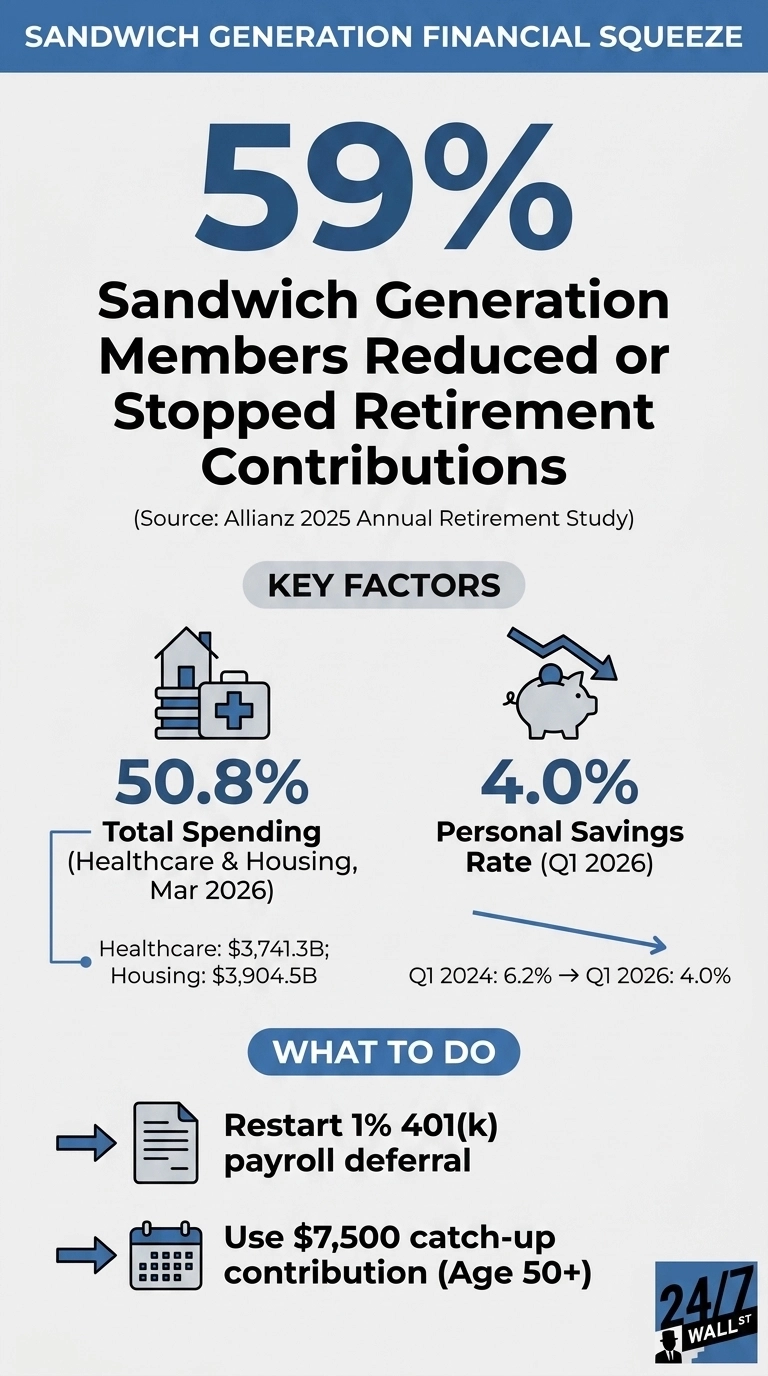

The Allianz 2025 Annual Retirement Study put a number on something that millions of households already feel in their bank accounts: 59% of members of the sandwich generation have reduced or stopped contributing to retirement savings to care for children and aging parents simultaneously. This is the real headline figure, as caregiving is emotionally taxing and a line item that is quietly draining the retirement accounts of working-age Americans in their 40s and 50s.

The Allianz survey, based on 1,000 nationally representative respondents fielded in January and February 2025, defines the group narrowly. These are people with at least one child under 18 and at least one living parent or parent-in-law. Within that group, 78% are providing financial, emotional, or physical support to their parents. The choice between saving and caregiving is concrete here. They are writing checks, taking time off work, and watching their 401(k) deferral rate slide because the household budget no longer has slack.

The retirement damage is already done

The Allianz numbers describe a slow-motion shortfall, with 70% of sandwich generation respondents saying the dual responsibility has significantly impacted their retirement plans, and 65% worry they will not have enough money to retire because of it. The more striking figure sits underneath: 40% say caregiving has derailed their retirement strategy entirely. Derailed is a strong word, and the survey uses it deliberately. These households are behind by more than a year or two. They are restructuring what retirement will look like, if it happens at all.

The broader stress shows up in how people describe their finances: 75% of members of the sandwich generation say they struggle to balance all their financial needs and goals. That is three out of four households telling a researcher, on the record, that the math no longer works.

The economic backdrop is making it worse

National savings data ultimately tells the same story when you zoom out. The personal savings rate has slipped from 6.2% in the first quarter of 2024 to 4% in the first quarter of 2026, even as disposable income continued to rise over that period. Americans are bringing in more money on paper but setting aside less of it, and total personal saving in dollar terms has moved lower as well. The gap between what households earn and what they save is being absorbed by spending that is hard to trim.

Most of that spending shows up in two places, which the sandwich generation simply cannot avoid. Housing and healthcare together make up just over half of all personal consumption, and both categories have been climbing steadily. Healthcare alone has added hundreds of billions of dollars in a little over a year, a rise driven by the everyday realities of elder care, prescriptions, copays, and the growing cost of assisted living. These are not discretionary expenses. They are the bills that arrive whether a household feels ready for them or not, and they are the ones that keep tightening the monthly budget for anyone supporting both children and aging parents.

Services inflation, which captures most caregiving costs, has stayed stubbornly elevated. The PCE services index rose 3.38% year over year in March 2026, and core PCE increased 3.2% over the same period. Wage gains have helped, but have not fully closed the gap. Average hourly earnings reached $37.41 in April 2026, yet consumer sentiment remains strained. The University of Michigan index registered 48.2 in May 2026, down from 56.6 a month earlier and still sitting deep in pessimistic territory.

What the data says, and what it does not

The Federal Reserve has begun easing, with the federal funds target upper bound at 3.75% as of May 12, 2026, down 75 basis points from a year earlier. Cheaper debt service helps at the margin. It does not refill a 401(k) that stopped receiving contributions three years ago.

For households inside the squeeze, the practical levers are narrow but real. Restarting even a 1% payroll deferral keeps the account active and captures any employer match left on the table. Workers 50 and older can use the catch-up contribution, which adds $7,500 per year to the standard 401(k) limit. Formalizing elder-care arrangements with siblings, including written cost-sharing, prevents one household from absorbing the full bill by default.

The honest read of the Allianz data is that caregiving is acting as a tax on retirement security for a specific demographic, and the economic backdrop of elevated service inflation and a 4% national savings rate is reinforcing the squeeze rather than alleviating it. The 59% who have already cut retirement contributions are behind for structural reasons. The structure of middle-aged caregiving in the United States has shifted faster than household balance sheets can absorb.

Contact [email protected] for any questions or corrections.