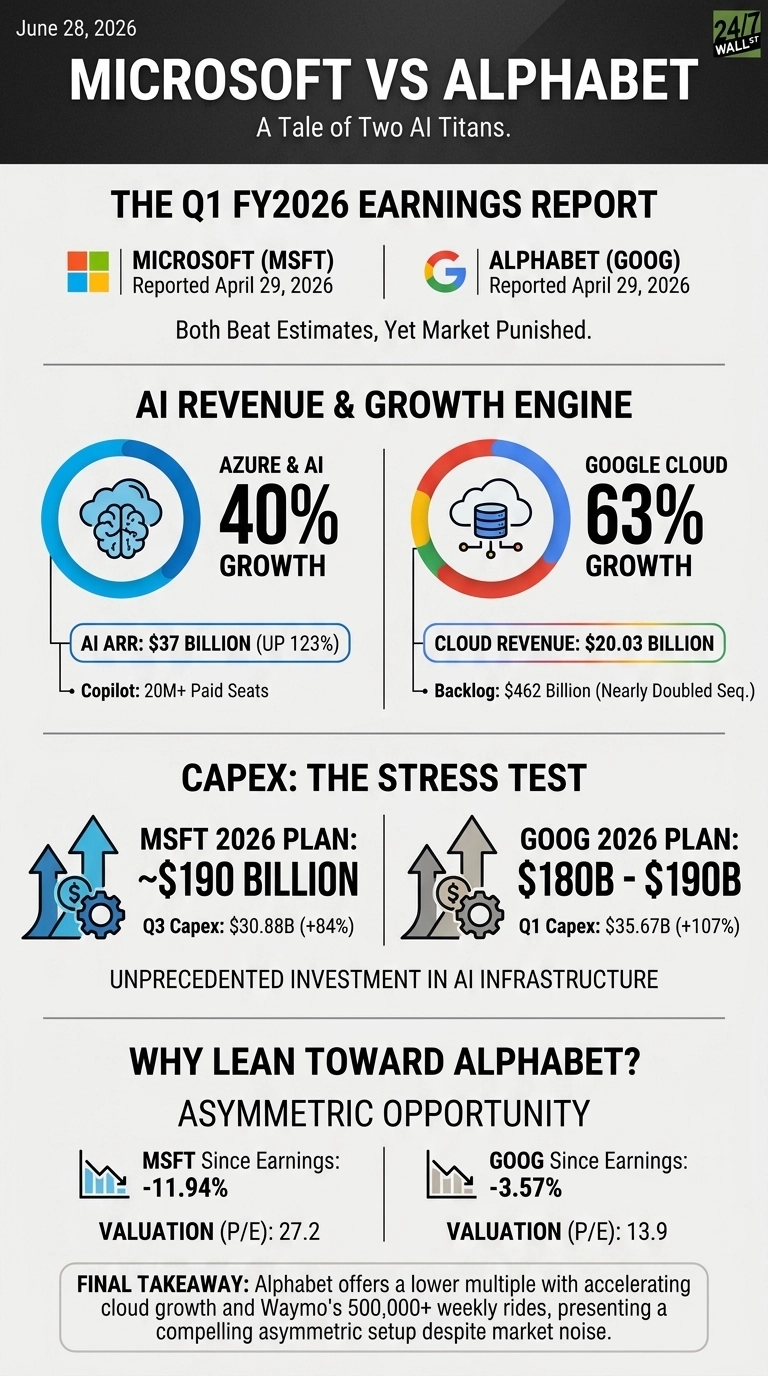

Microsoft (NASDAQ:MSFT | MSFT Price Prediction) and Alphabet (NASDAQ:GOOG) both reported earnings on April 29, 2026. Microsoft leaned on enterprise cloud and Copilot seats. Alphabet leaned on Search resilience and a hyper-growing cloud unit. Both beat estimates. Both are spending unprecedented sums on AI infrastructure. The market has punished both anyway.

Azure Heats Up. Google Cloud Runs Even Hotter.

Microsoft delivered $82.89 billion in revenue, up 18.3%, with EPS of $4.27 against a $4.09 estimate. Intelligent Cloud hit $34.68 billion, with Azure growing 40% in constant currency. That is the engine.

Satya Nadella told investors the AI business now runs at a “$37 billion ARR, up 123%” pace. Microsoft 365 Copilot now sits at over 20 million paid seats, with Accenture alone deploying 740,000 seats. Commercial RPO of $627 billion tells you the backlog is real.

Alphabet was, frankly, louder. Revenue of $109.9 billion grew 21.79%. Reported EPS of $5.11 blew past the $2.63 estimate, but a chunk came from $36.91 billion in unrealized equity gains, so I would not anchor on the headline.

The cleaner story is Google Cloud at $20.03 billion, up 63%, with backlog nearly doubling sequentially to $462 billion. Cloud operating margin expanded to 32.9% from 17.8%. Search held up too at $60.4 billion, up 19%, with queries at all-time highs.

A Partnership Model Versus a Vertical Stack

| Lens | Microsoft | Alphabet |

| Core AI bet | OpenAI partnership plus MAI models | Owns silicon, Gemini, and the stack |

| Cloud growth | 40% (Azure) | 63% (Google Cloud) |

| 2026 capex plan | ~$190 billion | $180B to $190B |

| Valuation (P/E) | 27.2 | 13.9 |

Microsoft pays for IP rights through 2032 and is monetizing through seats that increasingly behave like meters. Nadella was explicit: “The basic transformation of any per-user business of ours…will become a per-user and usage business.”

Alphabet, meanwhile, sells Gemini, TPUs, and BigQuery as one fabric. Sundar Pichai called the company “genuinely differentiated” because of the vertically optimized stack. Enterprise AI Solutions revenue grew nearly 800% year-over-year. That figure is accurate.

Capex Is the Stress Test

Microsoft burned $30.88 billion in capex, up 84.39%, and Amy Hood guided capex over $40 billion next quarter. Alphabet spent $35.67 billion, pushing free cash flow down 46.63% to $10.12 billion.

I will keep an eye on Azure constant-currency growth holding above the 39% to 40% guide and on whether Google Cloud margins can absorb the Wiz integration. The June 23 reports of top AI developers shifting toward Anthropic and OpenAI are worth tracking too.

Why I Lean Toward Alphabet Right Now

Both businesses are excellent. The price tags differ sharply. Since reporting, MSFT is down 11.94%, while GOOG is down just 3.57%.

Alphabet trades at a lower multiple, with cloud accelerating and Waymo doing 500,000+ autonomous rides per week. That is the asymmetric setup I want.

Microsoft remains the steadier compounder, with a fortress backlog and predictable enterprise renewals. For investors sensitive to volatility, capex clarity from both companies remains a key gating factor. I am willing to sit through the noise at Alphabet’s multiple.

Contact [email protected] for any questions or corrections.