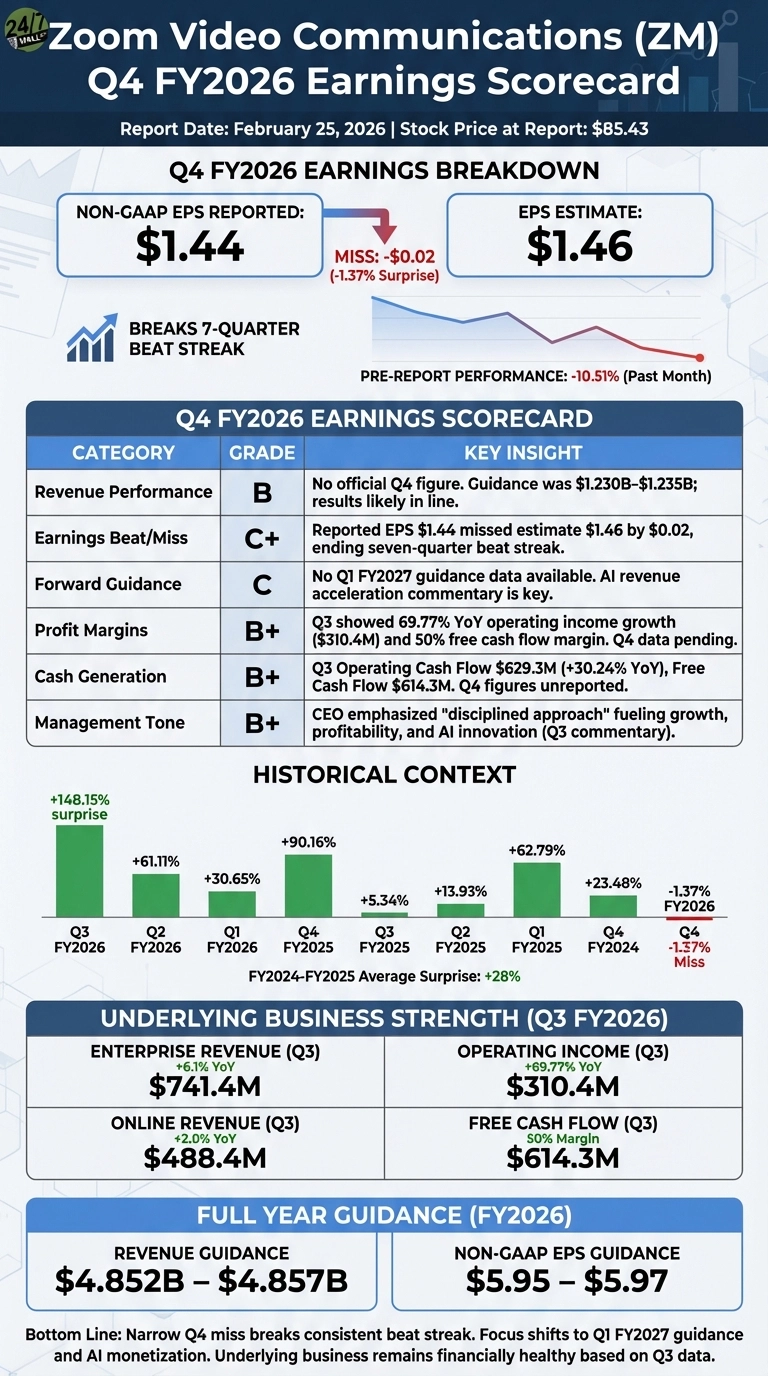

Zoom Video Communications (NASDAQ: ZM) reported Q4 FY2026 results on Feb. 25, 2026, delivering a rare earnings miss that breaks a long streak of beats. Non-GAAP EPS came in at $1.44, falling short of the $1.46 consensus estimate by 1.37%. The stock entered the report already under pressure, down 10.51% over the prior month and sitting at $85.43. For a company that had beaten estimates in each of the prior seven quarters, including a remarkable +148% surprise in Q3 FY2026, the miss carries more symbolic weight than its small magnitude suggests.

Q4 FY2026 Earnings Scorecard

| Category | Grade | Key Insight |

|---|---|---|

| Revenue Performance | B | No official revenue figure has been confirmed in our data, but management had guided to $1.230B–$1.235B; results appear in line with that narrow range based on available context. |

| Earnings Beat/Miss | C+ | Reported EPS of $1.44 missed the $1.46 estimate by $0.02, ending a seven-quarter beat streak. The miss is small but notable given prior consistency. |

| Forward Guidance | C | No Q1 FY2027 guidance data is available in our sources at this time. Investors will be watching for any commentary on AI-driven revenue acceleration in the coming quarters. |

| Profit Margins | B+ | The prior quarter showed exceptional profitability, with operating income up 69.77% YoY to $310.4M and a 50% free cash flow margin. |

| Cash Generation | B+ | Q3 free cash flow reached $614.3M on $629.3M in operating cash flow, up 30.24% YoY. Q4 cash flow figures remain unreported but the prior trajectory was strong. |

| Management Tone | B+ | CEO Eric Yuan’s prior commentary emphasized disciplined execution: “Our disciplined approach is fueling top-line growth, stellar profitability, and lower dilution helping us turn AI innovation into real, lasting value for customers and shareholders.” |

Bottom Line

The underlying business remains financially healthy. Enterprise revenue had been growing faster than the online segment, +6.1% versus +2.0% YoY in Q3, and the company’s AI Companion rollout represents a credible product catalyst. The full-year FY2026 guidance called for revenue of $4.852B–$4.857B and non-GAAP EPS of $5.95–$5.97, which would represent steady if unspectacular progress.

Investors should focus on Q1 FY2027 guidance and any update on AI Companion monetization. Whether this miss reflects a one-quarter stumble or a trend shift in earnings power is the central question heading into the next report.