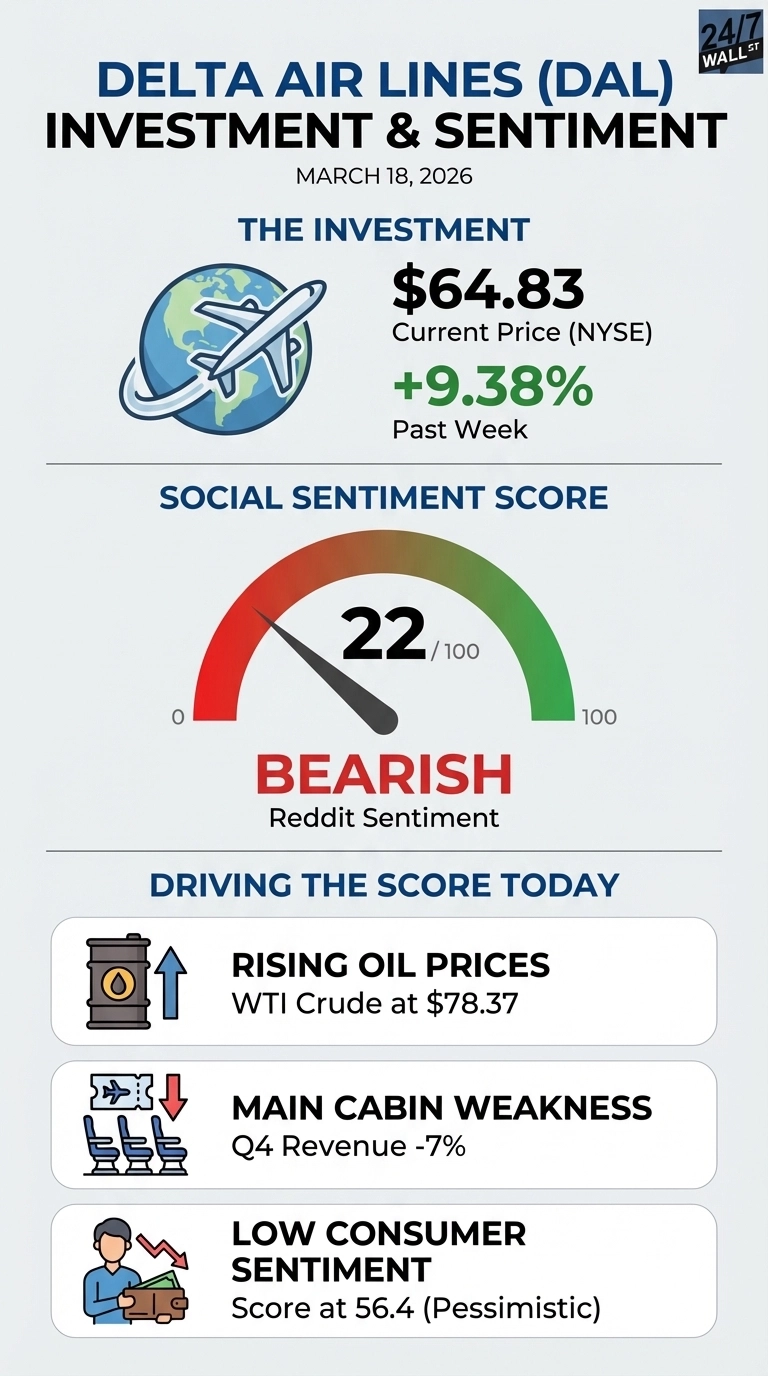

Still one of the world’s most notable airlines, Delta Air Lines (NYSE:DAL | DAL Price Prediction) sits at $64.83 after surging 9.38% over the past week, yet Reddit’s sentiment score dropped to 22 out of 100 on Wednesday morning, indicating a firm bearish tone. That contradiction is the story. Delta raised its Q1 revenue growth guidance to the high single digits, above its prior 5-7% forecast, while absorbing roughly $400 million in additional fuel costs since the escalation of the Iran conflict. The real question: is the $4.64 billion free cash flow machine a genuine fortress, or does it depend on a fuel environment that no longer exists?

The Oil Shock Debate

The bearish sentiment shift traces directly to oil, as WTI crude climbed from $63.09 in early February to $78.37 by March 6, landing Delta in a broader r/stocks discussion about energy-cost exposure. User yogi2350 framed it plainly in a post that drew 80 upvotes and 55 comments:

Oil prices creeping up again, which stocks are most exposed on a P/E basis?

by u/yogi2350 in stocks

The bull counter came from r/investing, where user MathTradeMan posted a recovery thesis that pushed sentiment to 78. The core argument: Delta owns a Pennsylvania crude refinery, letting it capture refining margins when jet fuel spikes rather than absorbing the full hit. “Management said hedging is a loser’s game long-term and bought a refinery instead. That’s a contrarian capital allocation decision that looks really smart right now,” the post read, noting Delta’s 2026 guidance was built on $2.28/gallon jet fuel.

Delta Airlines is different then every airline, I think it’ll be the best recovery play

by u/MathTradeMan in investing

Why Reddit Is Split on Delta Right Now

Sentiment swung from 78 on March 9 to 22 by March 18. Three forces drive the debate:

- Delta’s 2025 free cash flow hit a record $4.64 billion, up 61% year-over-year, giving it a financial cushion most airlines lack entering this oil shock

- Main cabin ticket revenue fell 7% in Q4 2025 to $5.62 billion, even before fuel costs surged, raising questions about whether premium pricing can offset coach volume softness

- University of Michigan consumer sentiment sits at 56.4, deep in pessimistic territory, which historically precedes reduced discretionary spending

The guidance raise briefly pushed sentiment back to 60, with one r/StockMarket post noting Delta raised revenue guidance “mid-Iran war” as a genuine surprise. CEO Ed Bastian confirmed the demand picture: “2026 is off to a strong start with top-line growth accelerating on consumer and corporate demand.”

United’s Slide Puts Delta’s Resilience in Context

United Airlines (NASDAQ:UAL) is down 16% year-to-date versus Delta’s more modest 6% decline, a gap that reflects how Delta’s premium revenue mix and refinery ownership are being priced as defensive advantages. The key watch is whether Delta’s full-year EPS guidance of $6.50 to $7.50 holds as jet fuel costs stay elevated above the $2.28/gallon assumption baked into that forecast.