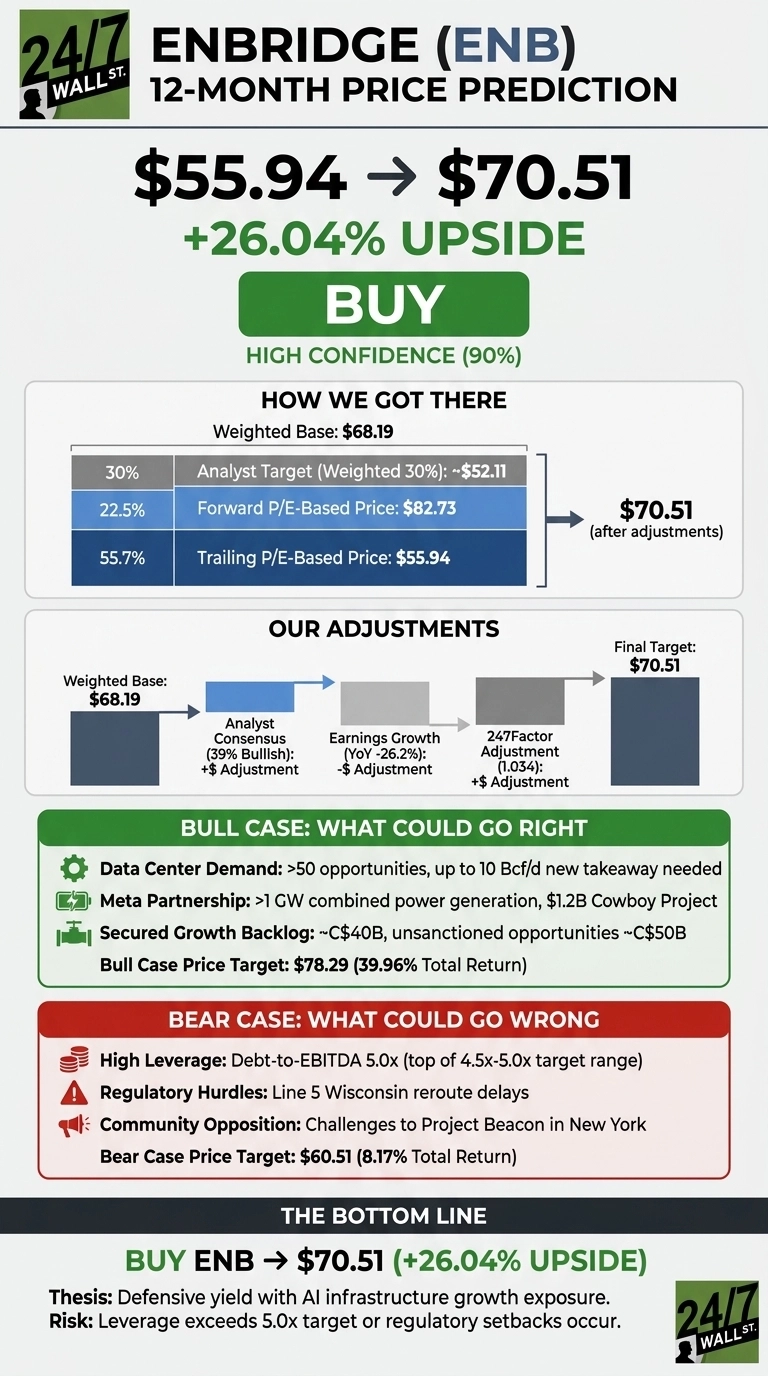

Enbridge (NYSE:ENB | ENB Price Prediction) is trading within striking distance of its 52-week high, and the question for investors is whether the rally has more room to run. Shares closed at $55.94 on June 15, 2026, just 11% below the 52-week high of $58.45.

Our 24/7 Wall St. price target for Enbridge is $70.51, implying 26.04% upside over the next 12 months. Our model rates ENB a buy with high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $55.94 |

| 24/7 Wall St. Price Target | $70.51 |

| Upside | 26.04% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Quiet Rally Built on Record Cash Flow

ENB has gained 20.09% year to date and 26.61% over the past year, outpacing typical midstream peers.

The Q1 2026 report, released May 8, 2026, delivered adjusted EPS of $0.98, adjusted EBITDA of $5.81 billion, and distributable cash flow of $3.85 billion. Mainline volumes ran at 3.2 million barrels per day and have been apportioned all year. Recent news flow reinforces the thesis: RBC Capital raised its target to C$79 and Scotiabank moved to C$78, both Outperform.

The Case for $78+

Bulls have an easy story to tell. Enbridge is advancing over 50 data center opportunities needing up to 10 Bcf/d of new gas takeaway. The Meta partnership now spans over 1 GW of combined power, with the $1.2 billion Cowboy Project in Wyoming adding 365 MW of solar and 200 MW of battery storage.

The secured backlog stands at C$40 billion with unsanctioned opportunities of C$50 billion. Our bull case scenario points to $78.29, a 39.96% total return. With 31 consecutive years of dividend hikes and a 6.9% yield, income investors get paid to wait.

What Could Go Wrong

Leverage is the biggest watch item. Debt-to-EBITDA sits at 5.0x, the top of the 4.5x-5.0x target range. CAD/USD translation, regulatory delays on projects like the Line 5 Wisconsin reroute, and community opposition to Project Beacon in New York add execution risk.

TD Bank maintains a Hold, and a Seeking Alpha analyst flagged concerns about acquisition-driven earnings quality. The bear scenario lands at $60.51, still 8.17% above current levels. The GAAP earnings decline largely reflects non-cash derivative losses, while distributable cash flow rose to $3.85 billion.

Enbridge Price Prediction 2026-2030

Our 24/7 Wall St. price target of $70.51 implies meaningful upside, and our model carries a buy rating with 90% confidence. The tipping factor is the take-or-pay commercial framework feeding a 20-year guidance track record.

The setup favors investors seeking defensive yield with AI infrastructure exposure. The thesis weakens if leverage climbs meaningfully above 5.0x or if the Mainline tolling settlement compresses margins more than expected.

Looking further ahead, here is where our model projects ENB could trade, assuming 5% post-2026 CAGR on EBITDA, EPS, and DCF per share holds.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $70.51 |

| 2027 | $78 |

| 2028 | $87 |

| 2029 | $97 |

| 2030 | $110 |

These projections assume Enbridge continues converting backlog into in-service assets on schedule. Significant upside could come from accelerated data center buildout, while regulatory setbacks or a sustained equity issuance program would pressure the trajectory.

Contact [email protected] for any questions or corrections.