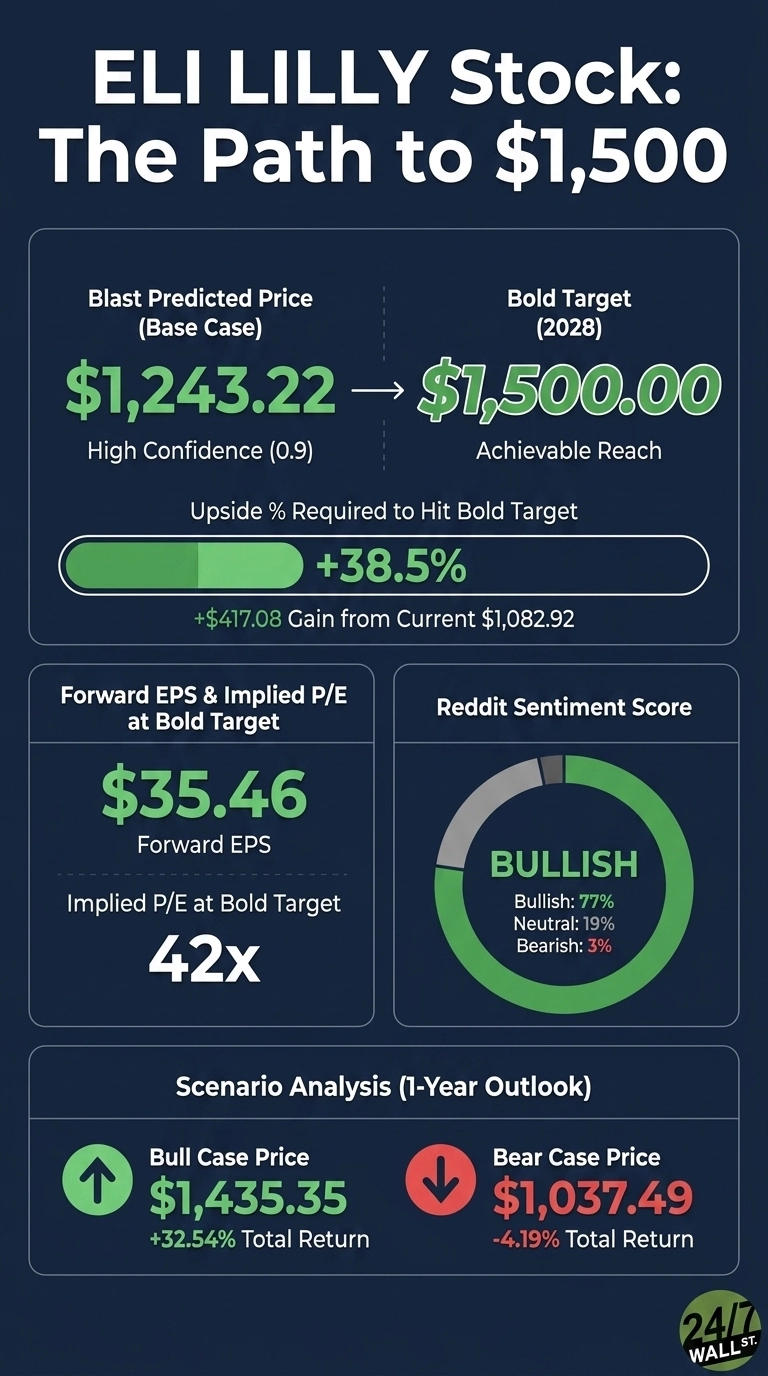

Eli Lilly (NYSE:LLY | LLY Price Prediction) just grew revenue 55.5% in a single quarter while raising full-year guidance to $82 billion to $85 billion. Mounjaro and Zepbound combined for $12.8 billion in Q1 alone. Yet shares are up just 1.11% year to date, sitting at $1,082.92. Can LLY reach $1,500 a share by 2028?

Why Lilly Shares Have Stalled in 2026

Fundamentals are accelerating while the stock is flat. LLY is up 6.29% over the past week and 24.94% over the past month, recovering ground lost during the early-2026 pullback from the December high near $1,062.

The drag is pricing. Realized prices fell 13% in Q1 as Mounjaro entered China’s reimbursement list and Zepbound cash-pay tiers declined. Management guided to a low-to-mid-teens price headwind for the full year. Investors are also digesting $584M in IPR&D charges tied to four acquisitions and $279M in litigation charges. With a beta of 0.481, this is a quality compounder waiting for the market to focus on volume.

Wall Street Sees 12% Upside. I Think That’s Too Cautious.

The analyst consensus target sits at $1,215.10, with 6 strong buys, 18 buys, 6 holds, and 1 sell. Our internal base case lands at $1,243.22 with high confidence (0.9), and a bull-case 12-month read of $1,435.35.

Consensus is anchored to 2026 numbers and largely ignores the 2028 setup. With 77% bullish sentiment, Q1 EPS growth of 169.9% year over year, and Foundayo’s oral GLP-1 launch only starting to ramp, analysts will need to mark up out-year models.

The Path to $1,500 Per Share

Reaching $1,500 from today’s price of $1,082.92 would require a gain of 38.5%. With forward EPS of $35.46, a price of $1,500 implies a forward P/E of 42x. Our base case of $1,243.22 already implies 37x, meaning the bold target requires roughly 5x additional multiple expansion or equivalent EPS upside.

That is achievable on two fronts. First, EPS. Management raised the 2026 EPS range to $35.5 to $37. With 42 active Phase III programs, retatrutide weight loss of 25 to 37 pounds in TRANSCEND, and Foundayo opening over 1 billion people with obesity worldwide, 2028 EPS in the mid-$40s is plausible.

Second, the multiple. CEO Dave Ricks framed the international setup directly: “Oral GLP-1s for obesity have not yet been introduced outside the U.S.” Four directors purchased shares on three separate occasions at prices between $919 and $989.

The primary risk is a U.S. obesity pricing reset that compresses both volume economics and the multiple.

Where Lilly Trades Today vs Its Earnings Power

At $1,082.92, LLY trades at a forward P/E of 31x against forward EPS of $35.46. Shares sit just below the 52-week high of $1,130.12 and well above the low of $619.40. The ten-year return is 1,596.87%. For a stock compounding earnings at this rate, 31x forward is reasonable.

Is $1,500 Realistic? My Verdict

$1,500 by 2028 requires a 38.5% gain from here. It’s a credible reach.

Three things need to go right: Foundayo scales internationally, retatrutide delivers a clean Phase III obesity readout, and the Medicare bridge converts into broader Part D participation in 2028 as Ricks expects.

A sharp regulatory shift on GLP-1 pricing would derail it. We’ve outlined the blueprint for how Eli Lilly could reach $1,500 in 2028.