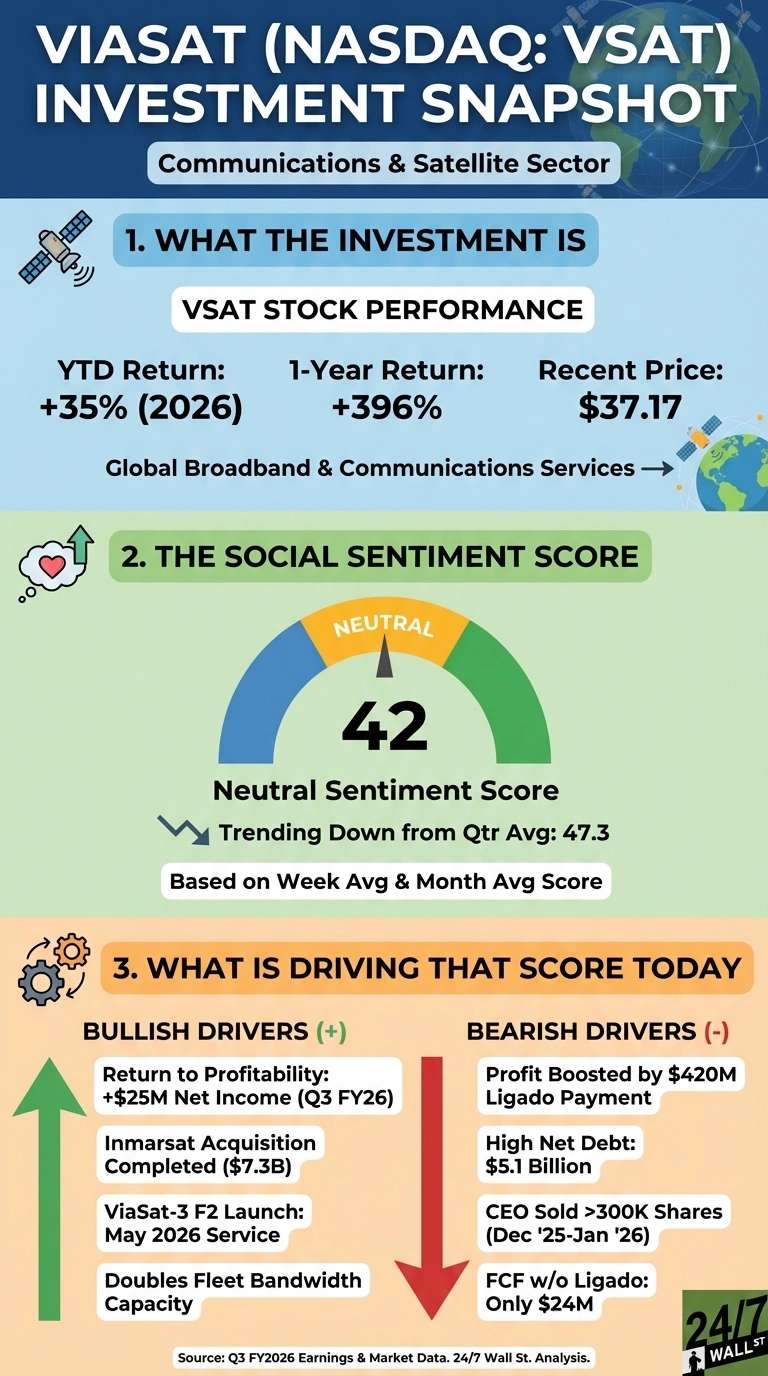

For potential investors or current shareholders watching closely, shares of Viasat (NASDAQ:VSAT) have climbed almost 35% year-to-date and are up 396% over the past twelve months, yet retail sentiment on Reddit sits at a neutral 42 out of 100, drifting down from a quarterly average of 47. It’s this gap between operating results and crowd conviction that tells a story: Viasat is returning to profitability, closing its massive Inmarsat deal, and preparing to double its satellite bandwidth, yet the market remains unsure whether to trust it and make it part of a core investment strategy.

Right now, investors are watching closely after Q3 FY2026 earnings showed net income swung from a $158 million loss to a $25 million profit year over year. Building on this positive momentum is the notion that ViaSat-3 F2 is on track to enter service in May 2026 and double the company’s entire fleet bandwidth.

Why Reddit Isn’t Celebrating Viasat’s Comeback

Discussion volume around VSAT is thin, with just 4 qualified mentions over the quarter, and concentrated in value-focused communities. Investors acknowledge the infrastructure assets but keep circling the same structural concerns:

- Q3 profitability was driven almost entirely by a $420 million Ligado lump-sum payment; excluding it, free cash flow was just $24 million

- EPS declined 2.6% annually over five years while revenue grew 15.4%, meaning growth has come at the cost of per-share value

- Net debt is $5.1 billion against a roughly $6.3 billion market cap, and Executive Chairman Mark Dankberg sold over 300,000 shares between December 2025 and January 2026

One r/wallstreetbets user framed the bull case directly, writing: “$VSAT is undervalued, I think. Someone prove me wrong.”

$VSAT is undervalued, I think. Someone prove me wrong

by u/[OP] in wallstreetbets

The Moat Is Real, But the Price Already Knows It

Analysts are also watching Viasat closely, with Deutsche Bank upgrading Viasat to Buy with a $48 price target and Morgan Stanley putting a $51 price target. With shares trading at $46, the consensus analyst target of $43.60 sits below the higher analyst targets and below current trading levels, a concerning sign. This said, the infrastructure moat, ground networks, multi-orbit capability, and a $4 billion backlog are difficult to replicate. Two more satellite launches and a deleveraging path are the key milestones analysts are watching as Viasat works to sustain its recent momentum.

Data Sources

- Viasat Q3 FY2026 SEC filing (February 5, 2026) via Fuse API: segment revenue, net income, FCF, and balance sheet figures

- Alpha Vantage News Sentiment (January 24 – February 23, 2026): analyst upgrades, Inmarsat acquisition close, news sentiment scoring

- StockStory/Finviz: Viasat Buy, Sell, or Hold Post Q4 Earnings?: five-year EPS and FCF margin data