NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) has spent the last two months digesting a strong Q1 earnings report, with the back half of fiscal 2027 looking constructive. Bank of America has flagged Nvidia’s networking silicon as the next multi-billion-dollar business inside the data center, and our model agrees the market is not fully pricing it in.

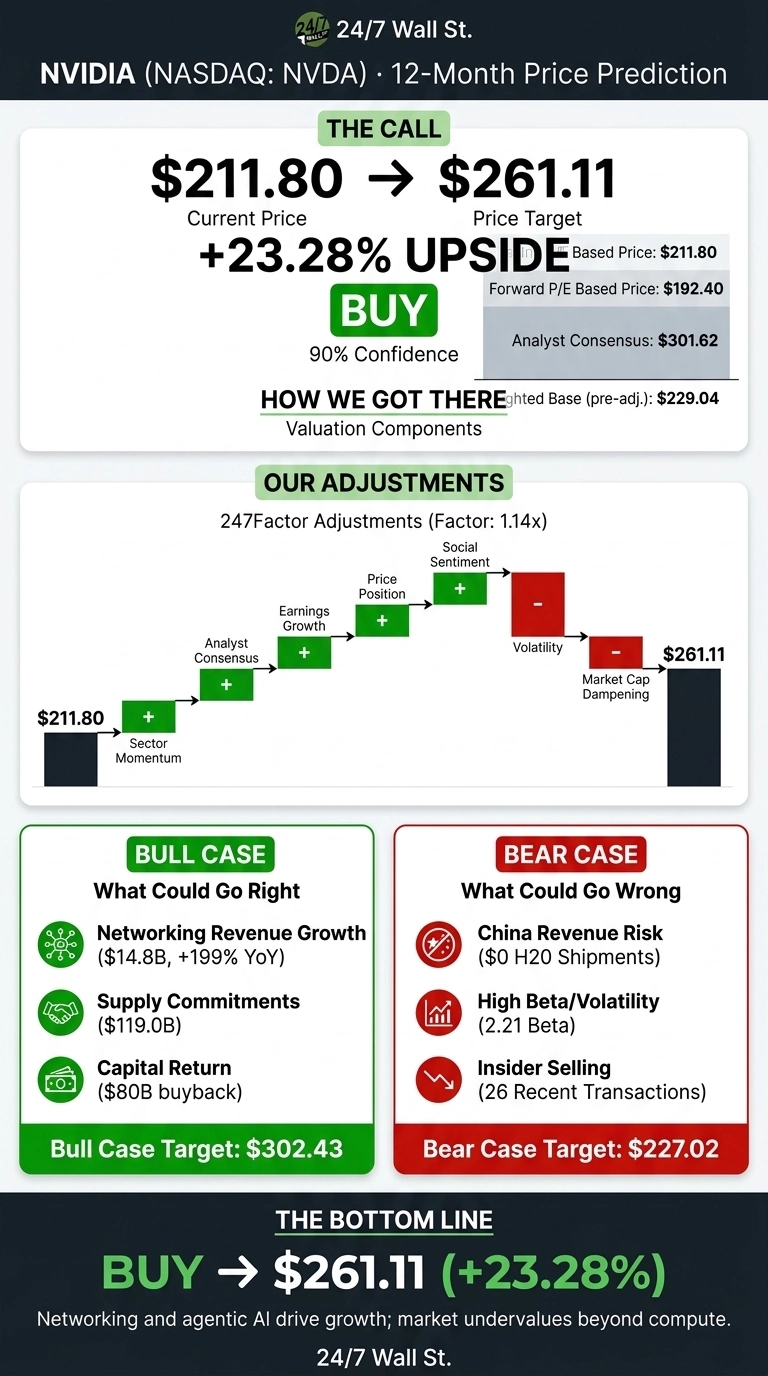

Our 24/7 Wall St. price target for NVDA is $261.11, implying 23.28% upside from $211.80. Our recommendation is buy, with high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $211.80 |

| 24/7 Wall St. Price Target | $261.11 |

| Upside | 23.28% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Summer Reset That Reopened the Runway

NVDA is up 7.55% in the past week and 13.7% year to date, though shares sit roughly 28% below the $236.26 52-week high.

Q1 FY2027, reported on May 20, 2026, delivered: revenue of $81.615 billion grew 85.23% year over year, non-GAAP EPS came in at $1.87 versus $1.7738 consensus, and management guided Q2 to $91.0 billion. Data center networking alone was $14.8 billion, up 199% year over year. That is the line item Bank of America keeps circling.

Why Bulls See $300 and Beyond

The bull case rests on three levers. First, networking scaled from roughly $7.25 billion in Q2 FY26 to $14.8 billion last quarter; Bank of America’s $20B business framing is not aggressive at that trajectory.

Second, supply commitments hit $119 billion, up from $50.3 billion two quarters ago, effectively pre-signing demand.

Third, capital return: an $80 billion buyback authorization landed in May on top of the $38.5 billion remaining.

Jensen Huang stated: “The buildout of AI factories, the largest infrastructure expansion in human history, is accelerating at extraordinary speed.” The Street’s $301.62 average target, backed by 48 Buy ratings, sits within reach if Blackwell 300 and Vera Rubin ramp cleanly (a scenario The Next Nvidia Playbook has been mapping).

What Could Go Wrong

Q2 guidance explicitly excludes China data center compute, and forward revenue was zero from H20 shipments this quarter versus $4.6 billion a year earlier. A prolonged export freeze caps the top line. Beta of 2.211 means any hyperscaler capex pause hits NVDA harder than most.

Insiders have been net sellers across 26 recent transactions. The counterfactual: the $4.5B H20 charge that crushed year-ago margins is gone, gross margin expanded to 75%, and free cash flow of $48.55 billion in a single quarter absorbs macro noise. A bear case scenario lands near $227.02, still above current levels.

How NVIDIA Compares to AMD and Broadcom

Advanced Micro Devices (NASDAQ:AMD) is the direct GPU competitor. AMD’s Q1 FY26 data center revenue of $5.78 billion grew 57% year over year, but NVDA’s data center segment is more than $75 billion in a single quarter. AMD trades at a trailing P/E near 206, making NVDA’s 32 multiple look pedestrian.

Broadcom (NASDAQ:AVGO) is the custom accelerator and AI networking counterpoint. AVGO printed $10.8 billion in AI semiconductor revenue last quarter, up 143%, and guided Q3 AI to $16.0 billion. It validates the size of the networking pie rather than shrinking NVDA’s slice.

| Company | Forward P/E | Latest Qtr Rev Growth |

|---|---|---|

| NVIDIA | 24 | 85.2% |

| AMD | ~35 | 37.9% |

| Broadcom | ~40 | 47.9% |

The peer set makes our $261.11 target look conservative.

Our Take on NVIDIA at Current Levels

Our 24/7 Wall St. price target of $261.11 is a buy at 90% confidence. Networking is real, compounding at triple digits, and the market is still valuing NVDA on compute alone.

The setup looks constructive if hyperscaler capex guides stay firm through the next TSMC report. The thesis weakens if China export policy tightens further and Q2 revenue prints below the $91 billion guide. Neither looks likely right now.

Here is where NVDA could trade if execution holds.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $235 |

| 2027 | $266 |

| 2028 | $301 |

| 2029 | $341 |

| 2030 | $386 |

These projections assume NVIDIA sustains data center dominance and networking scales as guided. Significant upside would come from an accelerated Vera Rubin cycle; downside from a sustained hyperscaler capex reset.

Contact [email protected] for any questions or corrections.