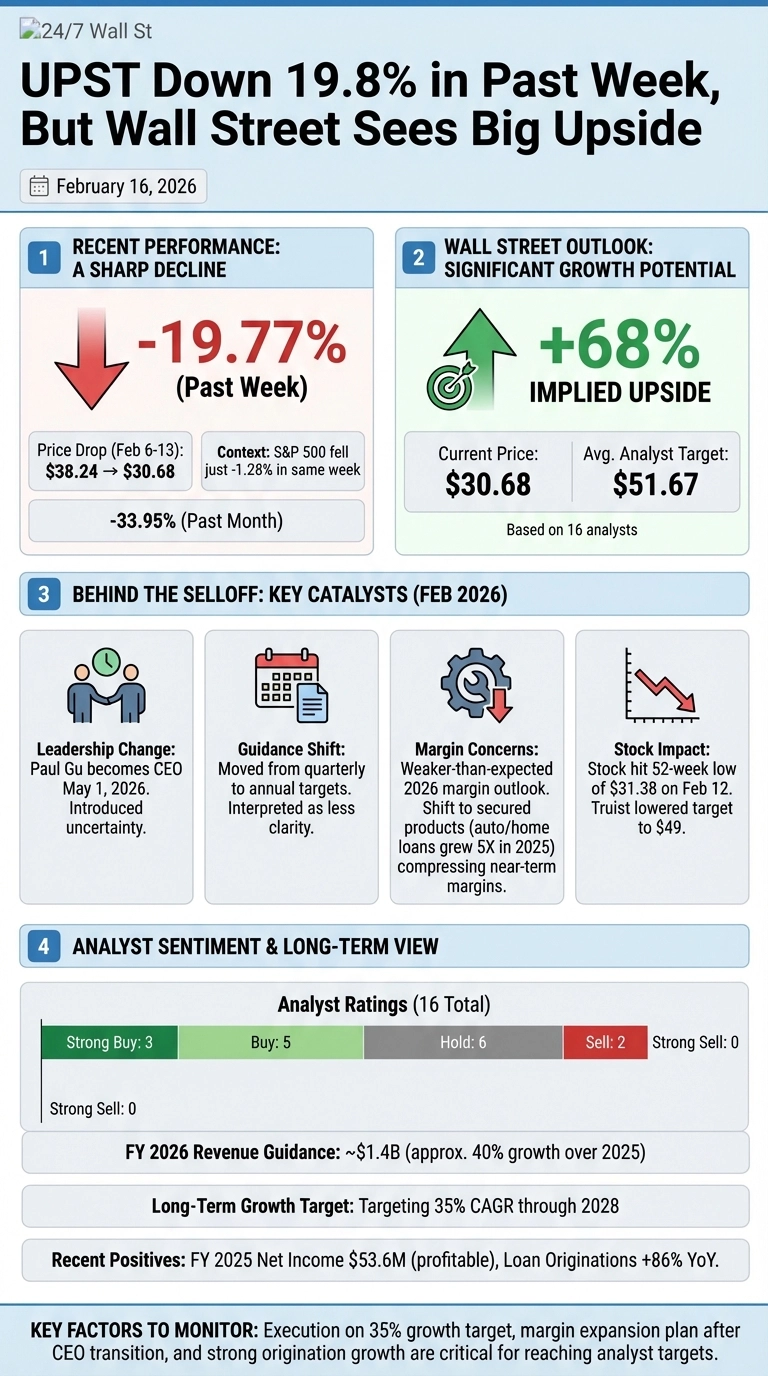

Upstart Holdings (NASDAQ: UPST) has dropped 19.77% over the past week, falling from $38.24 to $30.68 as of February 13. That’s a sharp decline for a stock that Wall Street still sees climbing to $51.67, implying 68% upside from current levels. The AI-powered lending platform reported fourth-quarter 2025 results on February 10, beating revenue estimates but triggering a selloff that has now erased 33.95% of its value over the past month. The broader market barely budged during this period, making this a company-specific event worth examining closely.

A Leadership Shakeup Overshadowed Strong Results

Upstart delivered $296.09 million in Q4 revenue, beating the consensus estimate of $294.45 million. Full-year revenue climbed 64% to over $1 billion, and loan originations surged 86%. The company returned to profitability with $53.6 million in net income for 2025 after posting a $129 million loss in 2024.

But investors fixated on two announcements that came with the earnings release. First, co-founder Paul Gu will replace the current CEO on May 1, 2026. Second, the company is shifting from quarterly guidance to annual targets only, citing a desire to focus on long-term execution rather than short-term forecasting. According to TIKR.com, the stock “plummeted 14%” specifically due to the leadership change and guidance shift. The market interpreted the moves as introducing uncertainty at a time when investors wanted clarity on how the company would sustain its momentum.

Adding to the pressure, management outlined weaker-than-expected margin guidance for 2026. The shift toward secured products like auto and home loans (which grew 5X in 2025) and a focus on prime borrowers is compressing contribution margins in the near term. Truist lowered its price target from $59 to $49, and Citizens downgraded the stock on valuation concerns. The stock hit a 52-week low of $31.38 on February 12.

Wall Street Still Sees the Growth Trajectory Intact

Despite the selloff, analysts remain constructive on Upstart’s long-term potential. The consensus price target of $51.67 sits well above the current price, and the ratings breakdown shows 3 Strong Buys, 5 Buys, 6 Holds, and just 2 Sells. That’s a net bullish tilt from 16 analysts covering the stock.

The bull case centers on Upstart’s ability to execute on its 35% compound annual growth rate target through 2028. Management is guiding for $1.4 billion in revenue for 2026, representing roughly 40% growth off the 2025 base. The company’s AI lending models continue to differentiate it from traditional credit underwriters, and its expansion into auto and home loans opens larger addressable markets than personal lending alone.

Even Goldman Sachs, which had previously rated the stock Sell, upgraded to Neutral on February 13 with a $35 price target. The firm acknowledged that the stock’s underperformance had created a “more balanced risk-reward profile” and recognized margin and take-rate compression that it had previously underestimated. That’s not exactly a ringing endorsement, but it signals that even skeptics see less downside risk at these levels.

The Numbers

Current Situation:

- Current Price: $30.68

- Average Analyst Target: $51.67

- Implied Upside: 68%

- Number of Analysts Covering: 16

- Recent Performance: Down 19.77% over the past week, down 33.95% over the past month

Analyst Ratings Breakdown:

- Strong Buy: 3

- Buy: 5

- Hold: 6

- Sell: 2

- Strong Sell: 0

Comparison to S&P 500:

- UPST Past Week: -19.77%

- S&P 500 Past Week: -1.28%

- UPST YTD: -29.84%

- S&P 500 YTD: -0.02%

The data suggests Wall Street is betting on execution over the next 12 to 24 months rather than immediate margin recovery. The stock is trading at 68x trailing earnings, reflecting the market’s skepticism about near-term profitability.

Key Factors to Monitor

Investors watching Upstart will likely focus on whether the new CEO delivers on the 35% growth target and whether margin compression proves temporary. The company has demonstrated it can scale originations rapidly, and its AI models provide a competitive advantage in underwriting. The leadership transition and shift to annual guidance introduce execution uncertainty that the market has shown it will monitor closely.

The 68% implied upside reflects analyst confidence in the long-term growth trajectory, though near-term margin pressure and the CEO transition represent key risks to that thesis. Competitors like Affirm (NASDAQ: AFRM | AFRM Price Prediction) have maintained stronger analyst support (consensus target of $86 with 22 Buys and 8 Holds), suggesting the market sees clearer visibility in alternative lending platforms with more established leadership teams.

The company’s ability to report strong origination growth over the next two quarters and articulate a clear margin expansion plan after the CEO transition in May will likely determine whether the stock can reach analyst price targets. Until those milestones are achieved, the risk-reward profile remains uncertain despite the attractive valuation relative to the growth outlook.

Contact [email protected] for any questions or corrections.