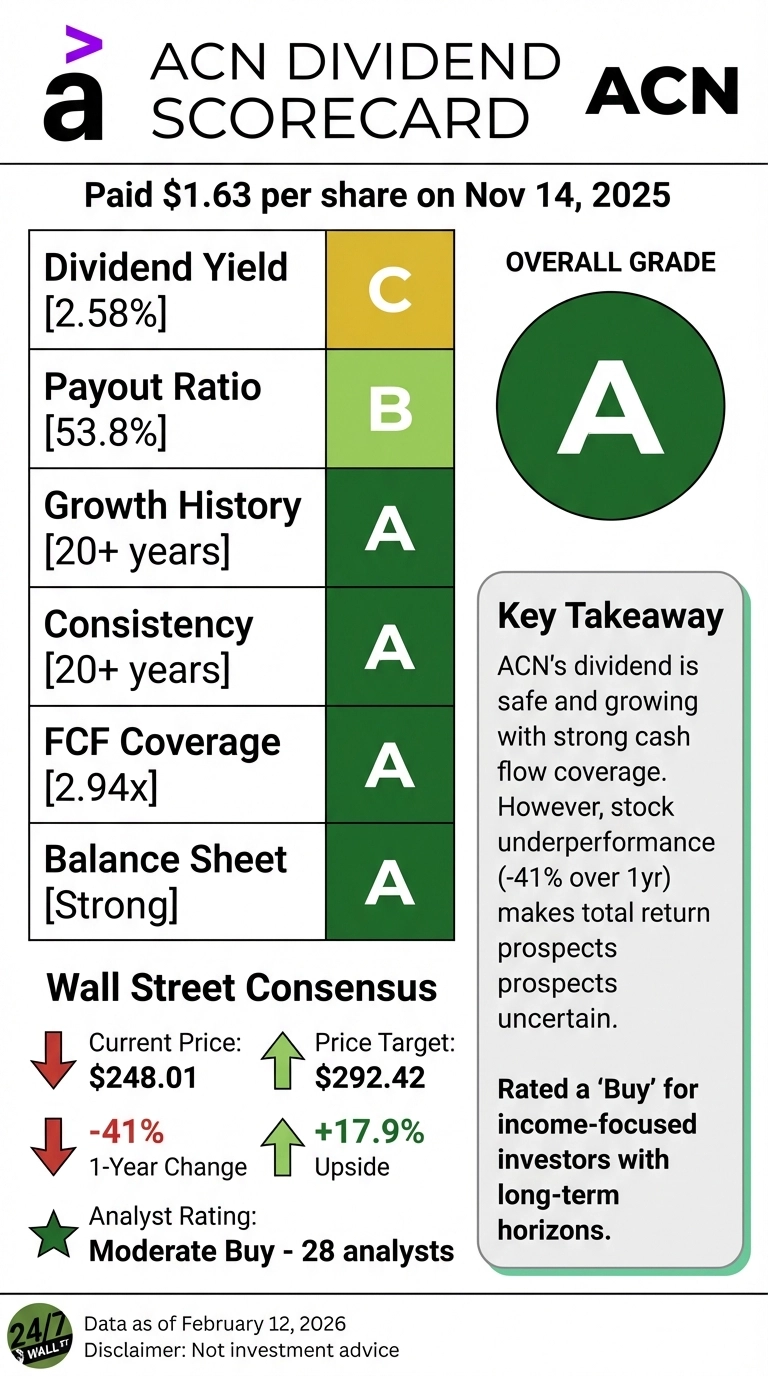

Accenture just paid shareholders $1.63 per share on February 13, 2026, marking the latest installment in a 20+ year streak of consecutive annual dividend increases. But with the stock down 41% over the past year and trading at $224.08, investors need to look beyond the growth streak to understand whether this 2.6% yielder still deserves a place in dividend portfolios.

The Dividend Growth Story Remains Intact

Accenture’s dividend trajectory tells a story of disciplined capital allocation. The consulting giant increased its quarterly payout from $1.48 to $1.63 starting in the third quarter of fiscal 2025, representing a 10.1% increase. On an annualized basis, shareholders now collect $6.22 per share, up from $5.54 the prior year-a 12.1% year-over-year increase.

The longer-term growth rates underscore the company’s commitment. Over five years, Accenture’s dividend has climbed 85.1%, and the 10-year growth rate stands at an impressive 510.8%. This consistency matters: Accenture has raised its dividend every year for more than two decades, placing it among the technology sector’s most reliable income generators.

Cash Flow Coverage Provides Substantial Safety Margin

The sustainability of Accenture’s dividend rests on robust cash generation. In fiscal 2025, the company produced $11.47 billion in operating cash flow, up from $9.13 billion the prior year. After subtracting $600 million in capital expenditures, free cash flow reached $10.87 billion.

Against total dividend payments of $3.70 billion, Accenture’s free cash flow covered the dividend 2.94 times, providing a comfortable cushion that leaves ample room for dividend growth even if business conditions soften. The company’s capital intensity remains low, with capex consuming just 5.2% of operating cash flow, a characteristic that distinguishes professional services firms from capital-heavy industrials.

The traditional payout ratio tells a similar story. With trailing twelve-month earnings of $11.57 per share and an annualized dividend of $6.22, Accenture’s payout ratio sits at 53.8%-well below the 60-70% threshold that typically signals limited room for growth. For context, IBM pays out 60.2% of earnings as dividends while growing its payout at just 3.6% annually over the past decade.

The Valuation Disconnect

Here’s where Accenture’s dividend story gets complicated. The stock trades at 20 times trailing earnings, down from a 52-week high of $383.40. Analysts maintain a $292.42 average target price, suggesting 30% upside from current levels, yet the stock has dramatically underperformed the broader market.

While the S&P 500 gained 14.8% over the past year, Accenture shareholders endured a 41% decline. Over five years, the stock is down 5.6% while the S&P 500 surged 76.5%. Even the dividend hasn’t offset this underperformance-total returns including reinvested dividends would still trail the index significantly.

The disconnect stems from concerns about Accenture’s growth trajectory. Fourth quarter fiscal 2025 revenue of $17.60 billion grew 7.3% year-over-year, but management’s fiscal 2026 guidance calls for just 2-5% revenue growth in local currency. That deceleration has investors questioning whether the company can maintain its premium valuation as traditional IT services spending slows.

Recent Wins and Strategic Positioning

Despite the stock’s struggles, Accenture continues winning major contracts that could support future dividend growth. The company recently secured a position on the U.S. Department of Veterans Affairs Electronic Health Record Modernization program, a multi-billion dollar mandate that reinforces its standing as a preferred partner for large-scale digital transformations.

In January, Accenture Federal Services won a $1.4 billion task order to modernize the Army Corps of Engineers’ cybersecurity system, though competitor SAIC has challenged the award. The company has also partnered with Palantir Technologies on sovereign AI data centers in EMEA, positioning itself in the high-growth artificial intelligence infrastructure market.

UBS analysts identify Accenture as a key beneficiary of increased generative AI spending, noting that enterprises are ramping up consulting budgets to implement AI capabilities. The firm maintains strong profitability with a 10.8% profit margin and 25% return on equity.

Capital Allocation Beyond the Dividend

Accenture doesn’t just return cash through dividends. The company repurchased $4.62 billion of stock in fiscal 2025, bringing total shareholder returns to $8.32 billion-roughly 71.6% of operating cash flow. This aggressive buyback program has helped offset dilution from stock-based compensation while supporting earnings per share growth even as revenue growth moderates.

The company ended its most recent quarter with $11.48 billion in cash and maintains a $5 billion share buyback authorization. This financial flexibility provides management with options to accelerate buybacks if the stock remains depressed or to pursue strategic acquisitions that could reignite growth.

What the Dividend Scorecard Shows

Institutional investors continue backing Accenture despite the stock’s weakness. ING Groep recently increased its stake by 219.3%, bringing its position to 141,196 shares valued at $34.8 million. The analyst community maintains a moderate buy rating, with 3 strong buy ratings, 13 buy ratings, 11 hold ratings, and just 1 sell rating.

The dividend itself scores well on sustainability metrics but faces questions on total return potential. The 20+ year growth streak and 2.94 times cash flow coverage earn high marks for safety and consistency. The 2.6% current yield sits above the S&P 500 average but trails other technology dividend payers like IBM’s 2.3%.

Where Accenture stumbles is in capital appreciation. A dividend growth rate of 12.1% looks impressive until you consider the stock’s 41% decline over the past year. Investors who bought Accenture for income a year ago have seen their total position value drop substantially despite receiving growing dividend checks.

The Path Forward

Accenture’s dividend remains on solid footing. The company generates ample cash flow, maintains conservative payout ratios, and operates in markets-AI consulting, digital transformation, cybersecurity-that should support long-term growth. Management has demonstrated unwavering commitment to the dividend through two decades of increases, including during the 2008 financial crisis and COVID-19 pandemic.

The challenge lies in valuation and growth expectations. At current prices, Accenture offers a forward P/E of 17.5 based on fiscal 2026 guidance of $13.19-$13.57 in earnings per share. That’s reasonable for a business with strong returns on capital and a growing dividend, but only if revenue growth reaccelerates beyond the 2-5% guided range.

For dividend-focused investors, Accenture presents a nuanced case. The dividend itself deserves a solid B+ grade: safe, growing, and backed by strong fundamentals. But total return prospects depend on whether the company can prove that generative AI consulting revenues will offset weakness in traditional IT services spending. The next few quarters will determine whether this dividend grower can also deliver the stock price appreciation that income investors need to achieve their overall return objectives.