Few small-cap semiconductor names have ridden the AI infrastructure wave as cleanly as Rambus (NASDAQ:RMBS | RMBS Price Prediction). Memory bandwidth is the choke point of AI inference, and Rambus sits directly in that value chain with DDR5 chipsets, HBM controller IP, and next-generation server module solutions. The question now is whether the stock has already priced in the boom.

Our 24/7 Wall St. Price Target for Rambus

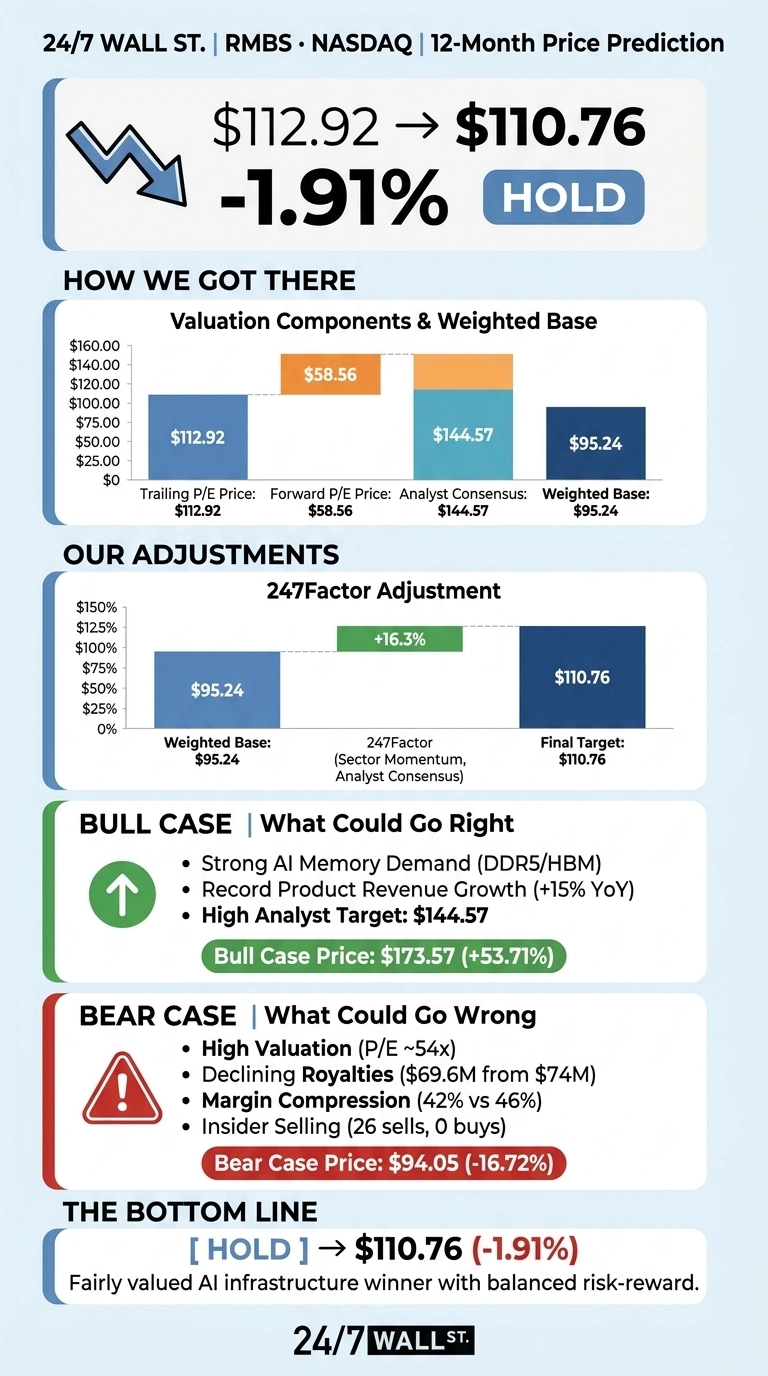

Rambus trades at $112.92 after a 32.29% pullback over the past month. Our 24/7 Wall St. price target for Rambus is $110.76, implying a -1.91% move over the next 12 months. Our model classifies the stock as fairly valued, with 90% confidence. Shares are sitting almost exactly at fair value.

| Metric | Value |

|---|---|

| Current Price | $112.92 |

| 24/7 Wall St. Price Target | $110.76 |

| Upside/Downside | -1.91% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target sits just below where Rambus trades today, and the AI thesis here is real. Product revenue tied to DDR5 and HBM has been the fastest-growing part of the business, and management just launched a DDR5-9600 chipset targeting AI PCs. Consider our target one datapoint. The bull case below outlines why shares could push well past $170.

From $65 to $174 and Back

Rambus has been on a tear, gaining 73.72% over the trailing year and 22.89% year to date, but the stock has cooled. Shares fell 8.71% last week alone and sit 17% below the 52-week high of $174.10.

Q1 FY26 revenue came in at $180.19 million, up 8.1% YoY, narrowly meeting expectations. Non-GAAP EPS of $0.63 came in just under the $0.64 consensus. Product revenue rose 15% YoY on AI server demand, while royalties slipped from $74 million to $69.6 million.

The Case for $173 and Higher

Bulls point to the $144.57 consensus analyst target and a bull-case trajectory that reaches $173.57 by July 2027, a 53.71% return. The engine is memory.

CEO Luc Seraphin said “The growth of AI inference and agentic workloads in the data center continues to drive demand for higher memory bandwidth”. Rambus dominates DDR5 RCDs, is shipping HBM4E controller IP, and just added a DDR5-9600 client chipset for AI PCs. FY2025 revenue rose 27.13% to $707.63 million, and operating income jumped 45.34%.

What Could Go Wrong

The bear case starts with valuation. At a 54 trailing P/E and 17x sales, expectations are elevated. Royalty revenue is shrinking, operating margin compressed to 42% from 46%, and Rambus disclosed a DOJ antitrust subpoena. Insider selling has been consistent, with 26 insider sells and zero buys over the past year.

A DCF from Simply Wall Street pegs fair value at $68.22 to $73.96. Our bear case lands at $94.05. Bulls would counter that rising R&D (up 18% YoY) reflects disciplined investment in HBM4E and SOCAMM2.

Fairly Valued for Now

The 24/7 Wall St. price target of $110.76 reflects a stock priced almost perfectly for its fundamentals. Rambus is a real AI infrastructure winner, but at these multiples the risk-reward is balanced.

I would get more constructive if Q2 FY26 product revenue lands at the top of the $95 to $101 million range and royalties stabilize. I would stay cautious if margin compression continues or the DOJ probe expands.

Extending our model forward, here is where Rambus could trade assuming the current AI memory cycle holds and margins gradually recover.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $110.76 |

| 2027 | $112.45 |

| 2028 | $116.20 |

| 2029 | $119.80 |

| 2030 | $123.39 |

These projections assume Rambus sustains DDR5 and HBM leadership. Meaningful upside or downside could emerge from HBM4E adoption pace, the DOJ investigation outcome, or a broader semiconductor cycle turn.

Contact [email protected] for any questions or corrections.