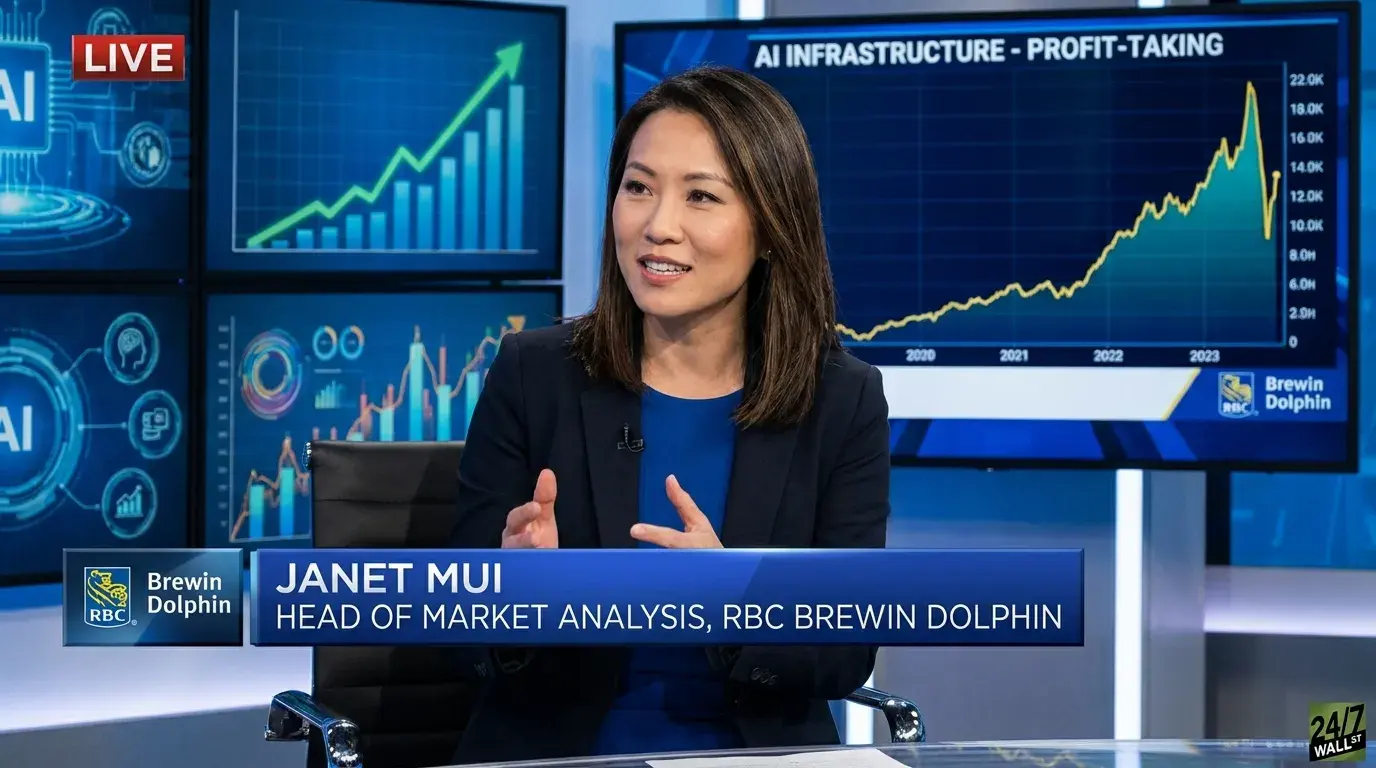

Janet Mui, Head of Market Analysis at RBC Brewin Dolphin, used a CNBC appearance on Tuesday, June 23, to push back against the idea that the recent pullback in AI and semiconductor stocks signals that something is broken in the sector. She believes the move looks like classic profit-taking after a vertical run, with the structural AI infrastructure story still firmly in place.

The market context supports the idea that this is an orderly pullback rather than a panic. The CBOE Volatility Index sat at 17.28 on June 22, 2026, inside its 15-to-20 “normal range” and well off the 31.05 peak hit on March 27, 2026. Even after a sharp single-day reset in chips, the fear gauge has stayed contained.

Why Mui Sees the Selloff as Profit-Taking

Mui anchored her analysis to the speed of the prior advance, particularly in Asia. “The retreat is somewhat expected given the blistering run, particularly in Korea, South Korean markets, because there has been a lot of retail participation, which is mainly driven by retail actually. And there has been a lot of leverage being used,” she said, framing the Korean drawdown as a natural unwind of crowded retail positioning.

On the chipmakers and memory names that led the selloff, she argued these businesses are still strong. “I don’t think that the fundamentals of the chipmakers or the memory players have changed. And also, I believe that this is more like a profit-taking and reversal of the very hot and overbought conditions,” Mui said.

The setup she is describing is visible across the major chip benchmarks. The VanEck Semiconductor ETF (NYSEARCA:SMH) is up 85.74% year to date and 157.8% over the past year through June 22, while the iShares Semiconductor ETF (NASDAQ:SOXX) is up 117.73% year to date and 192.32% over the trailing year. Both ETFs gave back a chunk in a single session, with SMH down 6.81% and SOXX down 7.71% on June 23. By contrast, the broader Invesco QQQ Trust (NASDAQ:QQQ) has held up better, up 20.13% year to date, suggesting concentrated unwind rather than market-wide stress.

The AI Infrastructure Boom Has Years of Runway

Mui pointed to industry messaging that points to supply constraints lasting for years. “The growth area we have now is obviously AI, particularly the buildup of the AI infrastructure is going to the hardware, semiconductors and memory providers. And we all heard from industry leaders that… there’s plenty of evidence that the bottleneck is there and would be until at least 2028 or beyond,” she said, presenting that timeline as the industry consensus she leans on.

Her bigger-picture argument is that this is going to be a generational capex cycle. “The core story is unchanged. The fundamentals are unchanged, as in the hyperscalers or businesses around the world have to spend billions of dollars to build out their AI infrastructure, which is completely new. And there will be… factories that produce output, just like human labor.”

Morgan Stanley recently raised its 2026 server market total addressable market to $809 billion, citing AI infrastructure needs, and Blackstone announced plans to invest $30 billion in AI data centers in Japan over three to five years, with COO Jonathan Gray saying, “[The] risk of underbuilding computing resources for AI is greater than concerns about a potential bubble.” Wedbush, on the same SK Hynix-driven memory wobble, viewed the dip as a buying opportunity, asserting that enterprise demand for AI remains strong.

Key Takeaways

Mui’s thesis is pretty much that when a market rises too fast, it eventually needs a reset. In her view, that reset is underway, but the forces that powered the rally remain strong. Chipmakers, memory providers, and AI infrastructure companies still sit at the center of a multi-year spending cycle that requires hyperscalers and enterprises to invest billions of dollars in building new computing capacity.

Contact [email protected] for any questions or corrections.