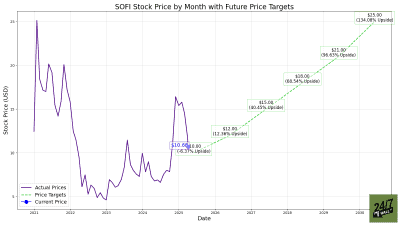

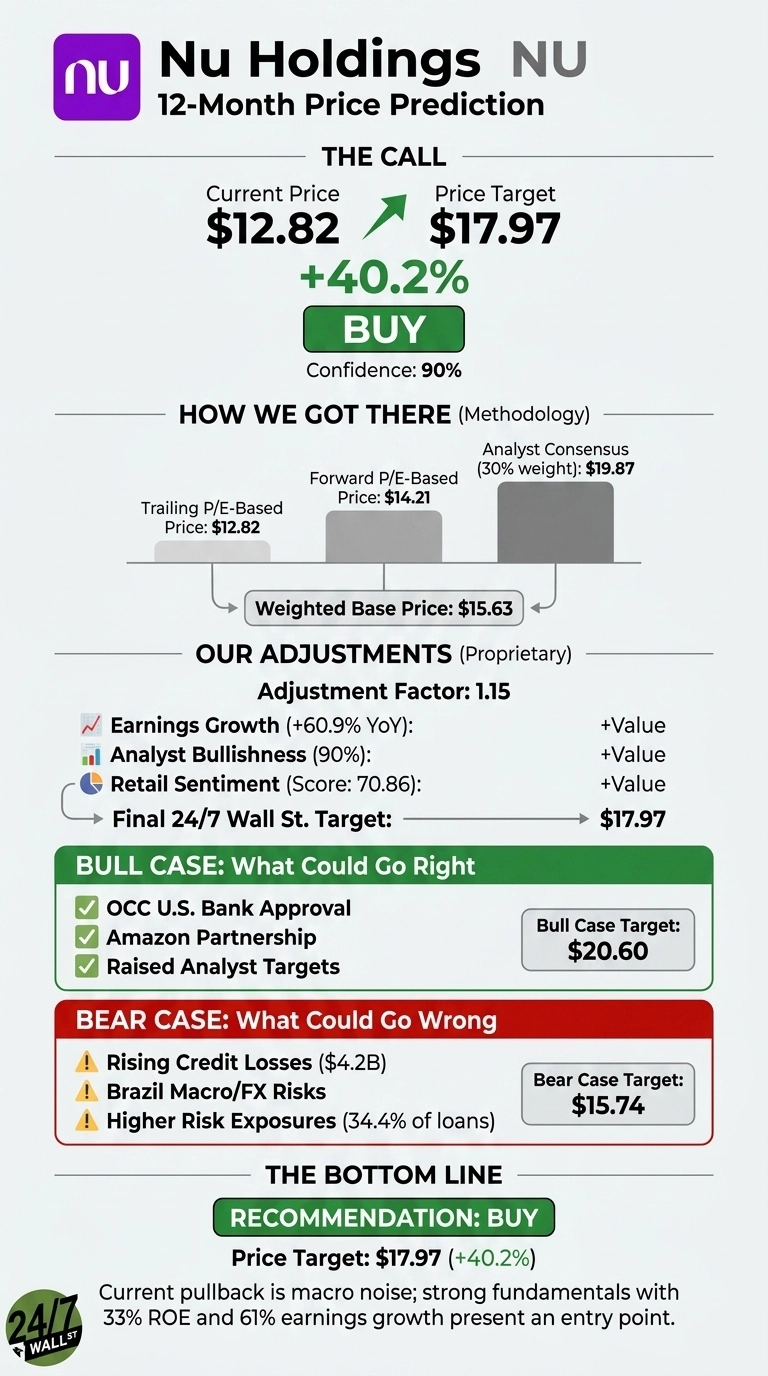

Our 24/7 Wall St. price target for Nu Holdings (NYSE:NU | NU Price Prediction) is $17.97, pointing to 40.2% upside from the current $12.82 share price. We rate the Latin American neobank a buy with a 90% confidence level. NU has pulled back sharply from its February peak, and our proprietary model reads that dislocation as an entry point on an intact thesis.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $12.82 |

| 24/7 Wall St. Price Target | $17.97 |

| Upside | 40.2% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Brutal Spring Sets Up Today’s Earnings Report

NU shares are down 11.46% over the past week, 14.25% over the past month, and 23.42% year to date, sliding from a February high near $18.98 toward the 52-week low of $11.71. The selloff tracks Brazil’s economic slowdown, high interest rates, and rising loan loss provisions rather than any change in the underlying franchise.

Fundamentals tell a different story. Nu closed 2025 with a record Q4 net income of $895 million, full-year net income of $2.87 billion (+45.61% YoY), FY2025 revenue of $15.77 billion (+42.06% YoY), and return on equity of 33%. The customer base reached 131 million across Latin America. Q1 2026 results are due after the close on May 14, 2026, making this the most important catalyst of the quarter.

Why Bulls See a Breakout to $20+

Bulls have the more interesting story. The OCC granted conditional approval in January 2026 for a Nubank N.A. U.S. national bank, opening deposits, lending, and digital-asset custody in the largest banking market. The Amazon Brazil partnership announced in late November 2025 widens distribution materially.

Loans to customers nearly doubled to $10.92 billion, deposits jumped to $41.9 billion, and secured lending grew to $2.7 billion from $1.4 billion. Susquehanna, JPMorgan, and KeyBanc have all raised price targets. The Street consensus sits at $19.87 with 19 buy ratings against 2 holds and zero sells. Our bull-case scenario points to $20.60 in a year.

What Could Go Wrong

Credit quality is the swing variable. Expected credit losses climbed to $4.20 billion from $3.17 billion, and 22.9% of credit card exposures and 34.4% of loan exposures are classified Higher Risk. The capital adequacy ratio slipped to 16.6% from 18.1%.

Brazilian real volatility and CSLL tax rate changes add macro overhang. Morningstar values NU at $15.30 with a Narrow Moat rating, and UBS sits at $16 Neutral. The rising loss provisions reflect a loan book that nearly doubled in size, and our bear-case scenario still produces $15.74, a 22.78% gain from here.

I’d Be a Buyer Here

The 24/7 Wall St. price target of $17.97 and buy rating reflect 90% confidence that the current pullback is macro noise on a 33% ROE franchise. The tipping factor is the disconnect between a stock down 23.42% YTD and earnings growing nearly 61% YoY.

I’d be a buyer if tonight’s Q1 earnings report confirms continued customer growth past 131 million and stable credit metrics. I’d stay sidelined if Higher Risk loan exposures push past 35% or the capital adequacy ratio breaks below 16%.

Here is where our model projects NU could trade, assuming the company compounds earnings near its 5-year base case annualized return of 20.74%.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $17.97 |

| 2027 | $18.69 |

| 2028 | $22.57 |

| 2029 | $27.25 |

| 2030 | $32.89 |

These projections assume Nu Holdings executes on Latin American expansion and the U.S. national bank rollout. Significant upside could come from successful Mexico and Colombia monetization, while downside risk centers on Brazilian credit cycle deterioration.

Contact [email protected] for any questions or corrections.