At $460.52, Microsoft (NASDAQ:MSFT | MSFT Price Prediction) is a Hold over the next 12 months, with a reasonable target near $560 if AI monetization compounds. The stock is a fortress business priced like one, and the debate is whether cloud dominance justifies a historic valuation premium.

Microsoft owns the productivity stack, the second-largest public cloud, and a deep partnership with OpenAI that extends royalty-free IP access through 2032. Azure drives the multi-year growth story, while Microsoft 365 generates high-margin recurring revenue.

The stock pulled back from its 52-week high of $551.05 as investors digested an aggressive AI capex cycle. After a recent bounce, the question is whether to chase or wait.

Why the bulls see a generational compounder

The cloud and AI engine is firing. Q3 FY26 revenue grew 18.3% to $82.886 billion, with Azure up 40% and Intelligent Cloud up 30%. CEO Satya Nadella said the “AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.”

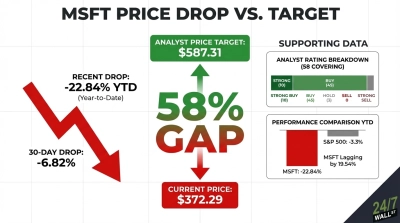

Commercial RPO hit $627 billion, up 99% YoY, providing years of revenue visibility. Margins remain elite, with operating margins above 45% and ROIC near 21%. Wall Street is overwhelmingly positive, with 52 Buy or Strong Buy ratings versus 3 Holds and zero Sells.

Why the bears say the price has run ahead of reality

The valuation leaves no room for error. Trailing P/E sits near 27, forward P/E around 23, and P/FCF stretches to roughly 48 as capex compresses free cash flow. FY25 free cash flow fell 3.32% even as revenue grew 14.93%.

Q3 capex jumped 84% YoY to $30.876 billion, and management guided calendar 2026 spend to roughly $190 billion. The OpenAI investment generated a $3.1 billion quarterly loss. Insider activity skews toward net selling, and Reddit chatter has fixated on the Gates Foundation exiting its remaining MSFT stake.

Why patience may be the smartest trade

This is an elite business at a full price. The bull thesis requires AI monetization to compound fast enough to absorb a $190 billion annual capex bill. The bear thesis requires a slowdown not yet visible in the numbers. Both could be partially right.

The composite prediction sentiment score is 67.77, bullish with medium confidence, yet Polymarket traders assigned an 80.5% probability to a down day heading into June. Markets are pricing consolidation rather than a breakout.

What the numbers actually say

Shares trade at $460.52 against an analyst consensus target of $560.63, implying roughly 21.7% upside across 55 covering analysts.

Performance has lagged badly. MSFT is down 4.35% year to date and up just 0.84% over the past year, while the S&P 500 has gained 11.24% YTD and 28.7% over twelve months. A 11.36% one-month rally closed part of the gap.

The verdict on Microsoft at $460

At $460.52, Microsoft is a Hold.

The business is performing flawlessly, but the price reflects most of the near-term AI monetization narrative. Forward P/E of 23 on a company guiding to 13% to 15% Q4 revenue growth is fair, especially with capex set to exceed $40 billion next quarter.

Existing shareholders own one of the highest-quality compounders in the market, with ROE above 33% and a debt-to-equity ratio of 0.176. New capital deserves a better entry point. A pullback toward the $402 fifty-day moving average would offer more attractive risk/reward.

Watch Azure growth, FY27 operating margin guidance, and any signal that the $627 billion RPO is converting to revenue faster than capex is depreciating. A reacceleration above the forecasted 39% to 40% Azure constant-currency growth tips this to a Buy. A miss on monetization tips it to a Sell.

The fortress quality is intact, but the moat may be priced more generously at a better entry point.

Contact [email protected] for any questions or corrections.