Fidelity Blue Chip Growth ETF (NYSEARCA:FBCG) is down 11.67% year to date as of late March 2026, a sharper pullback than the 8.42% decline in the Nasdaq 100 (QQQ) over the same period. For a fund built around owning the best large-cap growth companies, the first quarter of 2026 has been a stress test.

A Growth Fund Built on Mega-Cap Concentration

FBCG is an actively managed ETF launched in June 2020 with $5.4 billion in assets under management and an expense ratio of 57 basis points. Its mandate: own the highest-conviction large-cap growth names that Fidelity’s managers believe have durable earnings power.

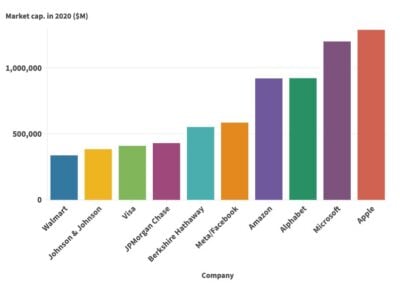

The result is a portfolio built around mega-cap concentration. NVIDIA alone represents 15.68% of the fund, followed by Apple at 9.49%, Alphabet at 8.42%, and Amazon at 7.76%. Those four names together drive a large share of daily returns.

Over the past year the fund has still delivered 17.37% in total return, but the recent drawdown reflects how quickly sentiment can shift when the macro environment tightens around the exact names this fund owns most heavily.

Export Controls and AI Trade Policy Will Define the Next 12 Months

The most consequential macro force for FBCG over the next year is U.S. export control policy toward China and how it constrains the AI chip trade. This is not a peripheral risk. NVIDIA, the fund’s largest holding, explicitly excluded any Data Center compute revenue from China in its Q1 FY2027 guidance. The company absorbed a $4.5 billion H20 inventory charge in Q1 FY2026 and estimated an additional $8 billion in lost H20 revenue in Q2 FY2026 due to those restrictions.

Any easing of export licensing requirements would unlock a revenue channel currently zeroed out in NVIDIA’s own projections. Further tightening would pressure the fund’s top holding and likely ripple through Amazon’s AWS and Alphabet’s cloud businesses, both of which depend on NVIDIA hardware at scale. Monitor the Bureau of Industry and Security for export rule updates and watch NVIDIA’s quarterly earnings calls for any change in China revenue language. The VIX sits at 27.44 and in the 93.8th percentile of its one-year range, reflecting how much uncertainty is already priced into growth equities broadly.

Rising Treasury yields compound this pressure. The 10-year yield has climbed to 4.42%, up 0.38% in just the past month and above its 12-month average of 4.229%. Higher yields compress the valuation multiples that growth stocks command, and FBCG’s portfolio is priced for strong future earnings. If yields stabilize or retreat, that headwind eases. If they push toward the 12-month high of 4.58%, expect continued multiple compression across the fund’s top holdings.

NVIDIA’s Weight and What Fidelity Does With It

Because FBCG is actively managed, position sizing decisions matter as much as underlying fundamentals. NVIDIA’s Q4 FY2026 revenue of $68.13 billion grew 73% year over year, and the company guided Q1 FY2027 to approximately $78 billion. That growth trajectory is hard to ignore.

But at 15.68% of the fund, a 10% move in NVIDIA’s stock produces roughly a 1.5% move in FBCG’s NAV (net asset value, the per-share value of the fund’s holdings), before any other position moves.

Fidelity’s monthly holdings disclosures will show any trimming or addition to the NVIDIA position. A reduction would signal the manager is locking in gains and reducing concentration risk. An increase would signal conviction in NVIDIA’s continued dominance of AI infrastructure spending, which NVIDIA’s CEO Jensen Huang described as an “agentic AI inflection point” with demand he called exponentially growing. Holdings files are published on Fidelity’s ETF page and updated monthly.

The Two Scenarios That Matter

If U.S. export controls on AI chips ease and the 10-year Treasury yield stabilizes below 4.25%, FBCG’s top holdings gain on both the revenue and valuation fronts simultaneously. If controls tighten further or yields climb toward 5%, the fund’s heavy NVIDIA weighting becomes a concentrated liability. Either way, the macro scenarios above are secondary to how Fidelity’s manager responds to them through active position management.

Contact [email protected] for any questions or corrections.