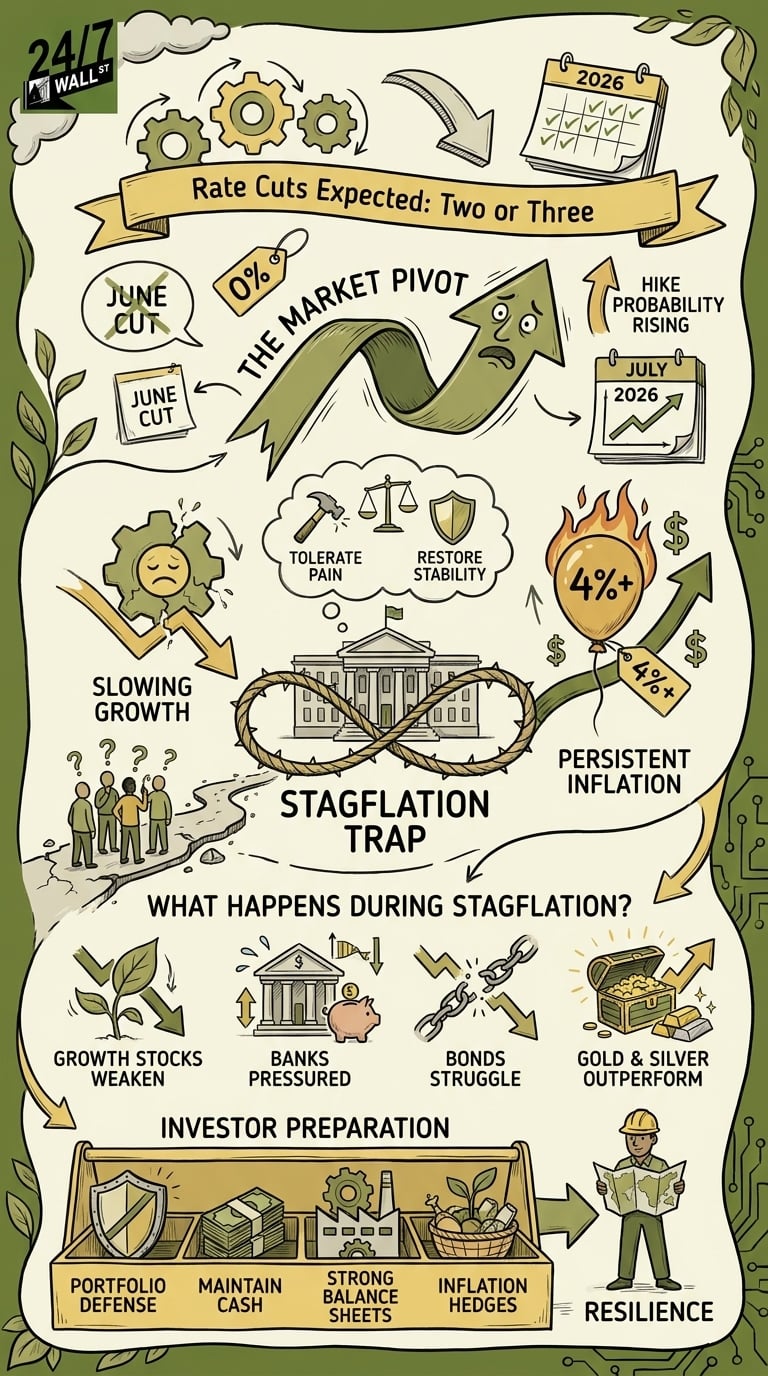

For most of 2026, Wall Street treated Federal Reserve rate cuts as inevitable. The only debate was whether investors would get two cuts or three. Bond traders, stock investors, and mortgage borrowers all built their expectations around the idea that inflation was cooling enough for the Fed to ride to the rescue.

Now, that entire narrative is unraveling. Markets have moved from confidently pricing multiple rate cuts to hoping the Fed simply avoids raising rates again. And that shift says a lot about where the U.S. economy may be heading next — toward a painful period of stagflation where inflation stays elevated even as growth slows and unemployment rises.

That’s a nasty combination because the Federal Reserve has very few painless solutions when both problems hit at the same time.

The Market’s Fed Pivot Just Reversed

The change in expectations has been dramatic. Earlier this year, futures traders expected as many as three quarter-point cuts from the Fed in 2026. Then expectations slipped to two cuts. Today, according to the CME FedWatch Tool, the odds of a June rate cut have collapsed below 1%.

Even after Kevin Warsh was confirmed as the next Federal Reserve chair this morning, markets still expect rates to stay exactly where they are at the June meeting. Futures pricing shows rate-cut probabilities remaining below 1% for much of the next year, while odds of hikes begin climbing starting with the July 2026 meeting. By January, markets see higher odds of a hike than keeping rates steady.

Prediction markets are sending the same message. Kalshi traders currently assign roughly a 68% probability that the Fed delivers no cuts at all this year, while indicating a 50% chance of a hike happening before July 2027.

In short, investors are no longer debating how quickly rates will fall. They’re debating whether the Fed may need to tighten policy again.

The Economy Is Starting to Look Like 1970s Stagflation

Why the sudden shift? Because the economic data increasingly resembles the early stages of stagflation.

Inflation has climbed back to its highest level since 2023. Consumer confidence is at an all-time low. Labor-market data, while still resilient on the surface, has started showing cracks beneath the headline numbers as hiring slows and layoffs creep higher. That’s a dangerous setup.

Normally, the Fed cuts rates when the economy weakens. But when inflation remains stubbornly high, policymakers can’t easily stimulate growth without risking another inflation surge. The Fed may have to choose which pain hurts less.

The comparison many economists increasingly whisper about is former Fed Chair Paul Volcker, who raised interest rates aggressively in the early 1980s to crush runaway inflation. Those hikes eventually worked, but they also triggered recessions and unemployment above 10%.

Granted, today’s inflation problem is nowhere near the double-digit levels of that era. But the policy dilemma feels familiar. If inflation stays sticky near 4% while growth slows, the Fed may tolerate economic weakness longer than investors expect.

Surprisingly, the bond market already appears to be pricing in that possibility. Treasury yields have climbed despite softer economic growth forecasts, with long-term yields pushing higher as investors demand more compensation for inflation risk.

Why Investors Should Prepare Now

If this stagflation scenario gains traction, several parts of the market could come under pressure simultaneously.

Stocks typically struggle because corporate earnings weaken while higher rates reduce valuation multiples. Banks can also face stress if the yield curve inverts, squeezing lending profits while loan defaults rise.

Here’s what tends to happen during stagflationary periods:

| Asset Class | Typical Performance During Stagflation |

| Growth stocks | Weakens as valuations compress |

| Banks | Pressured by inverted yield curves |

| Bonds | Struggle if inflation remains elevated |

| Gold & silver | Often outperform |

| Energy & commodities | Can remain resilient |

Gold has already climbed far above historic levels while silver has outpaced gold’s rise. That’s not random. Precious metals historically perform well when investors lose confidence in both economic growth and central-bank flexibility.

That said, investors do not need to panic. They need to prepare. This is an environment where portfolio defense matters more than aggressive speculation. Maintaining higher cash allocations, emphasizing profitable companies with strong balance sheets, reducing exposure to highly leveraged businesses, and owning some inflation hedges may prove valuable over the next several quarters.

Key Takeaway

The market’s outlook for Federal Reserve policy has flipped in just a few months. Investors started 2026 expecting multiple rate cuts. Now futures traders increasingly believe the next move may eventually be a hike instead.

That shift reflects growing fears that the U.S. economy is entering a stagflationary phase — slowing growth paired with persistent inflation. If that happens, the Fed may face a Volcker-style choice: tolerate economic pain now to restore price stability later.

When all is said and done, smart investors should not focus on predicting every Fed meeting. They should focus on building portfolios sturdy enough to survive an environment where both inflation and economic weakness linger longer than Wall Street expected.

Contact [email protected] for any questions or corrections.