Meta Platforms (NASDAQ:META | META Price Prediction) has been through the wringer. The stock is down 18.05% over the past year and 11.54% year to date, with a brutal 4.9% single-day drop on July 2, 2026. After running the numbers, the selloff looks overextended relative to fundamentals.

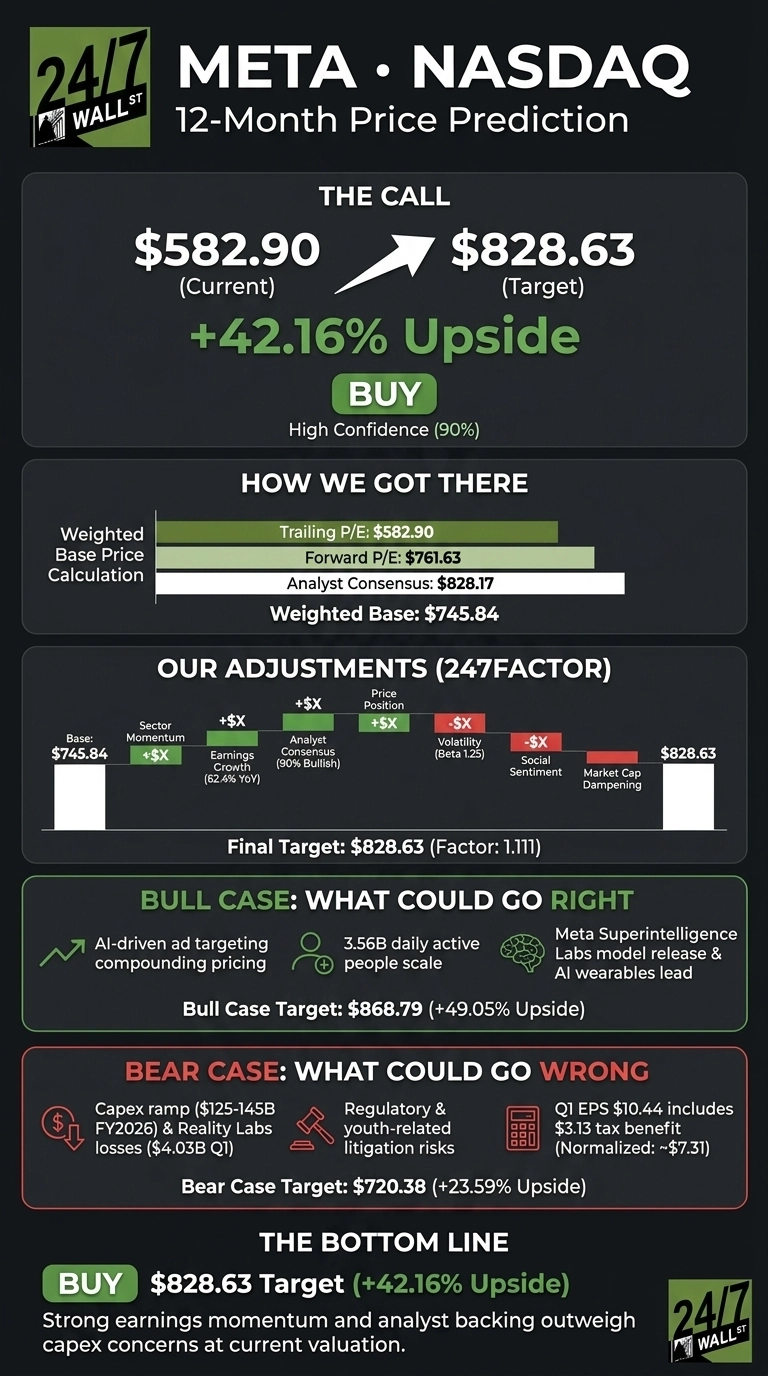

Our 24/7 Wall St. price target for Meta is $828.63, implying 42.16% upside from $582.90. The recommendation is buy, with high confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $582.90 |

| 24/7 Wall St. Price Target | $828.63 |

| Upside | 42.16% |

| Recommendation | BUY |

| Confidence Level | 90% |

How a $1.28 Trillion Giant Fell Out of Favor

Meta peaked near $785.23 in August 2025 before grinding lower into July 2026. The catalysts for the pullback were largely self-inflicted: management raised FY2026 capex guidance to $125-145 billion, up from the prior $115-135 billion range, citing higher component pricing and data center costs. Reality Labs is still bleeding, with a $4.03 billion operating loss in Q1 2026.

Yet the underlying business is roaring. Q1 2026 revenue jumped 33.1% YoY to $56.31 billion, ad impressions rose 19%, and price per ad climbed 12%. That is Meta’s fifth consecutive EPS beat. Reddit captured the mood best with a viral wallstreetbets post about “Suckerberg panic bought the entire AI chip supply,” which drew 13,591 upvotes.

The Case for $868 and Higher

The bull scenario projects $868.79, or 49.05% upside. The core drivers: Meta Superintelligence Labs released its first model in Q1, 3.56 billion daily active people across the Family of Apps, and AI-driven ad targeting that is compounding pricing power.

Ray-Ban Meta glasses give Meta the early lead in AI wearables. Of 63 analysts covering the stock, 57 rate it Buy or Strong Buy with zero sells. The forward P/E sits at just 19, a modest multiple for a business compounding earnings at this rate.

What Could Go Wrong

The bear case targets $720.38, still 23.59% above spot. Risks are real: FY2025 free cash flow fell 19.39% as capex nearly doubled, youth-related litigation trials are scheduled through 2026, and Q1’s $10.44 EPS was flattered by a $3.13 per share tax benefit from Treasury Notice 2026-7. Normalized operating EPS was closer to $7.31.

Bulls would counter that the capex ramp is building the AI infrastructure that already powered 33.1% Q1 revenue growth. Operating income still rose 30.29% YoY, and the balance sheet remains fortress-grade with interest coverage of 71x.

Meta Price Prediction 2026-2030

The 24/7 Wall St. price target of $828.63 reflects a rare setup: a mega-cap with 42.16% modeled upside, 90% confidence, and a Street that is uniformly constructive. The tie-breaker is valuation.

A 19 forward P/E on a business growing revenue at 33.1% is asymmetric. The setup strengthens if Q2 revenue lands at the high end of the $58-61 billion guide. Risks intensify if Reality Labs losses balloon or capex guidance climbs again.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $828.63 |

| 2027 | $975 |

| 2028 | $1,140 |

| 2029 | $1,335 |

| 2030 | $1,549.79 |

These projections assume Meta continues executing on AI monetization and family of apps growth. Significant upside could come from Reality Labs turning profitable; downside risk hinges on regulatory outcomes and capex discipline.

Contact [email protected] for any questions or corrections.