The question in our headline has a short answer based on our proprietary model: probably not in 2026. But the longer answer is more interesting, because the bull case scenario for DraftKings (NASDAQ:DKNG | DKNG Price Prediction) does get close to doubling within 12 months, and DKNG’s Predictions launch could reset the entire valuation conversation before year-end.

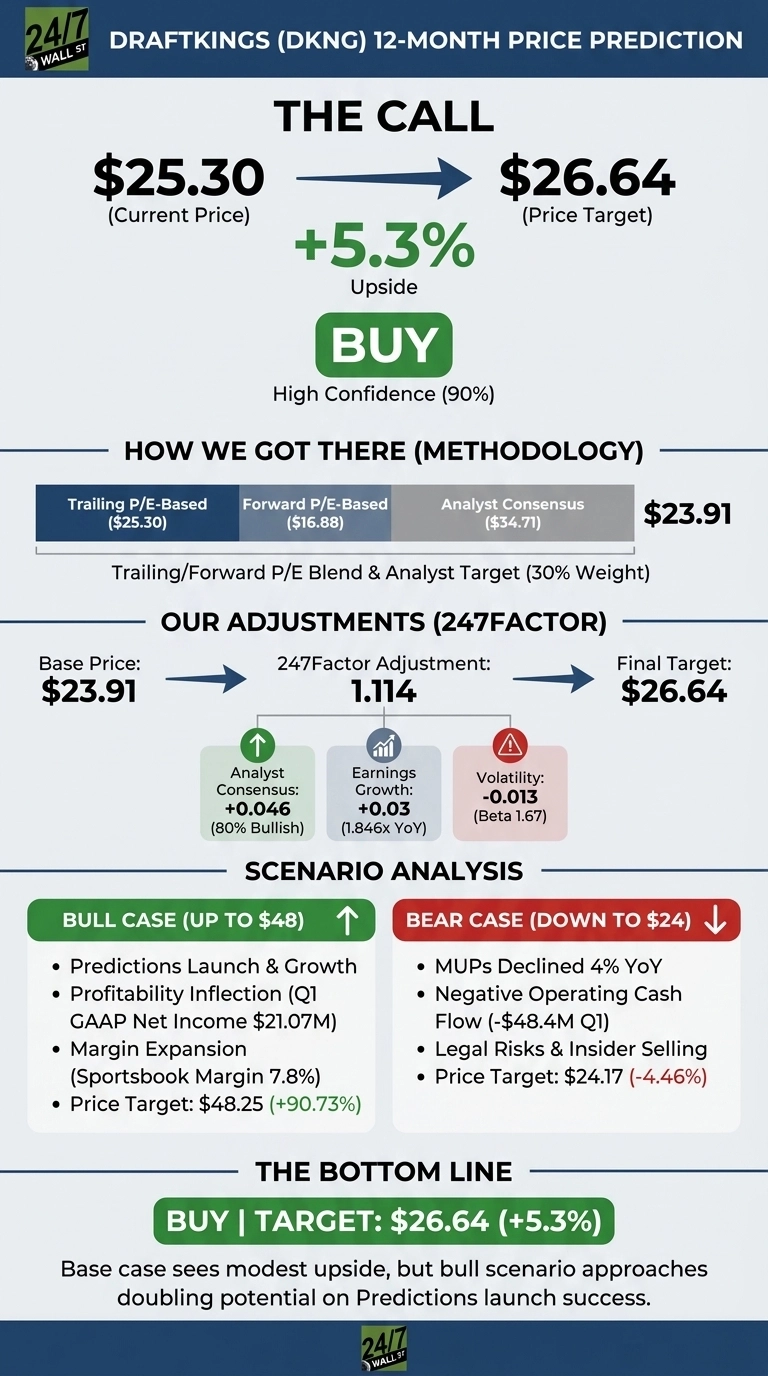

Our 24/7 Wall St. price target for DraftKings is $26.64, implying a modest 5.3% upside from the $25.30 close on June 2, 2026. The recommendation is buy, with a high 90% confidence score driven by strong analyst consensus and accelerating earnings.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $25.30 |

| 24/7 Wall St. Price Target | $26.64 |

| Upside | +5.3% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Brutal Year, a Quiet Recovery

DKNG has been punished. Shares are down 26.58% year to date and 24.99% over the past year, sliding from a 52-week high of $48.78 to a low of $20.46. But the tape is turning: DKNG is up 10% over the past month.

Q1 2026 captures the contradiction. Revenue of $1.65 billion beat by 4.54%, Adjusted EBITDA jumped 64% to $167.85 million, and GAAP net income hit $21.07 million. Yet EPS of $0.20 missed the $0.3591 consensus by 44.31%, reflecting heavy Predictions investment.

Why Bulls See $48 Ahead

The bull thesis is straightforward. Our bull case 1-year scenario projects $48.25, a 90.73% return that nearly doubles the stock. Analyst consensus sits at $34.71, with 23 Buy and 5 Strong Buy ratings.

The Predictions launch is the wildcard. CEO Jason Robins said, “profitability is inflecting. That gives us the firepower to press our advantage in Predictions… We intend to establish a leadership position in Sports Predictions before year-end.”

Morningstar’s Dan Wasiolek called prediction markets “an attractive opportunity on top of the core business”. Add a buyback authorization, Missouri mobile launch, and sportsbook net revenue margin expansion to 7.8%, and the path to a higher valuation becomes credible. UBS analyst Robin Farley raised the price target on DraftKings Inc. to $49 while maintaining a Buy rating.

What Could Go Wrong

The bear case worries me more than the bulls admit. Monthly Unique Payers fell 4% YoY, operating cash flow was negative $48.4 million, and DKNG faces two class action lawsuits alleging addictive product design. Insiders have leaned net seller, including Director Levin Woodrow’s 34,234 share sale at $25.71.

To be fair, the cash flow drag reflects deliberate Predictions investment in a new growth initiative. ARPMUP rose 21% to $131, which means fewer but more valuable users. Still, our bear case scenario lands at $24.17, a 4.46% drawdown.

Weighing the Setup

The 24/7 Wall St. price target is $26.64 with a buy recommendation and 90% confidence. DKNG will not double in 2026 in our base case, but the risk/reward remains asymmetric relative to the bull and bear scenarios above.

The setup looks constructive if Predictions launches on time and MUPs reaccelerate by Q3. The thesis weakens if MUP declines worsen or another addiction lawsuit gains traction.

DraftKings Price Prediction 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $26.64 |

| 2030 | $32.50 |

These projections assume DraftKings continues executing on its current strategy. Significant upside (toward the bull case $111.82 2031 target) could result from a successful Predictions launch and iGaming legalization in major states.