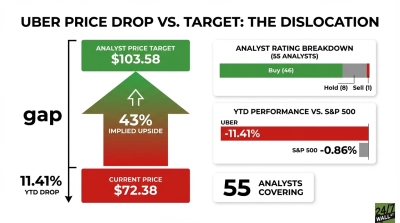

Uber (NYSE:UBER | UBER Price Prediction) has become a growth story firing on every cylinder while its stock quietly bleeds. Gross Bookings hit $53.72 billion in Q1 2026, trips grew 20% year over year, and Uber One crossed 50 million members. Yet shares trade at $72.16, down 22.66% over the past year. Can Uber shares double to $150 by July 2027?

Why Uber Shares Are Stuck Despite Record Bookings

The disconnect between Uber’s fundamentals and stock price is jarring. Year to date, shares are down 11.69%, with a 3.57% one-week bounce doing little to shift momentum. The one-month gain sits at just 2.5%.

Two factors weigh on the stock. First, GAAP earnings have been distorted by a $1.5B pre-tax equity investment revaluation headwind, dragging Q1 net income down 85.19% year over year.

Second, investors worry that Waymo and other robotaxi operators will erode Uber’s market share. With a beta of 1.12, the stock swings harder than the market, and every AV headline has cut against it. Shares sit 2% off the 52-week high of $101.99. The market refuses to credit Uber’s operating engine.

Wall Street Sees 45% Upside. Our Model Says 72%

Wall Street is bullish, but analysts are being too conservative. The consensus target of $104.48 rests on 9 Strong Buys, 36 Buys, 5 Holds, and just 1 Sell, with bullish sentiment at 88%.

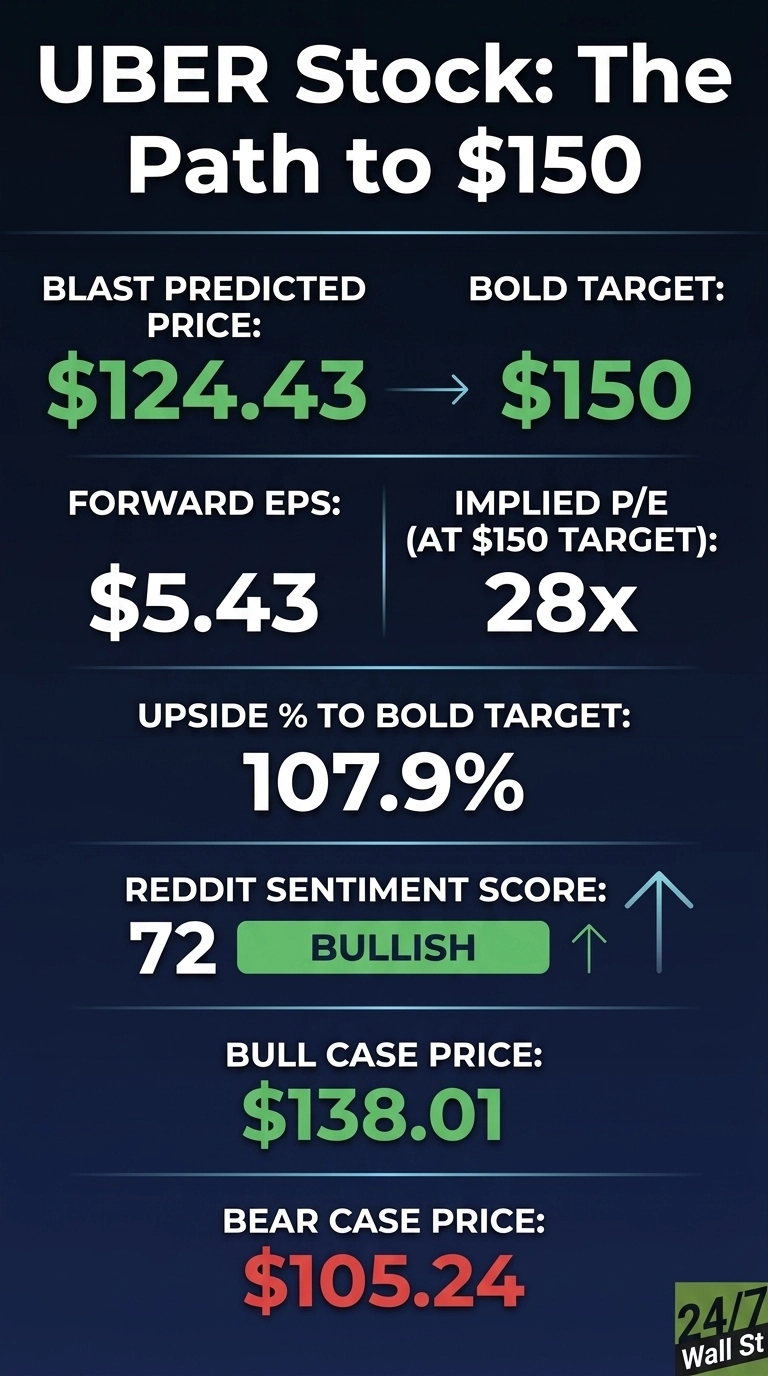

Our base case lands at $124.43, implying 72.44% upside with 90% confidence. The bull case reaches $138.01, the bear case delivers $105.24. Analysts anchor on a bruised trailing multiple, underweighting earnings-growth contribution while overweighting recent GAAP noise. When free cash flow ran at $9.76B for full-year 2025 and buybacks totaled $6.523 billion, a $104 target feels conservative.

The Path to $150 Per Share

Reaching $150 from $72.16 requires a 107.9% gain. This sits above both our base case and bull case, making it a stretch.

With forward EPS of $5.43, a $150 stock price implies a forward P/E of 28x. Our base case of $124.43 implies 14x, meaning the bold target requires roughly 14 turns of additional multiple expansion.

Management is executing key catalysts. CEO Dara Khosrowshahi said “AV Mobility trips grew more than 10x year-on-year” and framed autonomy as “another $1 trillion total addressable market”.

Q2 2026 guidance calls for Non-GAAP EPS of $0.78 to $0.82, up 31% to 38% year over year. If EPS compounds at that rate, the forward multiple compresses even as price rises, making 28x easier to defend. Primary risk: a broad AI-driven tech multiple contraction as flagged in Vanguard’s 2026 outlook.

Where Uber Trades Today vs Its Earnings Power

At $72.16 against forward EPS of $5.43, Uber trades at roughly 13x forward earnings. For a business growing gross bookings 21% and Non-GAAP EPS 44% year over year, that is cheap.

The stock sits near the 52-week low of $67.19 and far below the high of $101.99. Over ten years, UBER is up 73.59%, hardly heroic. The valuation gap is notable for patient long-term holders to monitor.

Is $150 Realistic? My Verdict

Reaching $150 requires a 107.9% gain. It is a stretch.

For it to happen, three things must click: EPS growth must stay in the 30%-plus range through 2027, the AV narrative must flip from threat to tailwind (Waymo, Zoox, and Pony partnerships driving value), and buybacks must shrink the share count aggressively. A recession hitting Mobility volumes before AV economics scale would derail it. We’ve outlined the blueprint for how Uber could reach $150 in 2027.

Contact [email protected] for any questions or corrections.