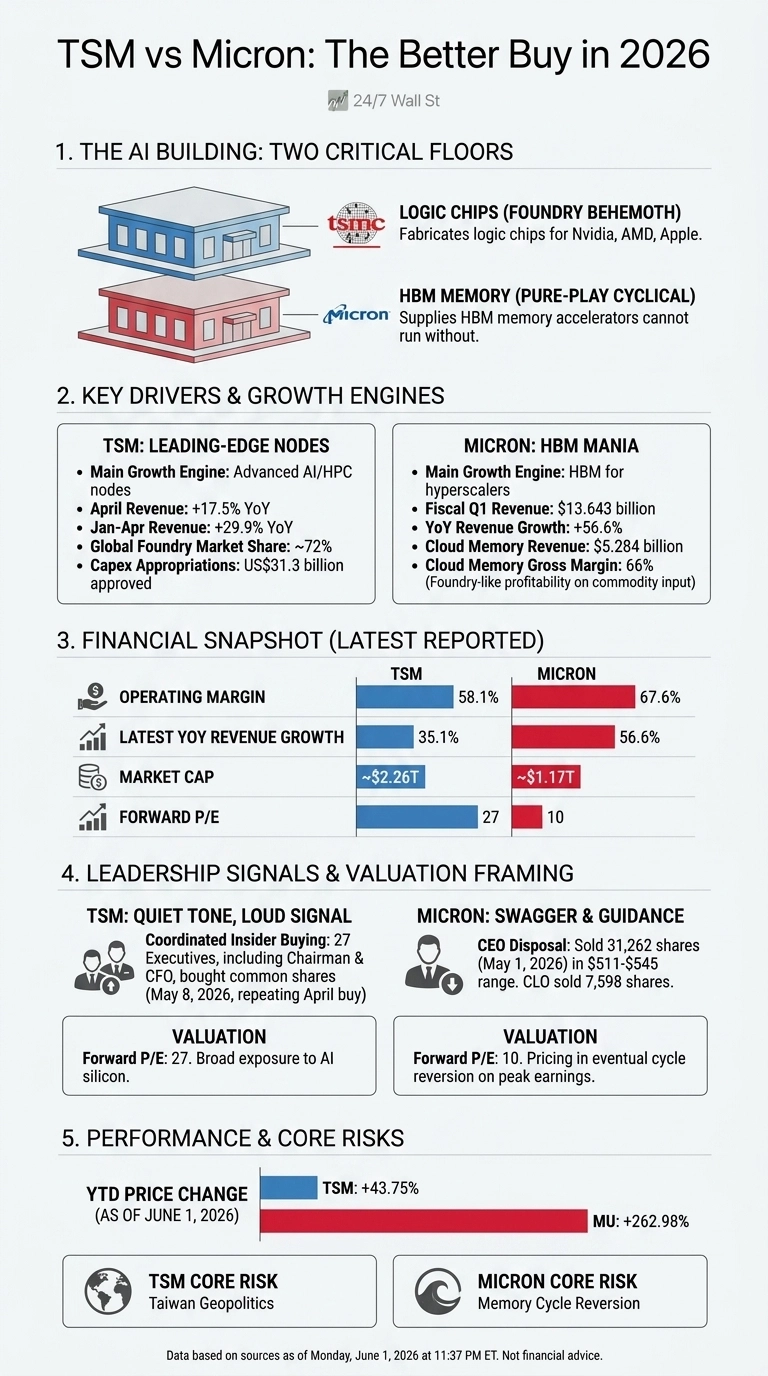

Taiwan Semiconductor Manufacturing (NYSE:TSM | TSM Price Prediction) and Micron Technology (NASDAQ:MU) sit at two different floors of the same AI building.

TSMC fabricates the logic chips that power Nvidia, AMD, and Apple. Micron supplies the HBM memory those accelerators cannot run without. Both just delivered blowout numbers, and the contrast between a foundry behemoth and a pure-play memory cyclical has rarely been sharper.

HBM Mania Carries Micron. Leading-Edge Nodes Carry TSMC.

Micron’s fiscal Q1 was the kind of quarter memory bulls have waited a decade for. Revenue hit $13.643 billion, beating estimates by 5.91%, while non-GAAP EPS of $4.78 crushed the $3.94 consensus. The Cloud Memory Business Unit alone generated $5.28 billion at a 66% gross margin. That is foundry-like profitability on a commodity input, which tells you how tight HBM supply really is.

TSMC’s story reads more like infrastructure than cyclicality. April revenue rose 17.5% year over year, and cumulative January through April sales grew 29.9%. The board signed off on roughly US$31.3 billion in capital appropriations and authorized up to US$20 billion for TSMC Arizona. With 72% global foundry market share, the company is effectively the toll booth for advanced silicon.

| Business Driver | TSMC | Micron |

| Main growth engine | Leading-edge AI/HPC nodes | HBM for hyperscalers |

| Latest YoY revenue growth | 35.1% | 56.6% |

| Operating margin | 58.1% | 67.6% |

Foundry Toll Booth Versus Memory Supercycle

CEO Sanjay Mehrotra told investors Micron’s Q2 outlook reflects “substantial records across revenue, gross margin, EPS and free cash flow.” Guidance backs the swagger: $18.70 billion in revenue and $8.42 EPS for the next quarter, with order books reportedly stretching into 2027.

TSMC’s tone is quieter but the signal louder. Twenty-seven executives, including Chairman C.C. Wei and the CFO, bought common shares together on May 8, 2026, repeating a coordinated buy from April.

Micron insiders did the opposite: CEO Mehrotra disposed of 31,262 shares on May 1 in the $511 to $545 range, and the Chief Legal Officer unloaded another 7,598 shares.

| Lens | TSM | MU |

| Forward P/E | 27 | 10 |

| YTD price change | 43.75% | 262.98% |

| Core risk | Taiwan geopolitics | Memory cycle reversion |

The Next Test Is Whether Memory Pricing Holds

Micron’s 998.9% one-year return already prices in a long supercycle. I will be watching whether HBM4 ramps cleanly and whether DRAM contract pricing stays firm into calendar 2027. For TSMC, the Arizona buildout and the pace of 2nm conversions matter more than any single quarter, especially with capex commitments now in the tens of billions.

How the Two Setups Compare

TSMC offers broader exposure to AI silicon through its foundry position, trades at a forward multiple of 27, and has seen coordinated insider buying. Micron’s setup looks spectacular today, yet a forward P/E near 10 on peak-cycle earnings reflects the market pricing in eventual cycle reversion.

The Micron thesis hinges on HBM scarcity persisting through 2027, while TSMC’s case rests on continued leading-edge node dominance regardless of memory pricing. Investors should weigh the 90.98% one-month move in Micron when assessing entry risk.

Contact [email protected] for any questions or corrections.