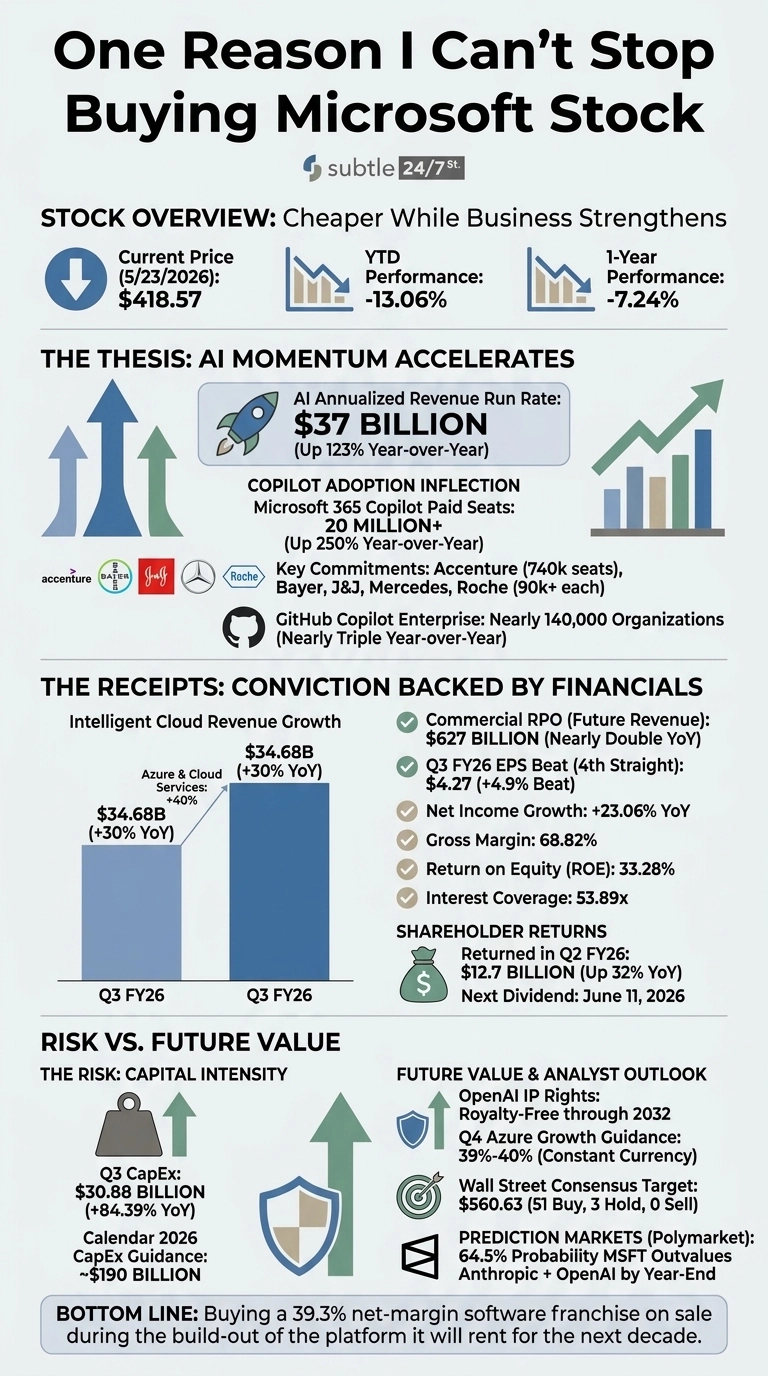

I keep hitting the buy button on Microsoft (NASDAQ:MSFT | MSFT Price Prediction) because the stock has gotten cheaper while the business has gotten stronger. The shares are down 13.06% year to date and down 7.24% over the past year, sitting at $418.57.

Meanwhile, the company just told me its AI business is running at a $37 billion annualized revenue run rate, up 123% year over year. That gap is the trade I am taking, quarter after quarter, with my own money.

The thesis I keep coming back to

Satya Nadella did not bury the lead on the last call. He said, “Our AI business surpassed $37 billion ARR, up 123%.” Then he added that this is “the beginning of one of the most consequential platform shifts” in tech. I can see the receipts inside the same report.

Microsoft 365 Copilot paid seats are now over 20 million, up 250% year over year, with Accenture alone running 740,000 seats and Bayer, Johnson & Johnson, Mercedes, and Roche each committed to 90,000 or more. GitHub Copilot Enterprise is inside nearly 140,000 organizations, almost triple a year ago. This is the install base of the next computing era, and it is paying a subscription.

The receipts behind the conviction

Reason one is the demand pipeline. Commercial remaining performance obligations hit $627 billion, nearly doubling year over year. That is contracted future revenue. Reason two is the engine producing it. Intelligent Cloud revenue rose 30% to $34.68 billion, with Azure and other cloud services up 40%.

Reason three is the quality of the franchise. Q3 FY26 delivered EPS of $4.27 against a $4.07 estimate, a 4.9% beat and the fourth straight, with net income up 23.06% on revenue up 18.3%. That is operating leverage on a company carrying gross margins of 68.82%, return on equity of 33.28%, and interest coverage of 53.89x.

Add the income side. The next dividend is on June 11, 2026, supported by $12.7 billion returned to shareholders in Q2 FY26 alone, up 32% year over year. The forward P/E sits at 22, which I do not consider expensive for a business compounding earnings and contracted backlog at this rate.

The risk I refuse to wave away

The honest threat is capital intensity. Q3 capex was $30.88 billion, up 84.39%, and management guided roughly $190 billion in calendar 2026 capex. If AI demand softens, that bill stings. The OpenAI relationship is also less exclusive than it was, and Microsoft absorbed $3.1 billion in OpenAI investment losses in Q1 FY26.

What keeps the thesis intact is the contracted backlog, the royalty-free OpenAI IP rights through 2032, and the fact that Q4 Azure growth is guided to 39% to 40% in constant currency with capacity still constrained.

Why the buy button stays active

Wall Street’s consensus target sits at $560.63, against 51 buy ratings, 3 holds, and zero sells.

Prediction markets give a 64.5% probability that Microsoft outvalues Anthropic and OpenAI combined by year-end. I am buying a 39.3% net-margin software franchise on sale during the build-out of the platform it will rent for the next decade, and I plan to keep buying until the market figures out which side of that ledger matters.

Contact [email protected] for any questions or corrections.