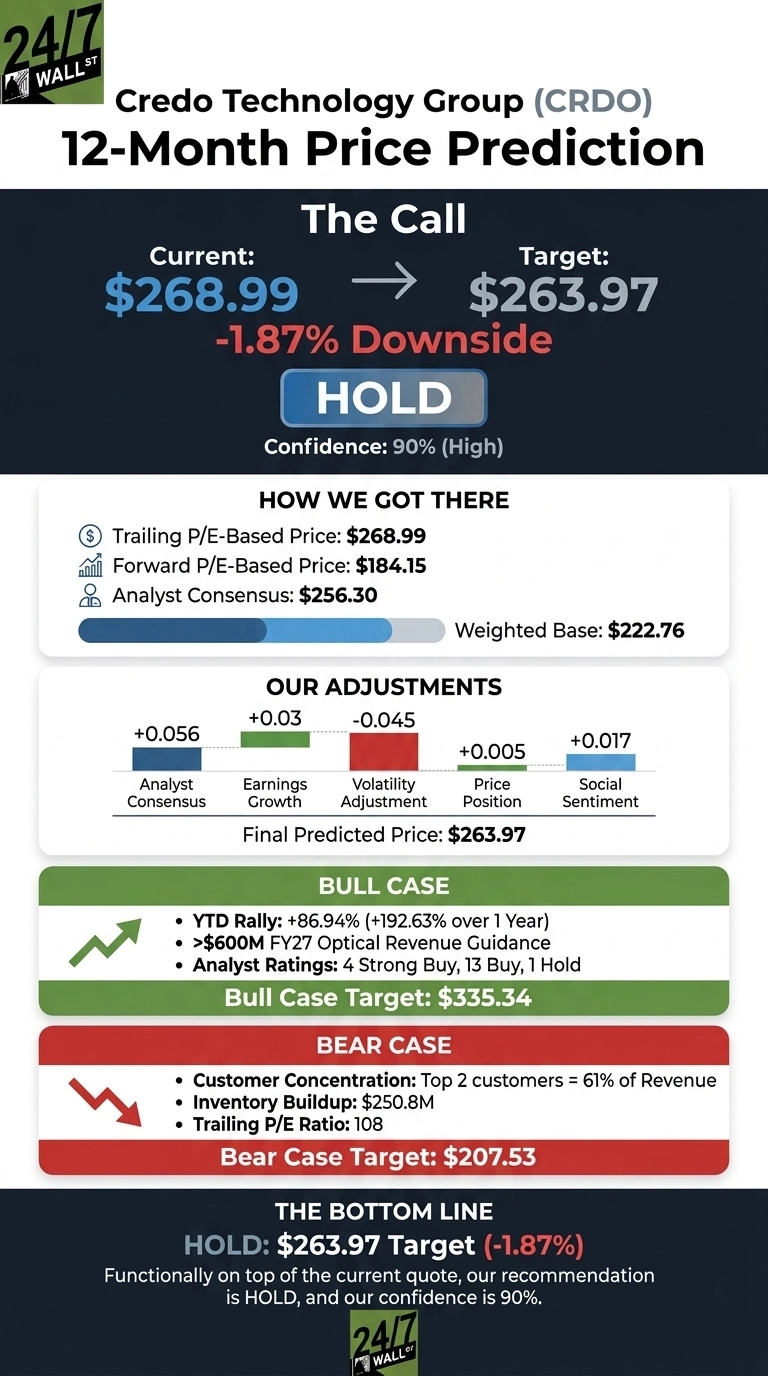

I am opening with our verdict on Credo Technology Group (NASDAQ:CRDO | CRDO Price Prediction). The stock has rallied 86.94% year to date, and our proprietary model now sees the shares trading almost exactly where they should.

The 24/7 Wall St. price target for Credo is $263.97, which sits a hair below the last close of $268.99. That implies 1.87% downside, a hold rating, and a 90% (high) confidence reading.

| Metric | Value |

|---|---|

| Current Price | $268.99 |

| 24/7 Wall St. Price Target | $263.97 |

| Upside/Downside | -1.87% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target sits a touch below where Credo trades today, and that gap is small enough to flip. The bull catalysts are real: the just-closed Dust Photonics acquisition opens a silicon photonics path to 3.2 Tbps, and management is guiding to more than $600 million in optical revenue for fiscal 2027. Treat our target as one datapoint. A full bull case sits below.

From $79 to $269 in a Year

Credo has been one of the AI infrastructure trade’s cleanest winners. The stock is up 192.63% over the past year, 23.16% over the past month, and 7.89% in the past week alone. Shares now trade 17% below the 52-week high of $308.67 and well above the $84.25 low.

The fuel is fundamental. Q4 FY26 revenue hit $437 million, up 157.02% year over year, with non-GAAP EPS of $1.16 beating the $1.0341 estimate by 12.17%. Full-year FY26 revenue tripled to $1.34 billion, and non-GAAP net income grew more than 5x to $662 million.

The Case for $335 and Higher

Our bull-case path lands at $335.34 over the next 12 months, a 24.67% gain. The setup is credible. CEO Bill Brennan guided FY27 revenue growth to more than 80% year over year, with Optical DSPs, SiPho PICs, and ZeroFlap optics each contributing more than $100 million.

He also flagged Neo Cloud customers eventually reaching roughly 20% of total revenue. The Street’s bullish camp is thick: 4 Strong Buy, 13 Buy, 1 Hold, 0 Sell ratings.

The Risks Worth Watching

The bear path takes Credo to $207.53, or 22.85% downside. Customer concentration is the headline risk: in Q4, the top customer was 34% of revenue and the second largest was 27%. Inventories also jumped to $250.8 million, and the trailing P/E sits at 108.

In fairness, bulls would counter that the inventory build supports the FY27 optical ramp Brennan described, and the forward P/E is a more digestible 51. Composite sentiment has also slipped 10.03 points over 30 days.

Credo Price Prediction 2026-2030

The 24/7 Wall St. price target of $263.97 is functionally on top of the current quote, our recommendation is hold, and our confidence is 90%. The decisive factor is valuation symmetry: trailing multiples have caught up to FY26’s spectacular growth.

The bullish trigger to watch is whether the FY27 optical ramp tracks ahead of the $600 million bar and Neo Cloud customers diversify the top-line. The bearish trigger is whether the top-two customers slow orders or gross margin slips below the 67% to 69% guide.

Looking further out, here is where our model projects Credo could trade, assuming the optical inflection plays out and AI capex stays elevated.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $263.97 |

| 2030 | $294.24 |

These projections assume Credo continues converting design wins into revenue. Significant upside could emerge from CPO and NPO traction in FY28, while a hyperscaler capex pause is the largest downside risk.

Contact [email protected] for any questions or corrections.