Benchmark initiated coverage of Microsoft (NASDAQ:MSFT | MSFT Price Prediction) with a Buy rating and $450 price target, arguing that the stock’s steep retreat from its 2025 highs represents a compelling long-term entry point. Microsoft shares have fallen 28% from their October 2025 level of $517.54 to $370.17 as of March 31, 2026, even as the company’s underlying fundamentals have strengthened. For patient investors, Benchmark’s thesis is straightforward: the selloff has disconnected price from business reality.

| Ticker | Company | Firm | Action | New Rating | New Target |

|---|---|---|---|---|---|

| MSFT | Microsoft | Benchmark | Initiation | Buy | $450 |

The Analyst’s Case

Benchmark frames Microsoft as a leading AI orchestration platform across enterprise and consumer markets, with the pullback driven by investor anxiety over capital expenditure levels rather than any deterioration in demand. The firm views those AI-related capex concerns as shortsighted given strong demand visibility, contracted hardware capacity, and strategic positioning for the AI supercycle.

The data supports that read. Microsoft’s commercial remaining performance obligation surged 110% year-over-year to $625 billion in Q2 FY2026, signaling an unprecedented volume of contracted future revenue. Meanwhile, Azure delivered 39% year-over-year growth in Q2 FY2026 and has maintained 39% to 40% growth across three consecutive quarters. Forward guidance calls for 37% to 38% Azure growth in the coming quarter.

Company Snapshot

Microsoft operates three core segments. Intelligent Cloud generated $32.91 billion in Q2 FY2026 revenue, up 29% year-over-year. Productivity and Business Processes contributed $34.12 billion, up 16%. The company’s total cloud revenue crossed a milestone: Microsoft Cloud reached $51.50 billion in a single quarter for the first time, up 26% year-over-year. CEO Satya Nadella captured the strategic moment plainly: “We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business that is larger than some of our biggest franchises.”

Why the Move Matters Now

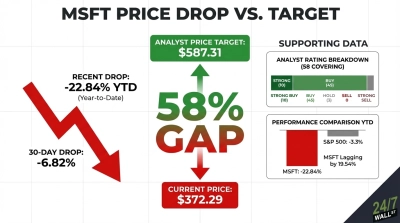

Microsoft stock is down 23% year-to-date in 2026, pushing it well below both its 200-day moving average of $478.51 and its 50-day moving average of $408.52. Yet Q2 FY2026 net income rose 59% year-over-year to $38.46 billion on revenue of $81.27 billion, beating estimates and growing 17% year-over-year. The forward P/E now sits at 33x, a meaningful compression from levels at the October highs. The broader analyst community is aligned: 54 analysts rate the stock Buy or Strong Buy against just 3 Holds and zero Sells, with a consensus price target of $589.90.

What It Means for Your Portfolio

Benchmark’s initiation adds a credible voice to a growing consensus that Microsoft’s pullback has created an asymmetric setup. The capex buildout, including a $5.5 billion Singapore AI infrastructure investment through 2029 and negotiations for a $7 billion natural gas power plant to supply data center capacity, reflects management’s conviction in sustained demand. Retirement-focused investors should weigh that conviction against near-term risks: recent insider activity shows a net selling direction across 31 transactions, and macro uncertainty continues to pressure the broader tech sector. The fundamental case is strong; position sizing and patience remain the appropriate discipline.