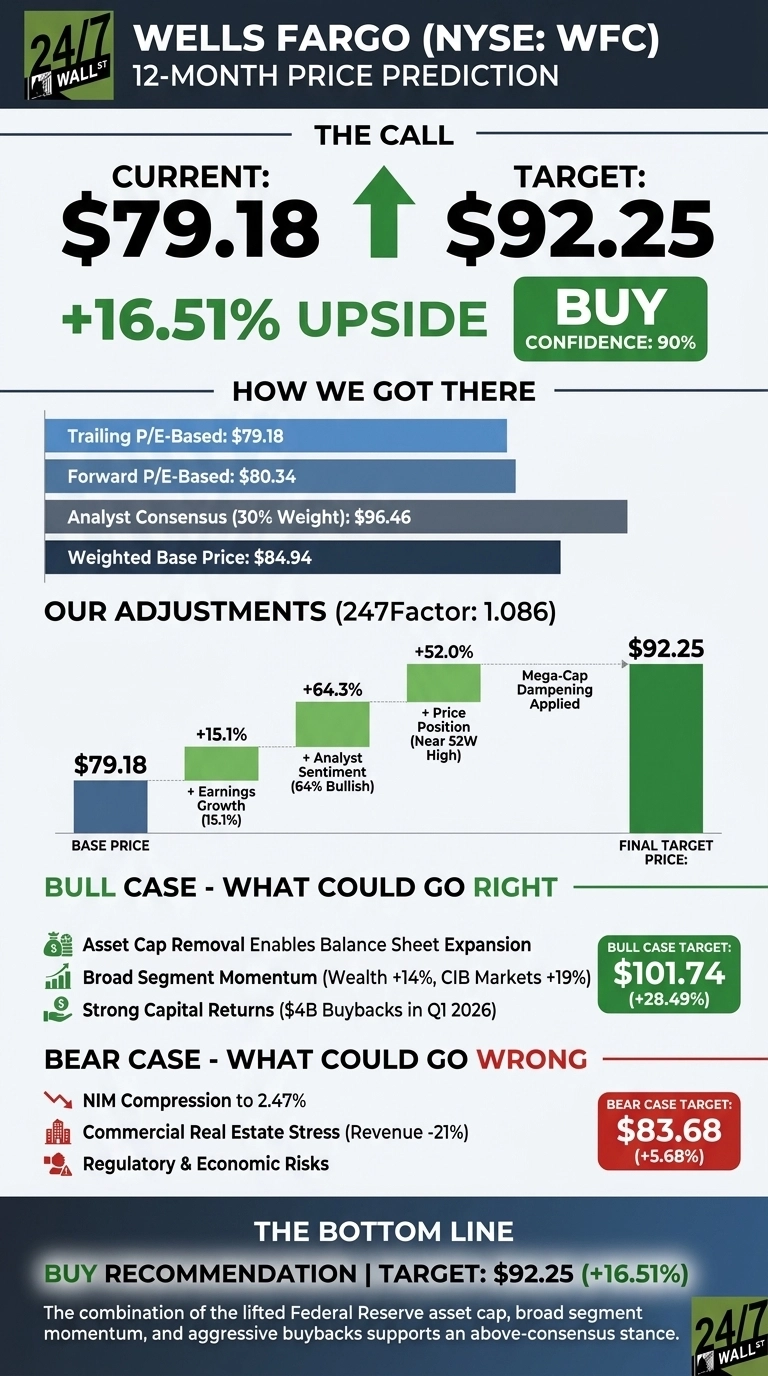

I am opening with the bottom line. Wells Fargo (NYSE:WFC | WFC Price Prediction) trades at $79.18 as of May 4, 2026, and our price target for Wells Fargo is $92.25 over the next 12 months. That implies 16.51% upside, and we rate the stock a buy with a confidence level of 90%. The combination of the lifted Federal Reserve asset cap, broad segment momentum, and aggressive buybacks supports an above-consensus stance.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $79.18 |

| 24/7 Wall St. Price Target | $92.25 |

| Upside | 16.51% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Rough Start to 2026 After a Banner 2025

Wells Fargo has been a tale of two periods. Shares are down 14.64% year to date after starting 2026 at $92.76, with a sharp pullback in March to $75.75 driving most of the damage. Over one year the stock is still up 9.6%, and over five years it has returned 93.76%.

Q1 2026 results, released April 14, 2026, showed EPS of $1.60 on revenue of $21.44 billion, with 15% diluted EPS growth and 11% loan growth. The stock still fell 5.7% after the earnings report as investors fixated on net interest margin compression to 2.47% from 2.67%.

Why Bulls See a Breakout to $100+

The bull case rests on the asset cap removal in 2025, which finally lets Wells Fargo expand its balance sheet after years of regulatory constraint. Q1 2026 already showed period-end loans crossing $1 trillion for the first time since 2020. Segment performance is broad: CIB Markets revenue grew 19%, Wealth and Investment Management 14%, and credit card new accounts surged nearly 60% YoY.

CEO Charlie Scharf reaffirmed the medium-term ROTCE target of 17% to 18%, saying “We feel as confident as ever in that target.” Our bull-case scenario points to $101.74, a 28.49% total return. The Wall Street consensus target of $96.46 sits in the same neighborhood, with 18 buy ratings against 10 holds and zero sells.

What Could Go Wrong

The bear case starts with the 2.47% NIM, which CFO Michael Santomassimo said could compress further. The CET1 ratio fell to 10.3% from 11.1% a year ago, CIB Commercial Real Estate revenue dropped 21%, and credit card delinquencies sit at 2.77%. Higher oil prices could pressure lower-income consumer spending, with Scharf warning the impact “will likely take some time to materialize.”

Bulls would counter that the CET1 decline came alongside $5.4 billion returned to shareholders in the quarter, and that NIM compression partly reflects deliberate growth in lower-ROA Markets assets. Our bear-case scenario still lands at $83.68, a 5.68% return.

Our Take on Wells Fargo Here

The 24/7 Wall St. price target of $92.25 backs a buy at 90% confidence. The tipping factor is the post-asset-cap growth runway combined with shareholder returns of $23 billion in 2025. The bull thesis stays intact if loan growth holds at mid-single digits and the ROTCE target is reaffirmed. The thesis weakens if NIM falls below 2.40% and credit card delinquencies push past 3%.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $92.25 |

| 2030 | $128.96 |

These projections assume Wells Fargo continues executing on the 17% to 18% ROTCE plan. Significant upside or downside could come from M&A activity, regulatory changes around Basel III, or a sharp credit cycle turn.

Contact [email protected] for any questions or corrections.