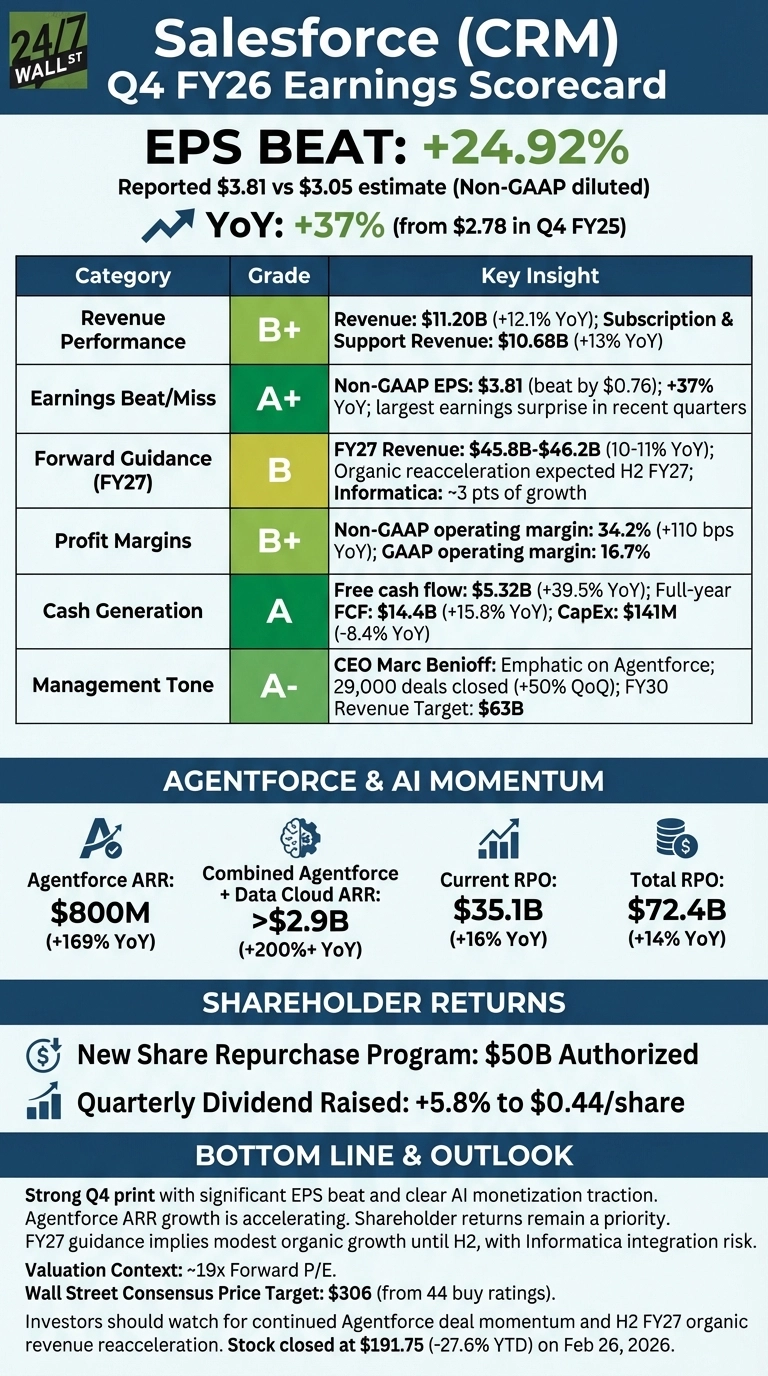

Salesforce delivered a standout Q4 FY26, with non-GAAP EPS of $3.81 crushing the $3.05 consensus estimate by nearly 25%, while Agentforce momentum signaled that the company’s AI pivot is generating real commercial traction. Despite the strong print, the stock entered the session at $191.75, down 27.6% year-to-date, reflecting broader investor concerns about growth deceleration that this report may begin to address.

Q4 FY26 Earnings Scorecard

| Category | Grade | Key Insight |

|---|---|---|

| Revenue Performance | B+ | Revenue of $11.20B grew 12.1% YoY, meeting expectations with a modest beat; subscription and support, which makes up 95% of revenue, rose 13% YoY to $10.68B. |

| Earnings Beat/Miss | A+ | Non-GAAP EPS of $3.81 beat estimates by $0.76, up 37% from $2.78 in Q4 FY25; the largest earnings surprise in recent quarters. |

| Forward Guidance | B | FY27 revenue guided to $45.8B-$46.2B (10-11% growth), with organic reacceleration expected only in H2; Informatica accounts for roughly 3 points of that growth. |

| Profit Margins | B+ | Non-GAAP operating margin expanded 110 basis points YoY to 34.2%; GAAP operating margin of 16.7% compressed versus prior quarters due to Informatica-related costs. |

| Cash Generation | A | Free cash flow surged 39.5% YoY to $5.32B in the quarter; full-year FCF reached $14.4B, up nearly 16%, with CapEx falling to just $141M. |

| Management Tone | A- | CEO Marc Benioff was emphatic on Agentforce, citing 29,000 deals closed, up 50% QoQ, and reaffirming a raised FY30 revenue target of $63B. |

Bottom Line

The headline story here is the EPS beat paired with genuine AI monetization. Agentforce ARR hit $800M, up 169% YoY, and combined Agentforce and Data Cloud ARR exceeded $2.9B, growing over 200% YoY. Current RPO of $35.1B, up 16%, suggests durable near-term revenue visibility. The new $50B share repurchase authorization and a 5.8% dividend increase to $0.44/quarter reinforce capital discipline.

The caution flag: FY27 guidance implies organic growth remains modest until the second half, and Informatica integration carries execution risk. With the stock trading at roughly 19x forward earnings against a Wall Street consensus price target of $306 from 44 buy ratings, investors weighing the setup should watch Q1 FY27 results closely. If Agentforce deal volume continues to compound at its current pace and H2 organic reacceleration materializes, the gap between the current price and analyst targets narrows considerably.

Contact [email protected] for any questions or corrections.