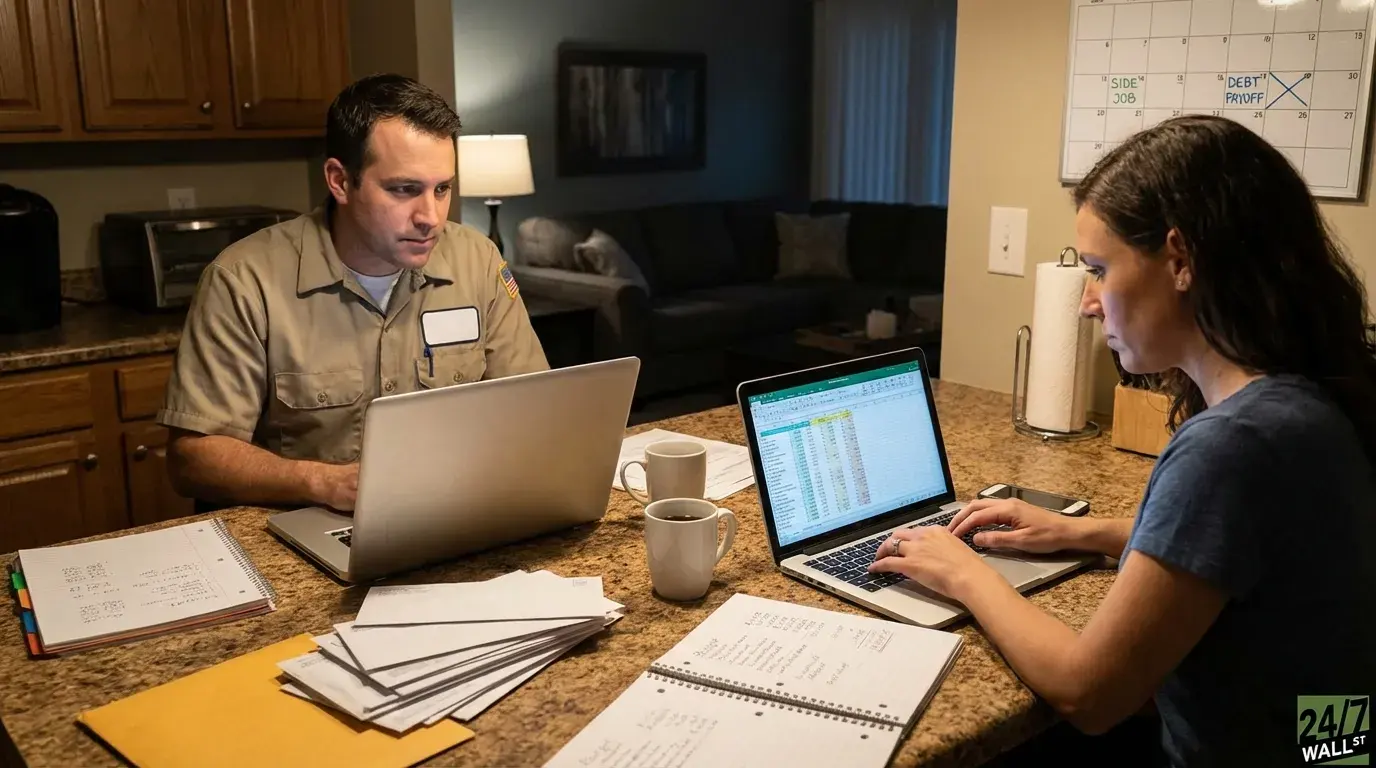

Brandon, an employee at Ramsey Solutions, and his wife Madison paid off $118,000 in debt over four years while raising three children. They did it by working extra jobs, eating at home, and sacrificing evenings with their kids. The story is real, the sacrifice was steep, and the math behind how they pulled it off is something most people never sit down to calculate.

Dave Ramsey’s observation during the conversation is worth examining closely: “It takes you about as long to get out as it did to get in. So if you spend 3 years making the mess, it takes you about 3 years to fix the mess. And my experience has been different than Larry’s. I think maybe because we’ve got the whole gazelle intensity thing going. It’s roughly about half.” That claim — that aggressive debt payoff can cut the recovery timeline in half — is the financial mechanic worth understanding here. It is directionally correct, but the math only works if you dramatically increase the money flowing toward debt every month.

Why the “Half the Time” Rule Requires Doubling the Effort

Debt grows because of compound interest: every month you carry a balance, the lender adds interest to what you owe, and next month you pay interest on that interest. The only way to reverse the math is to throw money at the principal faster than interest accumulates.

Brandon described eliminating approximately $25,000 to $30,000 in debt annually across four years. On a $118,000 balance, that pace of repayment far exceeds what a minimum-payment strategy would accomplish on most consumer debt. The two side jobs were not a lifestyle upgrade — they were the mechanism that made the math work.

Consider a household carrying $118,000 in mixed consumer debt at an average interest rate of 9%, a plausible blend of car loans, student debt, and credit cards. On a standard 10-year repayment plan, monthly payments would run approximately $1,495, and total interest paid would approach $61,000.

Now apply Brandon and Madison’s approach: direct $2,500 to $2,900 per month toward that same debt. At that pace, the balance clears in roughly four years, and total interest paid drops sharply. The difference between the two paths represents tens of thousands of dollars in interest that never gets paid. That is the financial case for intensity, and it is why Ramsey’s “half the time” observation holds when the extra income is real and consistently applied.

The Side Income Variable Most Plans Ignore

Brandon worked two side jobs to generate the surplus needed. This is where many debt payoff plans stall: people try to find the extra $500 to $700 per month purely through spending cuts, hit a ceiling, and lose momentum. Cutting spending reduces outflow; adding income increases inflow. Both matter, but income has no ceiling the way spending cuts do.

Madison emphasized: “A lot of patience and a lot of trusting your partner. There has to be good communication between both of you about where your money’s going.” Household debt payoff at this pace requires both partners to agree on every discretionary dollar, because a single month of lifestyle drift can erase weeks of side-job earnings.

The national backdrop makes their outcome striking. The U.S. personal savings rate stood at just 4% in the fourth quarter of 2025, down from 6.2% a year earlier. The average American is saving four cents of every disposable dollar. Brandon and Madison were redirecting a large share of their income toward debt elimination — a rate that requires structural changes to how money flows through a household, not just tighter grocery budgets.

Who Can Replicate This and Who Cannot

This approach works best for a household with two working-age adults, at least one of whom has a skill that can generate side income — freelance work, skilled labor, tutoring, or gig-economy work. It works when fixed expenses like housing and insurance are already lean relative to income, and when both partners are genuinely aligned on the goal, because the sacrifices are too visible and too daily to sustain without shared commitment.

The approach is harder for single-income households, for people whose primary job already demands long hours, or for those with caregiving responsibilities that limit available evening hours. Brandon acknowledged the cost directly: “The hardest part is giving up time with the kids, giving up time with family at night.” That trade-off is real and worth naming before committing to it.

The Calculation You Should Run Before Starting

List every debt you carry with its current balance and interest rate. Use a free debt payoff calculator to find your total interest paid under your current payment pace. Then recalculate with an extra $500 per month, an extra $1,000, and an extra $1,500. The difference in payoff date and total interest will tell you exactly how much your time and side income are worth in actual dollars before you commit to a single extra shift.

Brandon and Madison’s story is a worked example of a specific financial mechanic: more money applied to principal earlier saves a disproportionate amount of interest later. As Brandon put it: “You got yourself into it, you got to get yourself out of it. Just do it. Put in the work.” The math agrees with him.

Contact [email protected] for any questions or corrections.