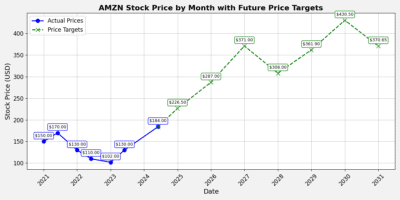

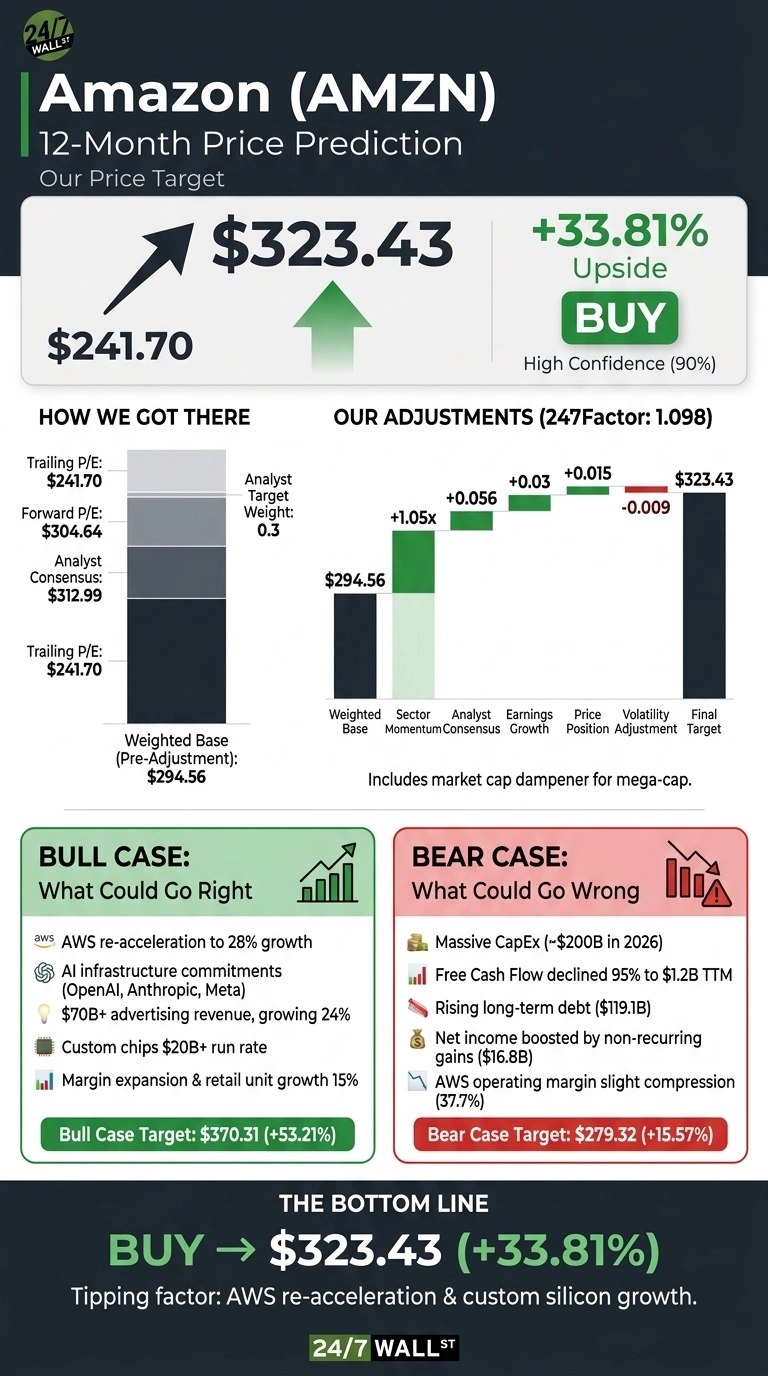

My Amazon (NASDAQ:AMZN | AMZN Price Prediction) call is straightforward. The 24/7 Wall St. price target for Amazon is $323.43 by July 2, 2027, and my base-case path has the stock crossing $300 for the first time around April 2, 2027 at a modeled $301.86. From a current price of $241.70, that is roughly 33.81% of upside. My recommendation is buy, at high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $241.70 |

| 24/7 Wall St. Price Target | $323.43 |

| $300 Crossed On | April 2, 2027 |

| Upside | 33.81% |

| Recommendation | BUY |

| Confidence Level | 90% |

How Amazon Got Back to $241 After a Rough Spring

Amazon is up 3.17% over the past week and 9.63% over the past year, but trading has been choppy. Shares fell 7.49% in the last month and sit about 12% below the 52-week high of $278.56, with a low of $196.

The setup got better fast in Q1 2026: EPS of $2.78 topped the $1.73 consensus, a 60.69% surprise on revenue of $181.52 billion, up 16.61% YoY. AWS grew 28%, the fastest in 15 quarters, and Prime Day just kicked off with online spending rising 5.3% on day one to $8.3 billion.

The Bull Case for $370

The bull scenario takes Amazon to $370.31, or 53.21% upside. Three engines drive it. AWS is compounding at 28% on a 37.7% operating margin, with landmark AI compute commitments from OpenAI (2 GW of Trainium), Anthropic (up to 5 GW), and Meta Platforms (NASDAQ:META).

The custom-chips business already runs at a $20 billion annual run rate with triple-digit YoY growth. Advertising is a $70 billion+ TTM franchise growing 24% at software-like margins.

North America retail margins expanded to 7.9% from 6.3%, and unit growth hit 15%, the highest since COVID. Analyst consensus already sits at $312.99 with 62 buy ratings and zero sells.

The Risks Worth Watching

The bear path stops at $279.32, still 15.57% upside, but the risks are real. Planned 2026 CapEx of roughly $200 billion pushed free cash flow down sharply, and long-term debt has climbed to $119.1 billion from $65.6 billion. AWS operating margin slipped to 37.7% from 39.5%, and Q1’s headline net income of $30.25 billion was boosted by $16.8 billion in non-recurring Anthropic gains.

Reddit sentiment turned bearish in late June around “overinvestment in data centres” concerns. It should be noted, however, that bulls counter that adjusted operating income still grew 30% YoY excluding investment gains, and management is guiding to strong long-term return on invested capital from the CapEx surge.

Amazon Price Prediction 2026-2030

My 24/7 Wall St. price target for Amazon is $323.43, a buy with 90% confidence. The tipping factor is AWS re-acceleration paired with a custom-silicon business that already prints $20 billion.

I’d be a buyer here if Q2 revenue lands inside the guided $194 billion to $199 billion range and AWS holds mid-20s growth. I’d stay on the sidelines if AWS decelerates below 22% or CapEx overshoots $210 billion without matching revenue.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $270 |

| 2027 | $323 |

| 2028 | $385 |

| 2029 | $460 |

| 2030 | $552 |

These projections assume Amazon continues executing on AWS, ads, and custom silicon at a 17.95% annualized base-case return through 2031. Significant upside could come from Trainium winning share from NVIDIA (NASDAQ:NVDA), while downside would likely come from a CapEx-driven return-on-capital reset.

Contact [email protected] for any questions or corrections.