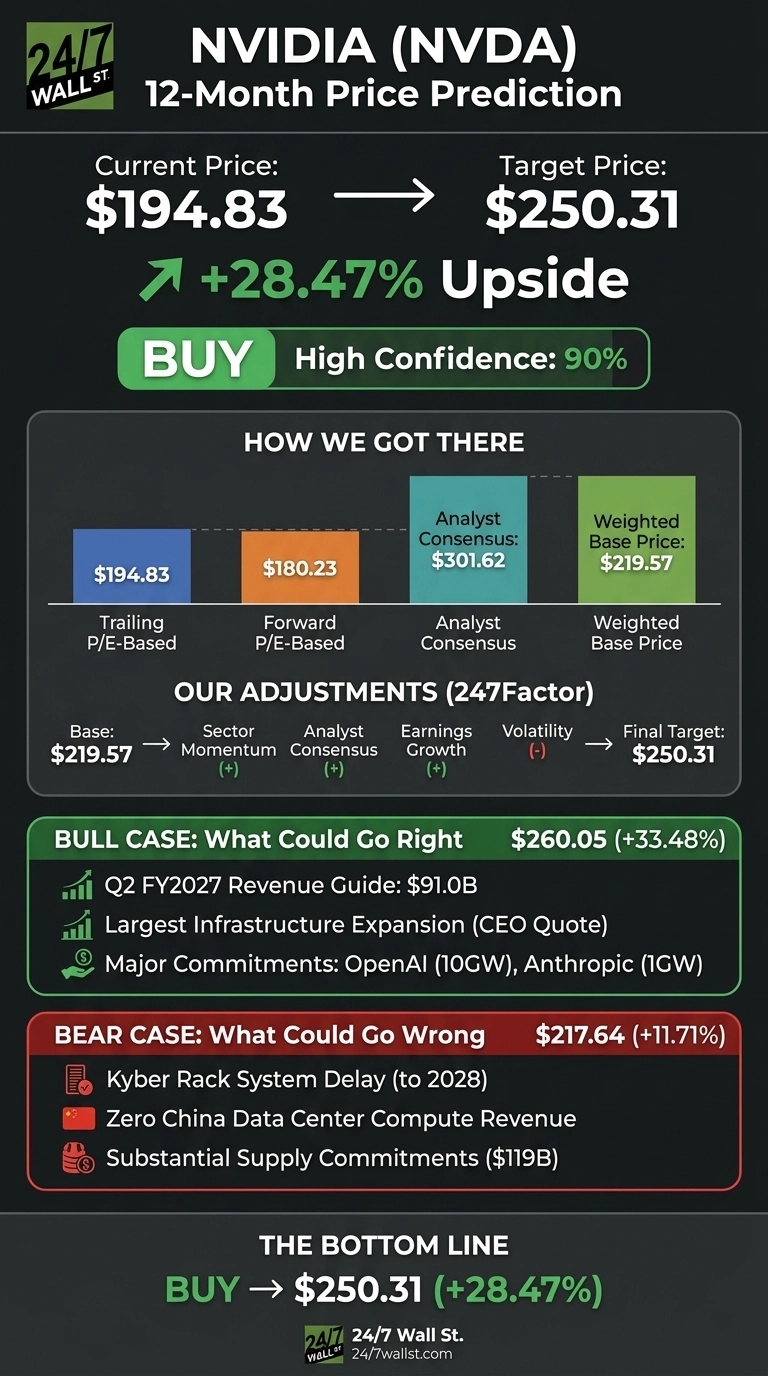

Our NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) call comes at a moment when the stock has cooled off but the underlying business is still accelerating. The 24/7 Wall St. price target for NVIDIA is $250.31 over the next 12 months, implying 28.47% upside from the $194.83 close on July 2, 2026. Our recommendation is buy with a confidence level we characterize as high at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $194.83 |

| 24/7 Wall St. Price Target | $250.31 |

| Upside | 28.47% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Pullback Into Blowout Fundamentals

NVIDIA shares fell 12.46% over the past month and now trade roughly 28% below the 52-week high of $236.26, even as year-to-date performance stays positive at 4.59% and the one-year return sits at 24.06%.

That derating happened despite Q1 FY2027 results (filed May 20, 2026) that beat on both lines: revenue of $81.615 billion grew 85.23% YoY, and non-GAAP EPS of $1.87 topped estimates by 5.42%. Data Center revenue reached $75.246 billion, up 92% YoY, with networking exploding 199%.

Recent news reinforces the demand backdrop: Foxconn reported a 40% quarterly sales increase on AI server strength, and Microsoft made Anthropic’s Claude generally available in Azure Foundry on GB300 Blackwell Ultra GPUs.

The Case for $260 and Higher

The bull scenario in our model targets $260.05, roughly 33.48% above spot. The Street is more aggressive: consensus analyst target sits at $301.62 with 10 Strong Buy and 48 Buy ratings against just 2 Holds and 1 Sell.

Q2 FY2027 guidance calls for revenue of $91 billion with 75% non-GAAP gross margin, and Jensen Huang described the Blackwell and Vera Rubin ramp as “the largest infrastructure expansion in human history”.

Major commitments from OpenAI (10GW), Anthropic (1GW), CoreWeave, and sovereign programs in the UK, Germany, and South Korea add visibility. On 22x forward earnings, the multiple compresses fast if 2027 estimates keep drifting higher.

The Risks Worth Watching

Our bear case lands at $217.64, still positive but far below consensus. CNBC reported on July 5, 2026 that NVIDIA’s Kyber rack system for Rubin Ultra chips has slipped to 2028 due to manufacturing issues, opening a door for AMD and Google. China exposure has effectively gone to zero: guidance excludes any China Data Center compute.

And $119 billion in supply commitments create demand-risk if hyperscaler capex normalizes. Insider activity has skewed toward net selling across 16 recent transactions. That said, bulls would counter that supply commitments reflect confidence in booked orders backed by real demand, and that networking growing at 199% shows full-stack lock-in that is very hard to displace.

The Setup Favors Upside

The 24/7 Wall St. price target of $250.31 and a buy rating reflect a business compounding revenue at 85% while trading at 22x forward earnings, with 90% confidence behind the projection.

The setup looks attractive if the Q2 earnings report confirms $91 billion and Blackwell 300 shipments stay ahead of schedule. The setup weakens if the Kyber delay expands into the base Rubin timeline or if hyperscaler capex guidance turns lower. On today’s setup, the risk skews to the upside.

NVIDIA Price Prediction 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $219.09 |

| 2027 | $267.34 |

| 2028 | $324.66 |

| 2029 | $353.02 |

| 2030 | $389.92 |

These projections assume NVIDIA continues executing on its Blackwell and Vera Rubin roadmap. Meaningful upside or downside could come from Chinese market re-entry, a sharper competitive push from AMD and hyperscaler custom silicon, or a change in AI training capex intensity.

Contact [email protected] for any questions or corrections.