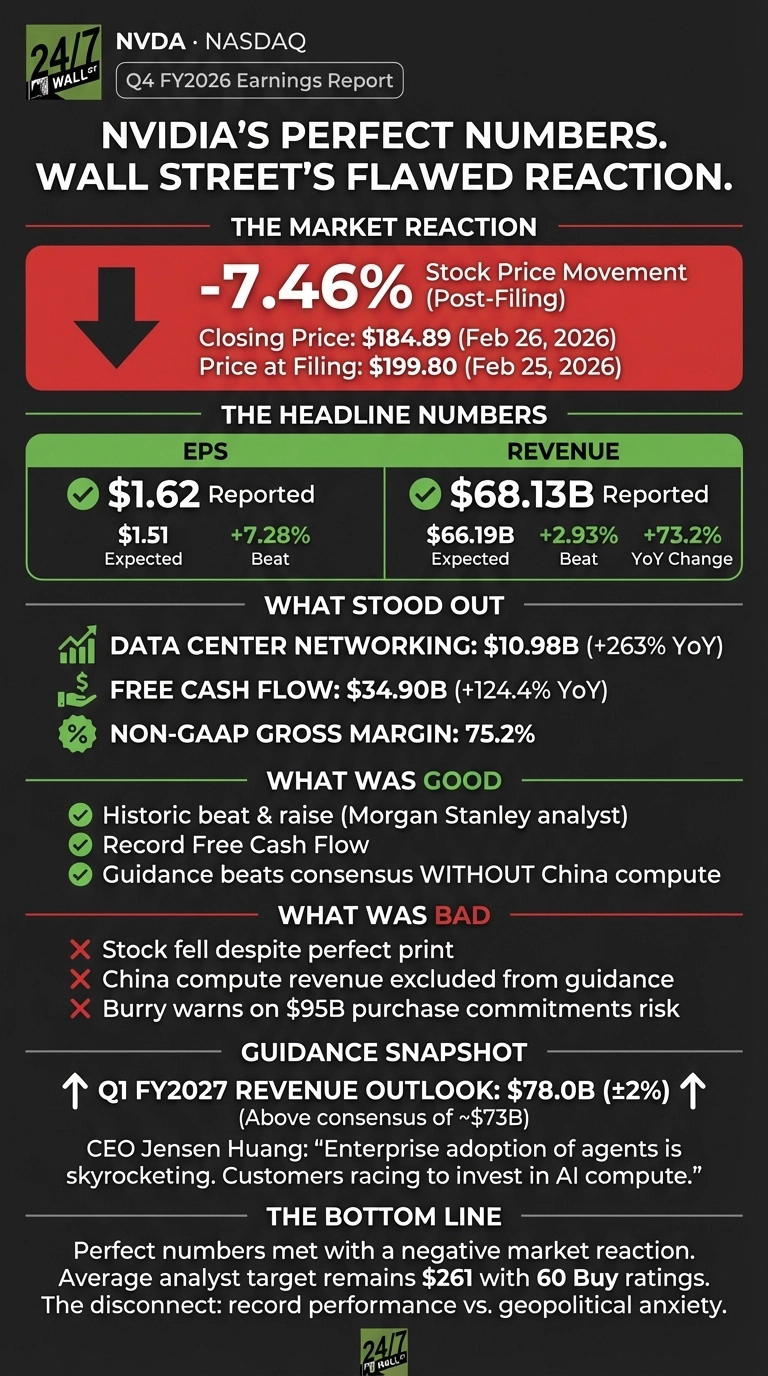

Yesterday we were watching whether Nvidia’s Q4 results would finally break the stock out of its range. The numbers were, by any objective measure, perfect. And yet this morning, shares are sitting near $184.89, down roughly 7% from the $199.80 price at the time of filing. Wall Street is doing what Wall Street does: finding reasons to sell a great story.

The Numbers Left Nothing to Complain About

Nvidia posted $68.13 billion in revenue, beating estimates by nearly $2 billion and growing 73% year over year. EPS came in at $1.62 against a $1.51 estimate, the fourth consecutive quarter of beating consensus. Free cash flow hit $34.9 billion, up 124% year over year. Non-GAAP gross margins held at 75.2%.

The segment deserving more attention: Data Center Networking surged 263% year over year to $10.98 billion, driven by the NVLink compute fabric ramp on GB200 and GB300 systems. That is not a GPU story. That is an AI infrastructure story, signaling Nvidia’s moat is widening beyond chips into the connective tissue of every major AI data center being built right now.

Morgan Stanley analyst Joseph Moore called it “the largest, cleanest beat and raise in the history of the semis industry.” Q1 FY2027 guidance came in at $78 billion, plus or minus 2%, roughly $5 billion above what the Street had penciled in.

China Is the Asterisk Wall Street Cannot Stop Staring At

That $78 billion guidance excludes all Data Center compute revenue from China. Export restrictions have effectively walled off one of the world’s largest AI markets. Nvidia previously took a $4.5 billion charge in Q1 FY2026 tied to China restrictions on H20 chips. The market is pricing in ongoing geopolitical drag, and that anxiety is legitimate. China is not a rounding error.

But the selloff misses the point: Nvidia guided to $78 billion without China, and that number still beats consensus. The business is now large enough that losing an entire country’s data center compute revenue still produces record guidance. That is the real headline.

Management Tone and Market Reaction

CEO Jensen Huang was unambiguous on the call: “Enterprise adoption of agents is skyrocketing. Our customers are racing to invest in AI compute.” Reddit captured the retail frustration, with one post asking “How is NVDA down almost 3% after the blockbuster print?” generating 722 comments. The selloff is not irrational, but it is shortsighted.

What to Watch From Here

Analyst price targets average $261 with 60 buy ratings against just one sell. Watch how those targets shift after today’s open, and whether the China exclusion in guidance becomes a recurring line item or a one-quarter footnote. That distinction will define the next leg for this stock.

Nvidia reported the cleanest earnings in semiconductor history, guided above consensus without China, and generated nearly $35 billion in free cash flow in a single quarter. The numbers were perfect. The market reaction was not.

Contact [email protected] for any questions or corrections.