Home Depot (NYSE:HD | HD Price Prediction) is the largest home improvement retailer in America, and right now it’s stuck in a frustrating holding pattern.

CEO Ted Decker told investors after Q1 that “the underlying demand in our business was relatively similar to what we saw throughout fiscal 2025, despite greater consumer uncertainty and housing affordability pressure.” Translation: the business is fine, the macro is not. Shares are down 3.89% YTD while consumer spending grinds higher. So can HD really hit $450 by 2028? Let’s run the math.

What’s Holding Home Depot Back Right Now

The issue is the housing cycle. Existing home turnover remains depressed, big-ticket remodel demand has been soft, and customer transactions fell 1.3% in Q1 FY2026. GAAP operating margin compressed to 11.9% from 12.9% as SRS Distribution amortization weighed on profitability.

Shares have fallen 7.13% over the past year and sit 11% below the 52-week high of $418.06. With a beta of 0.974, this is a slow grind that has tested patience. The recent 5.18% one-week bounce hints sentiment may be turning, but the housing overhang is real.

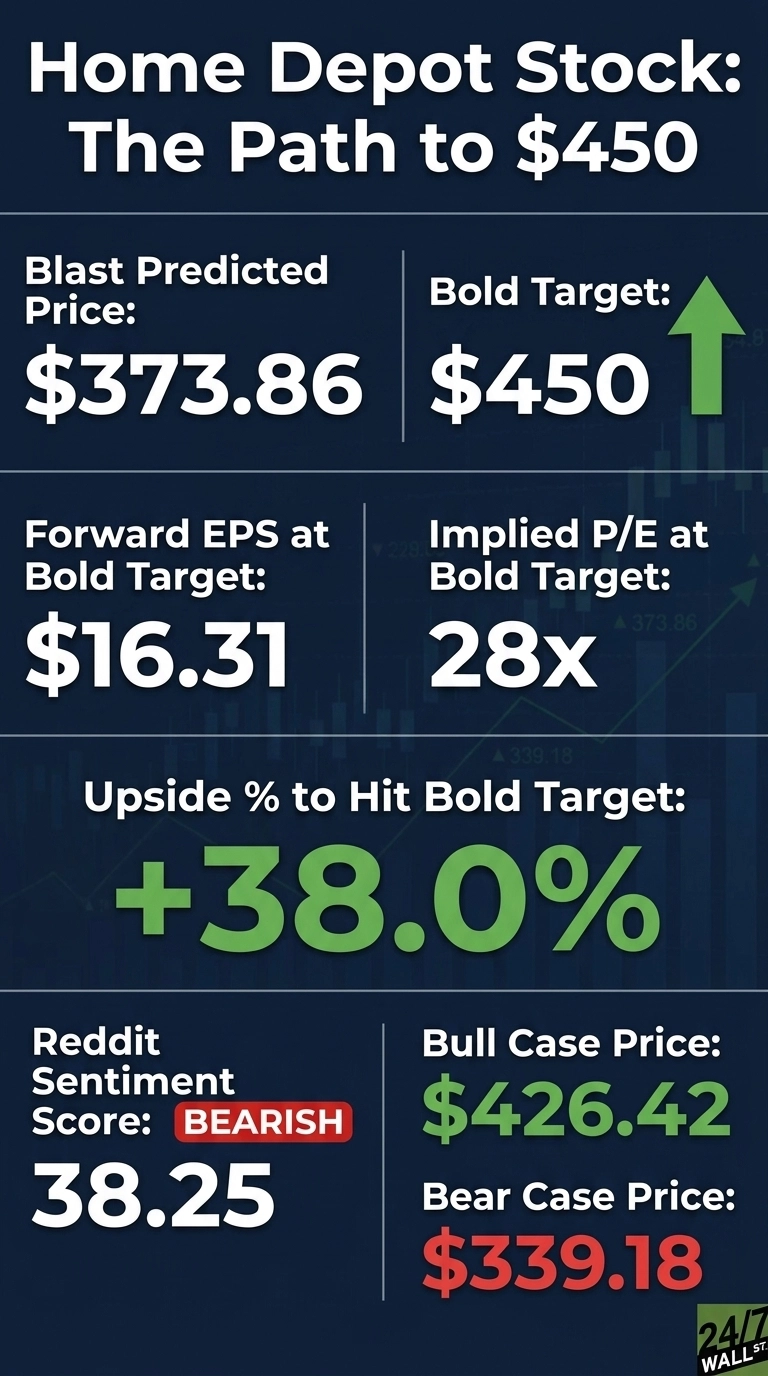

Wall Street Sees Modest Upside. Our Model Sees More

Wall Street’s consensus price target sits at $370.18, with 4 Strong Buy, 18 Buy, and 14 Hold ratings, no Sell calls. That is a polite shrug. Our base case lands at $373.86 for a 14.68% two-year return, with a bull case of $426.42 and a bear case of $339.18. Our confidence sits at 90%, which is high.

I think analysts are anchoring too hard on FY26 guidance and underweighting what happens when housing turnover normalizes. With 61% of analysts bullish and insiders net buying across 54 recent transactions, the conviction is quietly building.

The Path to $450 Per Share

Here is the math. Reaching $450 from today’s price of $326.01 would require a gain of 38%. With forward EPS of $16.31, a price of $450 implies a forward P/E of 28x. Our base case of $373.86 already implies 22x, meaning the bold target requires roughly 5x of additional multiple expansion.

Is that achievable? I think yes, under the right conditions. Our 247Factor adjustment came in at 1.061, driven by moderate analyst optimism (+0.037 contribution) and a mega-cap dampening that limits upside math. But the bigger story is the macro.

BEA data shows furnishings spending climbed to $527.5B in April 2026 from $516.7B in January, and housing services spending reached $3,930.7B. If mortgage rates ease and remodel demand reawakens, FY27 and FY28 EPS could push well past $17.

Layer in SRS and GMS contributions scaling, and a 27x multiple on rising earnings becomes defensible. The primary risk: a prolonged housing recession that keeps comps flat into 2028.

Where Home Depot Trades Today vs Its Earnings Power

At $326.01, HD trades at a forward P/E of 20x, which strikes me as cheap for a business with 128.4% ROE and 156 consecutive dividend payments.

Shares sit between a 52-week low of $286.95 and high of $418.06. Over the past decade, HD has returned 224.88%, a reminder that patience here usually pays. The current valuation reflects cycle pessimism, not structural decline.

Is $450 Realistic? Here’s My Take

Reaching $450 by 2028 requires a 38% gain from here. I think it is a stretch but not a long shot.

Three things need to go right: housing turnover normalizes by late 2027, SRS and GMS integration drives operating margin back above 13%, and the Fed cuts enough to revive big-ticket projects.

What derails it? A second leg lower in housing that keeps comps negative into FY27. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how Home Depot could reach $450 in 2028.