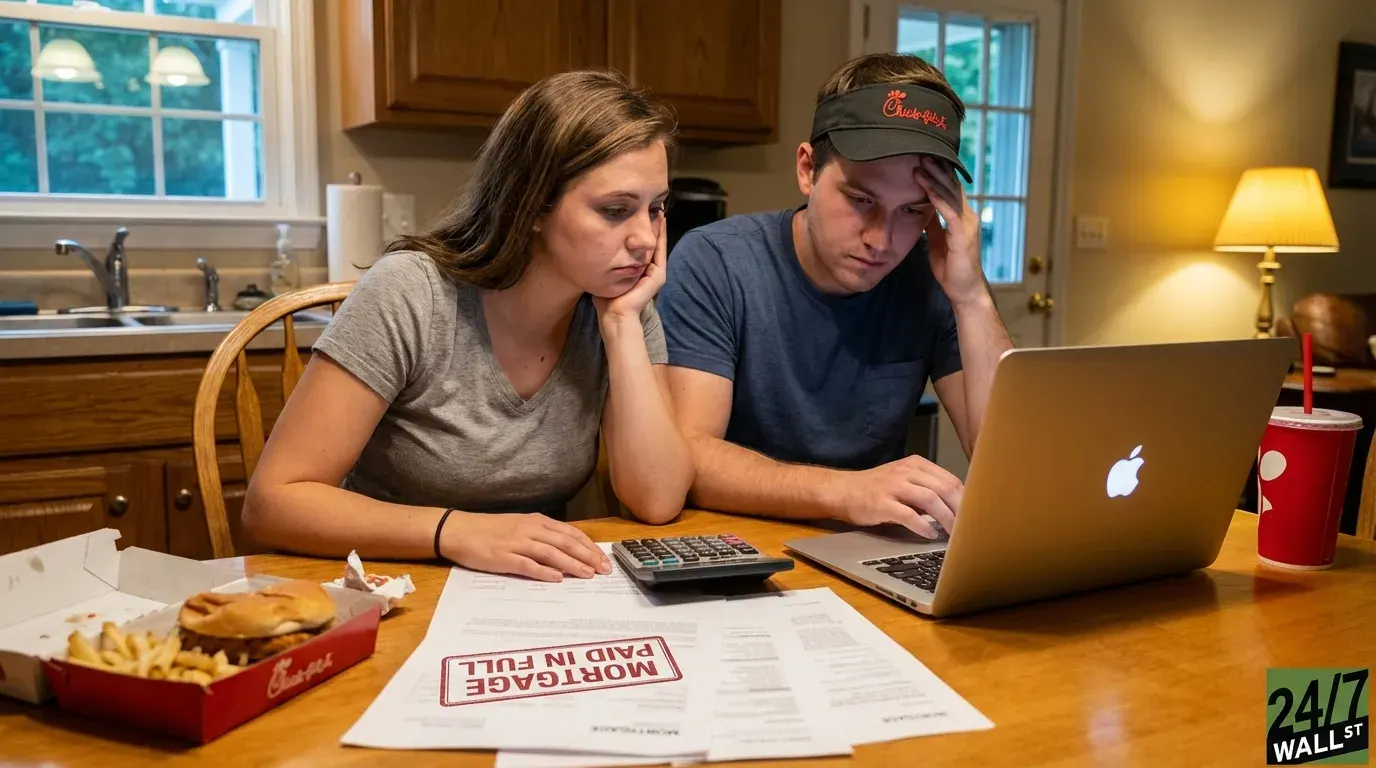

On their honeymoon, Holly turned to her new husband Josh and said, “Can we please get jobs at Chick-fil-A?” It was a plan. Eighteen months later, the couple had paid off $175,000, including their house, at age 27. Dave Ramsey called it a “mic drop” moment for Gen Z. The story earns that label, and it also contains a practical blueprint worth understanding.

What They Actually Did

Josh and Holly, both Ramsey Solutions team members, worked a combined 70 hours per week at their regular jobs plus 15 to 20 additional hours at Chick-fil-A. The food angle was deliberate. “They feed you every time you work. So like Thursday, Friday, Saturday, like meals were checked off the list,” Holly explained. Every shift eliminated a line item from their budget, turning work hours into a direct reduction in living expenses.

Holly described the toll honestly: “There were definitely some nights, like when you’re in the grind of like Thursday night, we’re eating chicken again, and we’re like, I’ve got to go make chicken after this. We were shells of humans.” Josh’s framing was equally direct: “It was really fun to like lock arms in the first year of marriage.”

Ramsey’s verdict on the show: “It’s obvious that you guys were really dialed in together, and there wasn’t one of you dragging the other one along. You can take on anything if you do that.” That observation deserves more attention than it usually gets.

Why Paying Off a Mortgage Early Saves More Than Most People Expect

Paying off $175,000 in 18 months required channeling an extraordinary share of their combined income toward the mortgage each month, on top of normal living expenses. For most households, that level of debt repayment is not achievable without a combination of high income, dramatically reduced spending, or both. Josh and Holly used both levers simultaneously.

The interest savings make the math compelling. On a 30-year mortgage, a borrower typically pays back far more than the original loan balance over the life of the loan. Eliminating that debt in 18 months wipes out the vast majority of that cost. The second job generated income while simultaneously eliminating food costs, compressing the payoff timeline from both directions at once.

The national savings rate has declined from 6.2% in early 2024 to 4.0% by late 2025, meaning the average American household is saving a shrinking fraction of already-stretched income. Josh and Holly were operating at a savings rate that is a multiple of the national norm, in an environment where most Americans feel financially stretched.

Who This Strategy Fits and Who It Does Not

The approach works cleanly for couples in their mid-20s to early 30s with no children, stable dual incomes, and a mortgage balance under $200,000. That profile has the physical capacity for a 90-hour combined work week, the flexibility to sacrifice social spending, and a short enough runway that the sacrifice has a visible finish line. Josh and Holly also had an edge most people overlook: they were aligned from day one. One partner dragging while the other pushes is the most common reason aggressive payoff plans collapse.

The strategy becomes harder to replicate for households with children, single-income earners, or people carrying high-interest consumer debt alongside a mortgage. In those cases, sequencing matters. Ramsey’s own framework addresses this: eliminate non-mortgage debt first, build a three-to-six month emergency fund, then attack the mortgage. Paying down a mortgage while carrying 20% credit card debt is the wrong order of operations.

A 35-year-old with a $400,000 mortgage, two kids, and $30,000 in credit card debt cannot replicate this story directly. But the underlying principle, channeling every available dollar toward a single target until it is gone, is exactly the same. The target and the timeline change. The mechanics do not.

How to Apply This Approach to Your Own Mortgage

Start by identifying your own version of the Chick-fil-A shift: any income source that also offsets an existing expense, whether a side job that covers groceries, freelance work that replaces a subscription budget, or a weekend gig that eliminates a dining-out habit. The compounding effect of earning and saving simultaneously is what made their timeline possible.

Then find your own break-even. Take your current mortgage balance, find your interest rate, and use a free amortization calculator to see what your total interest cost looks like at the current payoff pace versus an accelerated one. Seeing that number concretely is what turns vague intention into a real plan.

Josh noted the key was “taking time to be grateful throughout the journey.” That is not sentiment. It is a practical tool for sustaining effort over 18 months of 85-hour weeks. The financial mechanics are learnable. The willingness to stay in the grind is what actually determines the outcome.

Contact [email protected] for any questions or corrections.