Meta (NASDAQ: META | META Price Prediction) and NVIDIA (NASDAQ: NVDA) both just delivered headline-grabbing quarters, but from opposite sides of the AI capex trade.

Meta is writing the checks. NVIDIA is cashing them. With $10,000 in hand, the question is whether you want the buyer of compute at a discount or the seller of compute near record highs.

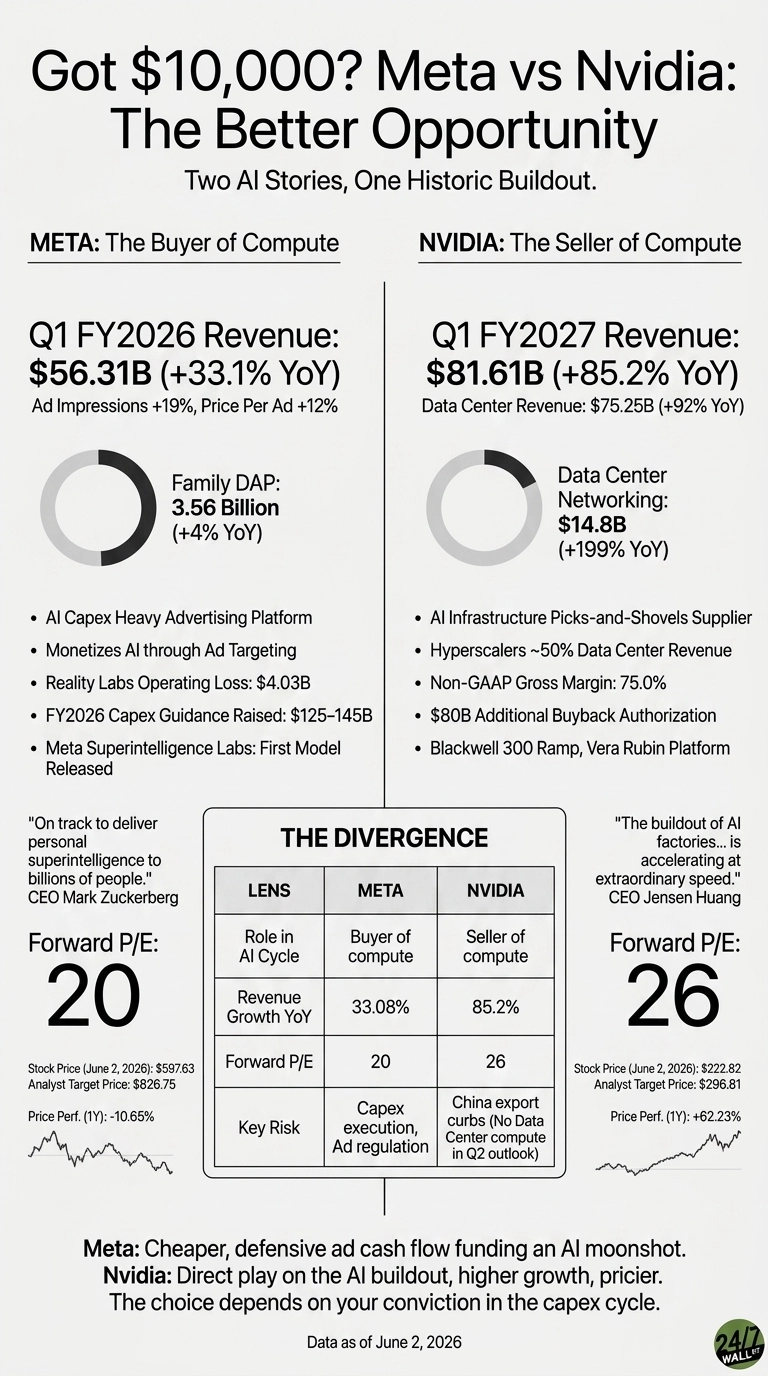

One Quarter, Two Very Different AI Stories

Meta’s Q1 was a flex of the ad machine. Revenue hit $56.31 billion, up 33.08% year over year, with ad impressions +19% and pricing +12%. Family daily active people reached 3.56 billion. Reported EPS of $10.44 looks huge, but $3.13 came from a one-time CAMT tax benefit. Strip that out, and the story is steady ad strength funding an AI buildout that keeps getting more expensive.

NVIDIA’s most recent earnings report was louder. Revenue of $81.61 billion grew 85.2% year over year, with Data Center alone at $75.25 billion and networking up 199% on InfiniBand and Spectrum-X demand.

Jensen Huang called the AI factory buildout “the largest infrastructure expansion in human history”. The Blackwell 300 ramp, Vera Rubin platform, and BlueField-4 give NVIDIA a roadmap deep into 2027.

Where the Strategies Really Diverge

Meta is leaning into capex like a hyperscaler. Full-year 2026 capex guidance jumped to $125 to $145 billion, up from the prior $115 to $135 billion range. Zuckerberg framed it as a march toward “personal superintelligence to billions of people”, but Reality Labs still bled $4.03 billion in operating losses. That is a lot of conviction to ask of advertisers.

NVIDIA, meanwhile, is monetizing every dollar of that buildout. Non-GAAP gross margin hit 75%, with hyperscalers driving roughly 50% of Data Center revenue and sovereign AI customers filling out the rest. Management authorized $80 billion in additional buybacks and raised the dividend to $0.25.

| Lens | Meta | NVIDIA |

| Role in AI Cycle | Buyer of compute | Seller of compute |

| Revenue Growth YoY | 33.08% | 85.2% |

| Forward P/E | 20 | 26 |

| Key Risk | Capex execution and ad regulation | China export curbs |

The Next Test Is Who Justifies the Spend

Meta shares are down 10.68% since the April 29 report and 9.39% year to date, with Reddit chatter shifting bearish on the layoff and AI ROI narrative (latest sentiment score 25).

NVIDIA is up 19.48% YTD and 62.23% over one year, though retail is wrestling with GPU rental price drops and Michael Burry’s skepticism. I will be watching Meta’s Q2 revenue band of $58 to $61 billion and whether NVIDIA’s $91 billion Q2 guide holds without China Data Center compute.

Why I Lean NVIDIA, With Meta as the Patient Pick

On a $10,000 split today, the risk/reward appears to tilt toward NVIDIA. The forward P/E of 26 on triple-digit Data Center growth still looks reasonable to me, and analyst targets averaging $296.81 suggest room above the current $222.82.

Meta is the cheaper, more defensive name at a forward P/E of 20 with an analyst target of $826.75, and it suits investors who want ad cash flow funding the AI moonshot. Skeptics of AI capex returns may find the setup uncertain, while investors who believe the buildout is real often view NVIDIA as the most direct expression of that thesis.

Contact [email protected] for any questions or corrections.