On a recent All-In Podcast episode discussed one of the biggest unresolved questions in the AI boom: Are companies actually generating meaningful returns from AI spending, or is Wall Street still pricing in future benefits that have yet to show up in the real economy?

Chamath Palihapitiya, Jason Calacanis, David Sacks, and Altimeter Capital founder Brad Gerstner openly split on the answer. Chamath laid out the clearest line in the sand, arguing that he expects that within roughly 500 days, companies will need to prove AI spending is translating into measurable economic returns.

Chamath’s “Fork in the Road”

Chamath warned of a “fork in the road” in roughly 500 days, when companies will have to show that AI spending has generated AI revenue. His framing was blunt: “There is literally not a scintilla of evidence that AI has helped lift the operating margins of the S&P 500.” He expects that companies will need to eventually show “I spent X and I made Y, where Y is now greater than X.” In his view, the proof should ultimately appear in hard economic metrics like S&P 500 operating margins, global productivity growth, or GDP itself.

The Attribution Debate

Brad Gerstner pushed back by pointing to improving corporate profitability across the market. He noted that S&P 500 operating margins expanded from roughly 11% in 2023 to 13% in 2025, arguing that AI likely deserves at least some credit for the improvement. But Chamath argued the margin expansion mostly reflects post-COVID restructuring, layoffs, and tighter cost discipline across corporate America rather than meaningful AI productivity gains. “I bet you dollars to donuts it’s not AI,” he said.

Jason Calacanis took the opposite side, focusing on what he sees happening operationally within startups and smaller companies today. “I’ve got 3 people on the team who are making all the interfaces and products that a 22-person investment firm should not be making internally,” Calacanis said, describing AI ROI as effectively a “fait accompli.” The MAG5 collectively grew headcount by just 3% over the last three years despite massive revenue expansion, while cloud infrastructure growth tied to AI continues to accelerate.

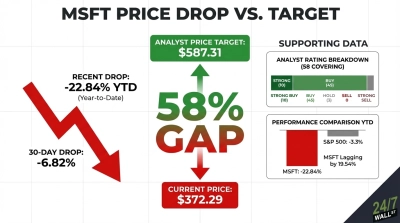

ROI Is Already Showing Up for Microsoft and Alphabet

Microsoft (NASDAQ:MSFT | MSFT Price Prediction) reported its Q3 FY2026 results on April 29, 2026, with revenue of $82.886 billion, up 18.3% YoY, EPS of $4.27, and an AI annual revenue run rate of $37 billion, up 123% YoY. Commercial RPO sits at $627 billion, up 99% YoY. Capex was $30.876 billion, up 84.39% YoY. Shares trade at $415.12, down 13.97% YTD. The spending side remains enormous. Microsoft’s capex rose 84% year over year to nearly $31 billion as the company continues racing to build enough AI infrastructure capacity.

Additionally, Alphabet (NASDAQ:GOOGL) posted Q1 FY2026 revenue of $109.896 billion, up 21.79% YoY, with Google Cloud at $20.028 billion, up 63%, and backlog over $460 billion. Capex doubled to $35.674 billion, up 107.44% YoY, compressing free cash flow by 46.63%. Shares are up 28.14% YTD at $400.80. At the same time, capex more than doubled year over year to $35.7 billion, compressing free cash flow by nearly 47%.

Sacks’ Middle-Ground View

David Sacks largely framed the disagreement as a matter of timing rather than a fundamental disagreement over whether AI will matter. He described AI ROI as “trickling down from infrastructure to model to application to end user,” arguing the productivity gains may simply take longer to fully appear across the economy.

Contact [email protected] for any questions or corrections.