Palantir (NASDAQ:PLTR | PLTR Price Prediction) and Oracle (NYSE:ORCL) both just put out earnings that read like AI manifestos, but the businesses underneath could not be more different.

Palantir closed Q4 2025 as a capital-light software shop riding U.S. commercial adoption. Oracle finished Q3 FY2026 as a balance-sheet-heavy hyperscaler pouring tens of billions into GPUs and concrete.

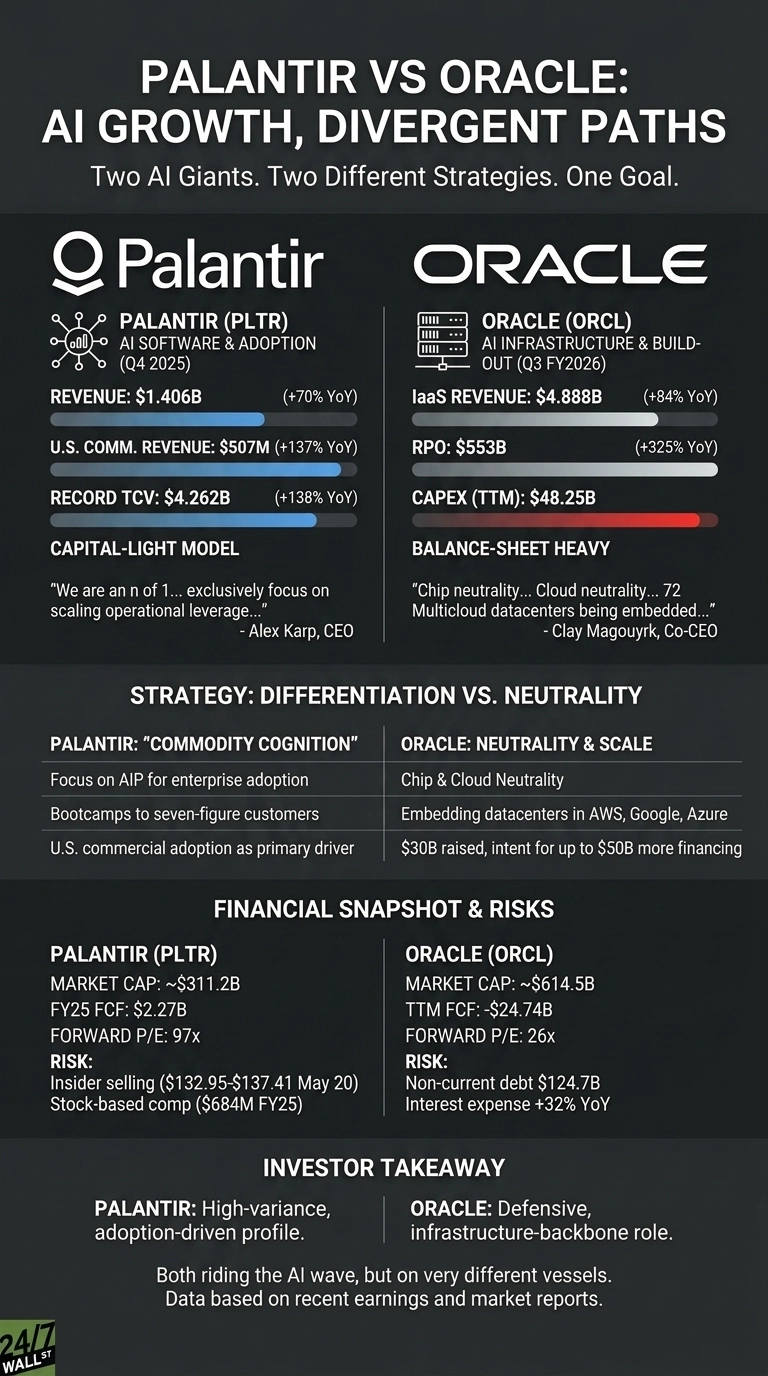

AIP Floods One Side. GPU Buildouts Define the Other.

Palantir put up $1.406 billion in revenue, growing 70% year over year, with U.S. commercial revenue exploding 137% to $507 million. That is AIP doing the work, pulling enterprises into bootcamps and turning them into seven-figure customers. Closed total contract value hit a record $4.262 billion, up 138%, which is what a real demand wave looks like.

Oracle’s quarter was a different animal. Cloud infrastructure revenue surged 84% to $4.888 billion, and remaining performance obligations rocketed 325% to $553 billion as customers prepaid or supplied their own GPUs. SaaS grew just 13% and core software a sleepy 3%, so the AI story is doing nearly all the heavy lifting.

| Driver | Palantir | Oracle |

| Top growth engine | U.S. commercial AIP | OCI (IaaS) |

| Capital model | Software, asset-light | Debt-funded datacenters |

| FCF posture | $2.27B FY25 FCF | -$24.7B trailing FCF |

Differentiation vs. Neutrality

Alex Karp framed it bluntly: “We are an n of 1, and these numbers prove it. Palantir is alone in choosing to exclusively focus on scaling the operational leverage made possible by the rapid advancements of AI models.” That is a bet on being uniquely indispensable inside the customer’s workflow.

Oracle is going the other way. Co-CEO Clay Magouyrk has pushed chip neutrality and cloud neutrality, with 72 Multicloud datacenters being embedded inside AWS, Google, and Azure.

Larry Ellison’s team raised $30 billion in bonds and convertible preferred and flagged intent for up to $50 billion more in financing. Non-current debt already swelled to $124.7 billion. That is conviction, or a very expensive bet, depending on the day.

The Next Test Is Cash Generation

For Palantir, I will be watching whether U.S. commercial can really clear the $3.144 billion bar implied in 2026 guidance, and whether stock-based comp ($684 million in FY25) stops diluting that pristine FCF story. Insider selling at $132.95 to $137.41 on May 20 is a small caution flag.

For Oracle, the question is whether $50 billion of FY26 capex converts into usable AI revenue fast enough to service that debt. Polymarket traders give an 84% probability Oracle hits the $50 billion capex target, but only 48% for $52.5 billion. The crowd believes in the plan while stopping short of pricing in a blowout.

How the Two Stack Up for Investors

Investors seeking defensive AI exposure with a dividend and a sizable revenue backlog will find Oracle’s profile more conservative. The 26x forward P/E and 26.1% one-year gain reflect a story already partly priced in, but RPO gives visibility most peers cannot match.

Palantir, trading at a 97x forward P/E after a 23.75% year-to-date drawdown, represents the higher-variance profile tied to enterprise AI adoption. One framing puts Oracle in an infrastructure-backbone role and Palantir in a smaller, more volatile sleeve. Should Oracle’s interest expense keep climbing past the 32% YoY pace, that balance would warrant reassessment.

Contact [email protected] for any questions or corrections.