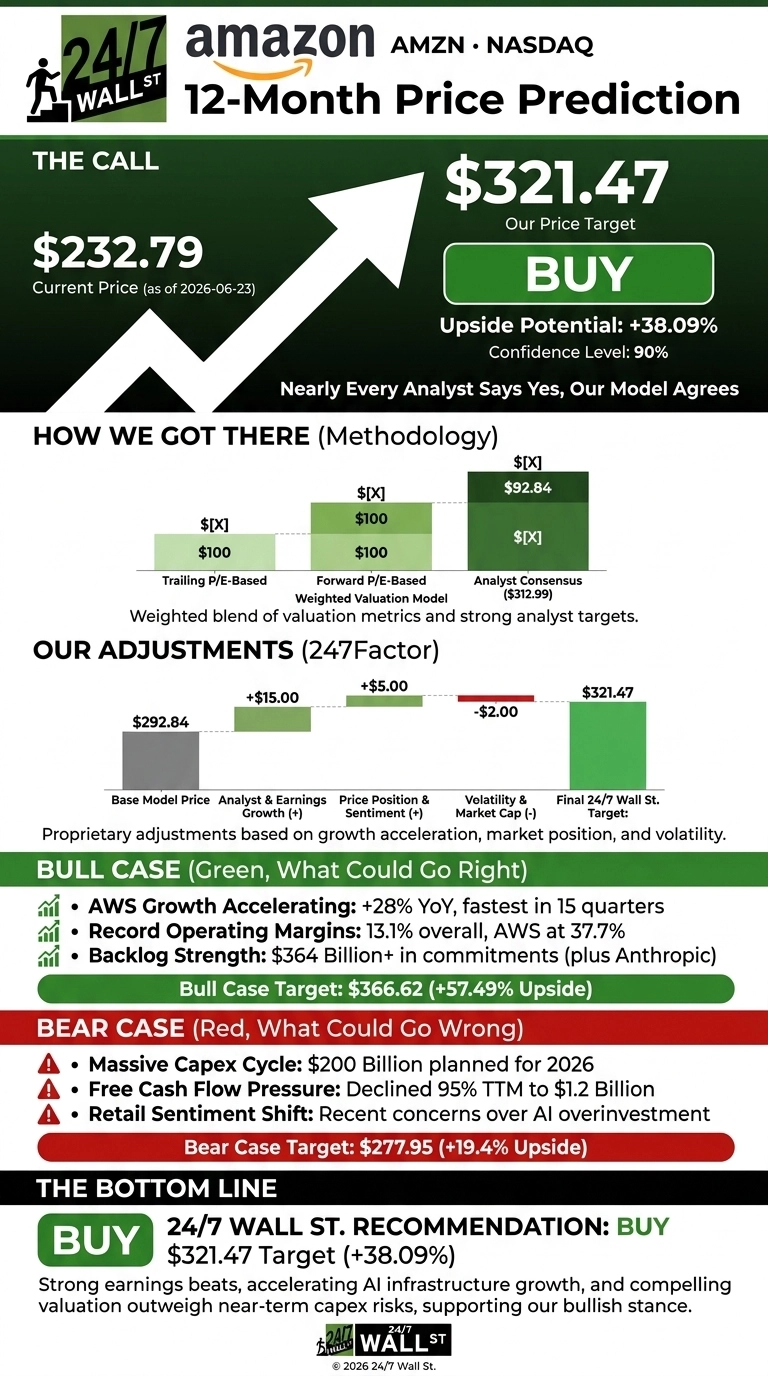

Amazon (NASDAQ:AMZN | AMZN Price Prediction) just delivered its fastest AWS growth in 15 quarters, yet shares have pulled back from recent highs. With analyst consensus overwhelmingly bullish, our proprietary model offers a clear read on whether this dip is a gift or a warning.

The 24/7 Wall St. Price Target for Amazon

Our 24/7 Wall St. price target for Amazon is $321.47 over the next 12 months, implying 38.09% upside from the recent close of $232.79. The model carries a 90% confidence score, and the recommendation reads buy.

| Metric | Value |

|---|---|

| Current Price | $232.79 |

| 24/7 Wall St. Price Target | $321.47 |

| Upside | 38.09% |

| Recommendation | BUY |

| Confidence Level | 90% |

Amazon trades roughly 12% below its 52-week high of $278.56 after a Q1 2026 earnings report that beat EPS estimates by 68.18%. Accelerating AWS growth, expanding operating margins, and a reset stock price give the model an unusually clean entry.

An Earnings Blowout the Market Hasn’t Rewarded

AMZN has slipped 5.38% over the past week and 12.59% over the past month, leaving shares up 0.85% year to date and 11.02% over twelve months.

The Q1 2026 release on April 29 showed strong results: revenue of $181.519 billion (16.61% YoY growth), EPS of $2.78 versus $1.653 expected, and operating income up 29.6% to $23.852 billion.

AWS grew 28% to $37.587 billion, and the chips business surpassed a $20 billion run rate. The stock drifted lower partly on retail concerns that the $200 billion 2026 capex plan will weigh on free cash flow, which fell 95% TTM to $1.2 billion.

The Case for $366 and Higher

The bull scenario builds on an AWS backlog of $364 billion, which does not yet include the recent Anthropic deal of over $100 billion. CEO Andy Jassy noted “we now have over $225 billion in revenue commitments for Trainium”, with OpenAI committing 2 GW of Trainium capacity starting 2027 and Anthropic up to 5 GW.

Operating margin hit 13.1% in Q1, the highest ever, and advertising crossed $70 billion in TTM revenue. Our bull case projects $366.62 within 12 months, a 57.49% return. Bullish analyst ratings cluster heavily: 47 Buys, 15 Strong Buys, and zero Sells. JP Morgan has an Overweight rating with a price target of $330.

The Risks Worth Watching

The bear case starts with capex. The $200 billion 2026 capex plan and a 95% TTM drop in free cash flow to $1.2 billion are precisely what retail communities flag as “multiyear downturn” risk. AWS operating margin compressed slightly to 37.7% versus 39.5% YoY, and net income was boosted by a $16.8 billion non-recurring Anthropic gain.

Bulls counter that this mirrors the original AWS buildout cycle, where heavy investment created the most valuable cloud franchise in tech. Our bear case still lands at $277.95, 19.4% above today’s price.

Amazon Price Prediction 2026-2030

The 24/7 Wall St. price target of $321.47 with 90% confidence points firmly toward buy. The setup looks attractive if you believe AWS can sustain 25%+ growth into 2027 as Trainium and Bedrock commitments convert to revenue.

The case weakens if you expect the $200B capex cycle to compress ROIC for multiple years without proportional revenue. The Q1 earnings report, the $364 billion backlog, and record margin all point in the same direction.

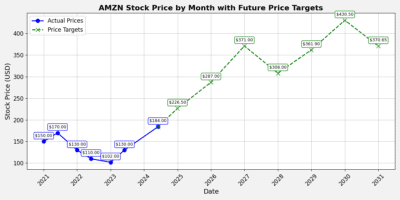

Looking ahead, here is where our model projects Amazon could trade in the coming years, assuming current growth trajectories and a roughly 19.83% annualized base case path hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $255 |

| 2027 | $305 |

| 2028 | $366 |

| 2029 | $438 |

| 2030 | $525 |

These projections assume Amazon converts its AWS backlog into revenue and sustains advertising momentum above 20% growth. Material upside or downside could come from faster AI monetization or a deeper capex digestion cycle.

Contact [email protected] for any questions or corrections.