The White House just proposed a $1.5 trillion defense budget for fiscal year 2027, a roughly 44% increase over current Pentagon spending. Even though U.S. and Israeli forces are no longer engaged in the 2026 Iran war, geopolitical pressure is mounting globally, and Congress is at least having the conversation. The direction of travel for defense spending is unmistakable, and iShares U.S. Aerospace and Defense ETF (NYSEARCA:ITA | ITA Price Prediction) is the most direct way to own that trend in a single fund.

What ITA Is Built to Do

ITA tracks the Dow Jones U.S. Select Aerospace and Defense Index, giving investors concentrated exposure to the U.S. defense industrial base. The fund launched in May 2006 and now holds approximately $13.6 billion in net assets across 48 total holdings. The expense ratio is 0.38%, modest for a sector fund.

The return engine is straightforward: government contract revenue. The prime contractors inside ITA earn money almost exclusively from multi-year defense procurement deals, which are largely recession-resistant and inflation-adjustable. When the Pentagon budget grows, companies inside ITA grow their backlogs, revenue, and earnings.

The backlog picture at RTX (NYSE:RTX) shows why the thesis is compelling now. The company reported a $268 billion backlog alongside Q4 2025 sales of $24.24 billion. That is a company with years of locked-in revenue. Boeing (NYSE:BA), meanwhile, secured the F-47 next-generation stealth fighter contract, a landmark win validating the defense industrial base diversification strategy the Pentagon has been quietly pursuing.

A Long Track Record That Backs the Thesis

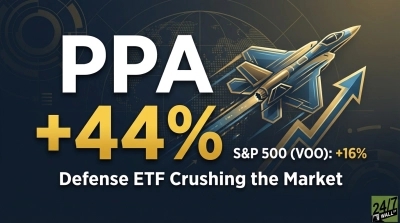

ITA has gained 68% over the past year and 118% over five years, compared to 64% for the S&P 500 over the same five-year period. Over a decade, ITA returned 322%, while the S&P 500 returned 218%. Defense spending cycles are long, and patient investors will win out for staying in the trade.

Year-to-date in 2026, ITA is up about 4%, while the S&P 500 is down nearly 2%. Defense is one of the few corners of the market that has held its ground as broader equities pulled back on rate and macro concerns.

Tradeoffs Investors Need to Understand

The fund’s concentration is its greatest strength and its most meaningful risk. The top three holdings represent nearly half the portfolio, meaning a serious operational stumble at a big contractor would drag the whole fund. RTX is carrying real execution risks: the Pratt and Whitney GTF engine crisis, a $1 billion missile liability settlement, and ongoing supply chain pressure. Boeing carries $54 billion in debt and is targeting 2026 as its “pivot year” back to profitability, a timeline that carries real execution risk.

The geopolitical trigger investors expect to drive the fund higher has produced a more complicated market reaction than anticipated. When the Iran conflict escalated in March 2026, defense ETFs, including ITA, actually slipped, with analysts pointing to already-elevated valuations and a market increasingly skeptical that traditional defense systems benefit as much from modern drone-centric warfare as the old playbook would suggest.

Trump’s $1.5 trillion request is the largest in decades, but Congress writes the actual appropriations. A budget proposal signals intent; the actual spending level depends on what lawmakers pass. Considering a ceasefire is in place, spending that much is unlikely, but something closer to $1 trillion is possible.

Where This Fund Belongs in a Portfolio

ITA works best as a tactical sector allocation, not a core holding. A 5% to 10% position gives investors meaningful exposure to the defense spending cycle without making the portfolio hostage to single-contractor execution risk or congressional budget negotiations. The fund’s 0.3% dividend yield is minimal, so income investors should not expect much cash flow. The value here is capital appreciation tied to a structural spending shift that just received its most explicit political endorsement yet.

Geopolitical catalysts can cut both ways in the short term, and the fund’s concentration in a handful of large contractors means company-specific stumbles will show up in the portfolio quickly.