Broadcom (NASDAQ:AVGO | AVGO Price Prediction) and Microsoft (NASDAQ:MSFT) both delivered AI-fueled quarters revealing two different playbooks. Broadcom sells custom silicon and switches for hyperscaler data centers. Microsoft sells cloud, copilots, and the productivity layer on top. Comparing them shows how the AI buildout splits between picks-and-shovels suppliers and full-stack platform owners.

Custom Silicon Surges While Azure Carries Microsoft

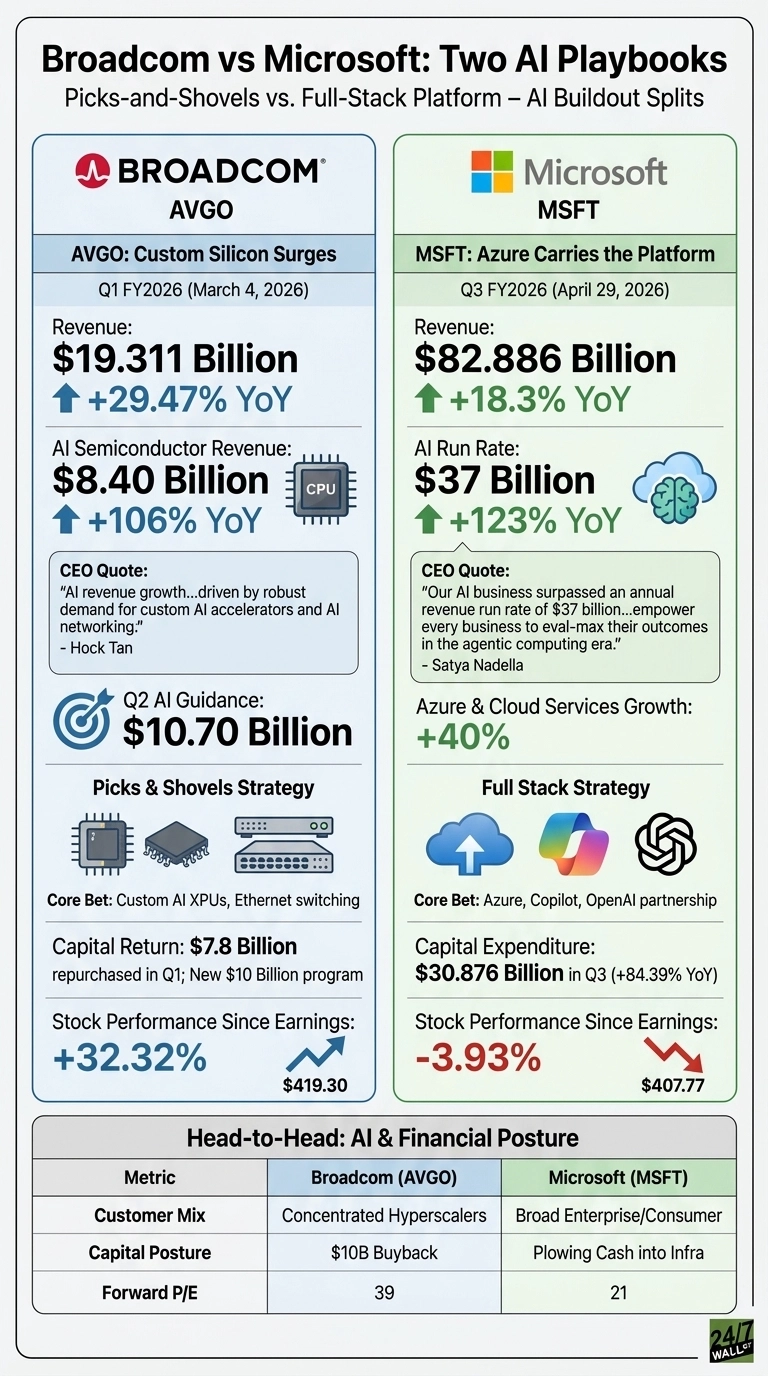

Broadcom’s Q1 FY2026 earnings report landed on March 4, 2026, with revenue of $19.311 billion, up 29.47% year over year. AI semiconductor revenue hit $8.40 billion, growing 106%. CEO Hock Tan called the growth “driven by robust demand for custom AI accelerators and AI networking” and guided Q2 AI revenue to $10.70 billion. VMware kept the software side flat at $6.796 billion, growing just 1%. The chip side is driving results.

Microsoft reported Q3 FY2026 on April 29, 2026 with revenue of $82.886 billion, up 18.3%, and EPS of $4.27. Azure and cloud services grew 40%, and the AI run rate hit $37 billion, up 123%. Commercial RPO of $627 billion nearly doubled, signaling a backlog that extends this cycle. Microsoft spent $30.876 billion in a single quarter, up 84.39%. Some funds are buying Broadcom switches and accelerators.

Picks and Shovels vs. Full Stack

| Lens | Broadcom | Microsoft |

| Core bet | Custom AI XPUs, Ethernet switching | Azure, Copilot, OpenAI partnership |

| Customer mix | Concentrated hyperscalers | Broad enterprise and consumer |

| Capital posture | $10 billion buyback, dividend hike | Plowing cash into infrastructure |

| Forward P/E | 39 | 21 |

Broadcom repurchased $7.8 billion in Q1 alone. Microsoft is funneling cash into capacity the $627 billion RPO suggests is presold. The market has rewarded the capex spender: AVGO is up 32.32% since its earnings report, while MSFT has slipped 3.93%.

The Next Test Is Whether Capex Pays Off

Watch whether Broadcom converts Tan’s $100 billion in AI sales by 2027 ambition into reality, especially after the Google TPU and networking supply agreement through 2031. Keep an eye on Microsoft’s Azure growth rate. If 40% holds while capex moderates, operating leverage flips quickly.

Why I Lean Toward Microsoft for Patient Money

Microsoft’s setup looks more interesting. A forward P/E near 21, an AI book growing 123%, and that monster backlog are not priced like a winner.

Broadcom is the higher-conviction momentum trade at 84 times trailing earnings with concentrated hyperscaler exposure. For torque to the AI buildout, Broadcom delivers it. For a discounted compounder where spending is already contracted, Microsoft is cleaner. I would hesitate on both only if hyperscaler capex rolls over, which I do not see this quarter.

Contact [email protected] for any questions or corrections.