Netflix reports Q2 2026 earnings after the close on July 16, 2026, and the stock heads into the earnings report at prices most investors never expected to see again.

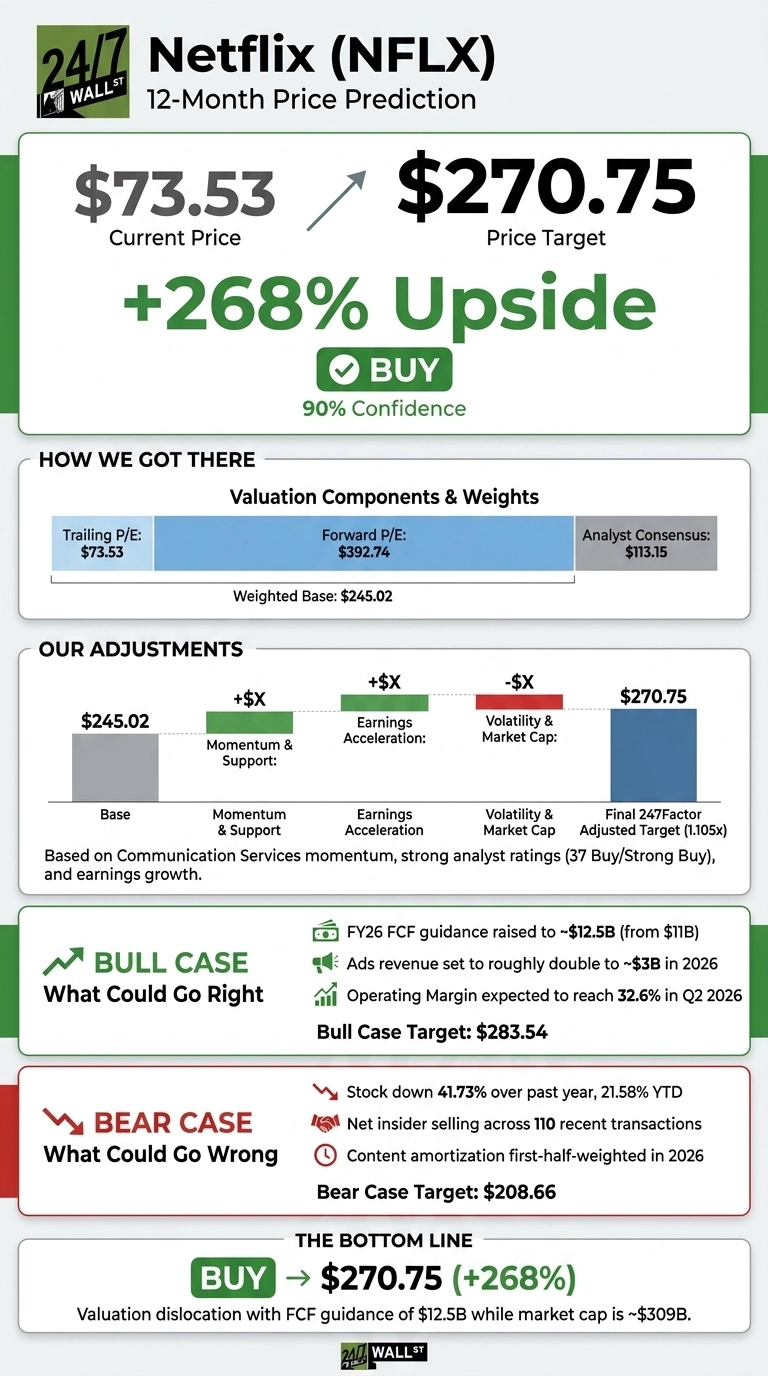

Our 24/7 Wall St. price target for Netflix (NASDAQ:NFLX | NFLX Price Prediction) is $270.75, implying 268.21% upside from $73.53. Our recommendation is buy, at 90% confidence, which is unusually high for our model.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $73.53 |

| 24/7 Wall St. Price Target | $270.75 |

| Upside | 268.21% |

| Recommendation | BUY |

| Confidence Level | 90% |

This aggressive target assumes the market has mispriced a business still growing revenue in the mid-teens with expanding margins.

A Brutal Year for a Growing Business

Netflix shares are down 41.73% over the past year and 21.58% year to date, trading roughly 11% below the 52-week high of $127.75. This drawdown collided with strong operating results.

Q1 2026 revenue of $12.25 billion grew 16.19% year over year, and management raised the 2026 free cash flow outlook to roughly $12.5 billion, up from $11 billion. The reported EPS of $1.23 came in missing expectations by 8.55%, but net income was inflated by a $2.80 billion Warner Bros. termination fee.

The Case for $283 and Higher

Netflix guided FY2026 revenue to $50.7B to $51.7B at a 31.5% operating margin. Advertising is set to roughly double to $3 billion in 2026, with advertiser count up 70% year over year to 4,000+ clients. Live events, gaming, and the content slate (Narcos, Fincher, Gerwig’s Narnia) support continued engagement.

Polymarket traders assign a 72.5% probability to a Q2 earnings beat and 64% to a Q2 operating margin between 32% and 34%. Our bull scenario points to $283.54 in 12 months.

What Could Go Wrong

NFLX has declined 9.89% on average on the day of an earnings miss and 1.58% even on beats. Content amortization is first-half-weighted in 2026, the Brazilian tax dispute carries a $700 million deposit exposure, and the abandoned Warner Bros. deal removes an acceleration lever.

Insider activity shows net selling across 110 recent transactions. Most insider sales are routine 10b5-1 dispositions, and FCF growth of 91.44% in Q1 argues the underlying engine is intact. Our bear case still lands at $208.66, above today’s price.

How Netflix Compares to Disney and Spotify

Walt Disney (NYSE:DIS) is the closest streaming-plus-content comp. Disney trades at a P/E of roughly 13 with an operating margin of 14.6%, versus Netflix at a P/E of 28 and an operating margin of 29.5%. Disney’s Entertainment SVOD segment only just cracked 10.6% margins. Netflix earns nearly triple that on streaming, which supports the premium multiple.

Spotify (NYSE:SPOT) is the direct-to-consumer subscription growth peer. Spotify carries a market cap of $99 billion on 293 million Premium subscribers and 761 million MAUs. Netflix at $309 billion serves 325 million paid subs but monetizes each far better.

On a market-cap-per-paid-sub basis, Spotify commands a higher figure despite lower margins, suggesting Netflix’s target multiple is reasonable.

Netflix vs. Peers

| Company | P/E | Operating Margin |

|---|---|---|

| Netflix | 28 | 29.5% |

| Disney | 13 | 14.6% |

| Spotify | N/A | N/A |

Netflix Price Prediction 2027

The 24/7 Wall St. price target of $270.75 is aggressive, and sell-side consensus of $113.15 implies meaningful upside. The recommendation is buy at 90% confidence.

Raising 2026 FCF guidance to $12.5 billion while the market caps this business at $309 billion is a genuine valuation dislocation. The bull thesis strengthens if Netflix delivers the guided Q2 operating margin of 32.6% and reaffirms ads doubling. The thesis weakens if content amortization compresses margins below 30% and subscriber additions stall.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2027 | $270.75 |

This projection assumes Netflix executes on its ad-tier ramp, expands margins toward 35%, and holds subscriber growth in the mid-single digits. Upside could come from live sports expansion or strategic acquisition. Downside risk centers on content quality deterioration and macro-driven ad softness.

Contact [email protected] for any questions or corrections.