Of everything Uber (NYSE:UBER | UBER Price Prediction) said in its Q1 report yesterday, the real story is that Uber One has crossed 50 million members, and those members now drive half of Gross Bookings across Mobility and Delivery. That single fact reframes what kind of company Uber is becoming.

Becoming a Membership Business

For years, the bear case on Uber was simple. Rides are transactional. Whoever offers the cheapest fare wins the trip. A membership tier with 50 million paying users looks like a subscription business attached to a global logistics network.

CEO Dara Khosrowshahi framed it directly on the call, calling it “an exciting milestone as we execute against our platform strategy, with members now driving half of our Gross Bookings across Mobility and Delivery.” Read between the lines and you can see the shift. Gross Bookings grew 25% year over year to $53.72 billion while reported revenue rose only 14%, weighed down by business model changes. Underneath, trips climbed 20% and monthly active platform consumers reached 199 million, up 17%. The membership flywheel is doing the heavy lifting.

Why This Reframes the Valuation

Subscription-led platforms get rewarded for predictable revenue and pricing power. Uber is starting to show both. Operating income jumped 57% to $1.923 billion, adjusted EBITDA margin expanded to 5% of Gross Bookings, and the company repurchased $3.011 billion of stock while still generating $2.286 billion in free cash flow.

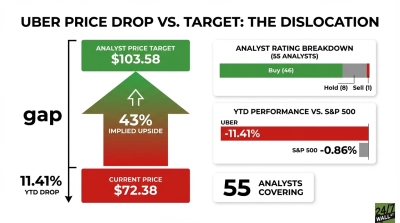

Yet the stock trades at a P/E of roughly 17, with a year-to-date decline of about 3% and a one-year decline near 8%. That is a multiple that prices Uber as a mature gig-economy operator, not a platform compounding members and bookings at this rate. Q2 guidance calls for 31% to 38% non-GAAP EPS growth. That is the disconnect the title points to.

Insiders seem to agree. The CFO bought 22,400 shares at $71.25 in late February, a discretionary purchase outside of any vesting cycle.

The Signal Going Forward

Watch the Uber One member count next quarter, and watch how often management talks about it before the financial metrics. If members keep moving past 50% of bookings, Uber stops being valued like a ride app and starts being valued like the platform it is quietly becoming. That is the one thing to remember from this quarter.

Contact [email protected] for any questions or corrections.