Apple (NASDAQ:AAPL | AAPL Price Prediction) has become one of the more interesting setups in mega-cap tech. After a 46.9% rally over the past year and an 8.01% year-to-date gain, the stock consolidated in June. With earnings accelerating and the iPhone 17 cycle feeding the top line, our model sees room for double-digit upside.

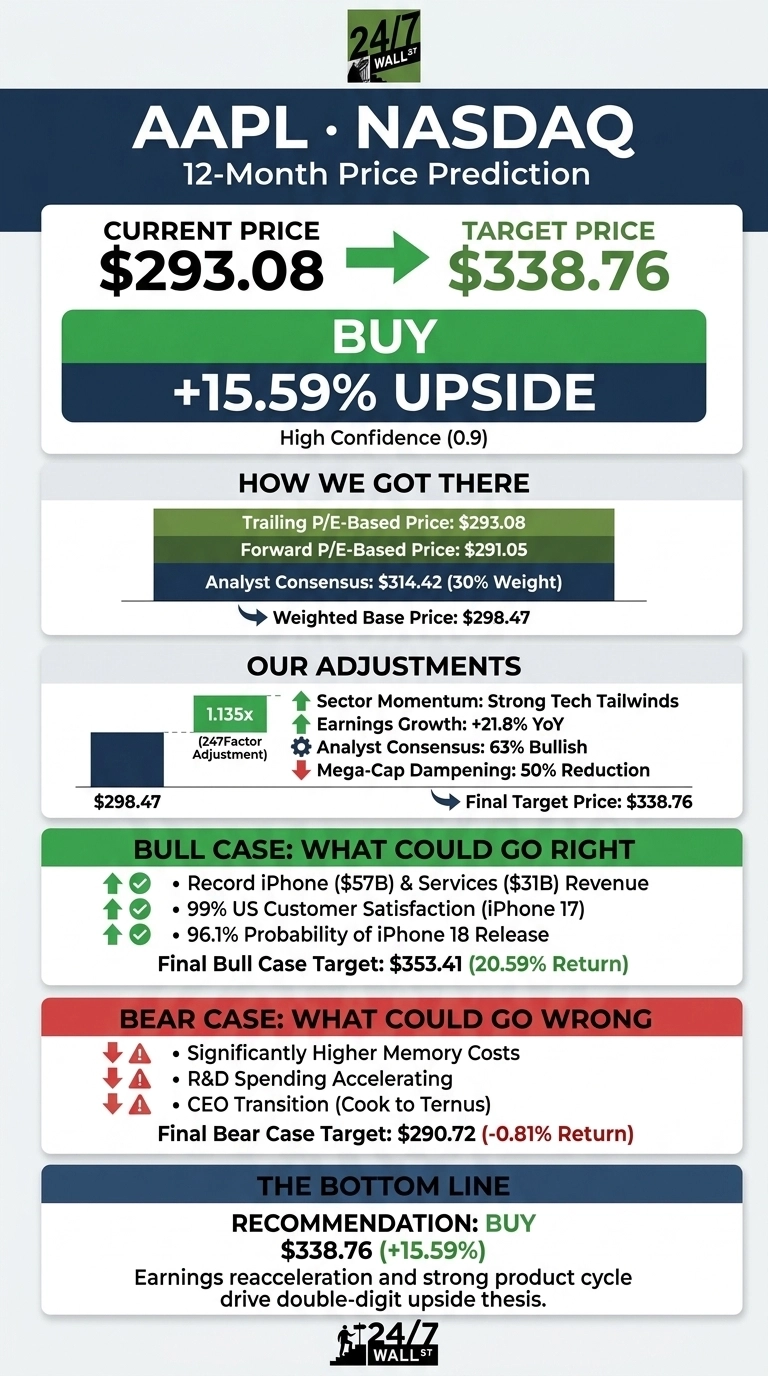

Our 24/7 Wall St. price target for Apple is $338.76, implying 15.59% upside from $293.08. The recommendation is buy, with high confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $293.08 |

| 24/7 Wall St. Price Target | $338.76 |

| Upside | 15.59% |

| Recommendation | BUY |

| Confidence Level | 90% |

An Earnings Run That Keeps Surprising to the Upside

Apple’s March quarter was its strongest in years. Revenue came in at $111.184 billion, up 16.6% year over year, with EPS of $2.01 beating the $1.94 consensus. That marked the 8th consecutive quarter of beating Wall Street estimates.

iPhone revenue hit $56.994 billion, Services set an all-time record at $30.976 billion, and gross margin expanded to 49.3%. Tim Cook called it “our best March quarter ever, with revenue of $111.2 billion and double-digit growth across every geographic segment.”

The stock pulled back from its May high near $308.82, down 5.1% over the past month. Shares sit just 1% off the 52-week high of $317.40 and well above the low of $198.47.

The Case for $353 and Higher

Bulls have plenty to work with. The iPhone 17 family was described by Cook as “the most popular lineup in our history,” with US customer satisfaction at 99%. Greater China revenue grew 28% in the March quarter, and India remains, in Cook’s words, “a huge opportunity.”

Services growth of 16% against a 2.5 billion active device base provides recurring, high-margin revenue. Prediction markets put a 96.1% probability on an iPhone 18 release this year, with foldable iPhone odds at 84.5%. Our bull case targets $353.41, a 20.59% return.

The Risks Worth Watching

Cook flagged “significantly higher memory costs” ahead and warned the impact will grow beyond June. R&D spending is accelerating well above company-wide growth, which could pressure operating leverage.

Insider activity has been net selling, with 47 transactions recently. The CEO transition, with John Ternus taking over September 1, introduces execution risk. The trailing P/E of 36 leaves little margin for a miss.

The buyback authorization of $100 billion and ongoing margin expansion to 49.3% partly offset cost worries. Our bear case lands at $290.72, essentially flat.

Apple Price Prediction 2026-2030

The 24/7 Wall St. price target of $338.76 reflects high confidence (90%) and a buy rating. The tipping factor is earnings reacceleration. Revenue growth jumped from 7.94% in Q4 FY25 to 16.6% in Q2 FY26, and gross margins keep expanding.

The bullish case strengthens if Apple delivers another double-digit revenue result in the June quarter, in line with the 14-17% guidance. The thesis weakens if memory cost pressure compresses gross margin below 47% or if China growth stalls. Right now, the setup tilts positive.

Here is where our model projects Apple could trade in the coming years, assuming current growth trajectories and market conditions hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $338.76 |

| 2027 | $370.00 |

| 2028 | $402.00 |

| 2029 | $435.00 |

| 2030 | $468.42 |

These projections assume Apple executes on the iPhone refresh cycle and Services flywheel. Significant upside or downside could result from a foldable launch, AI monetization, or a sharper geopolitical hit to China revenue.

Contact [email protected] for any questions or corrections.