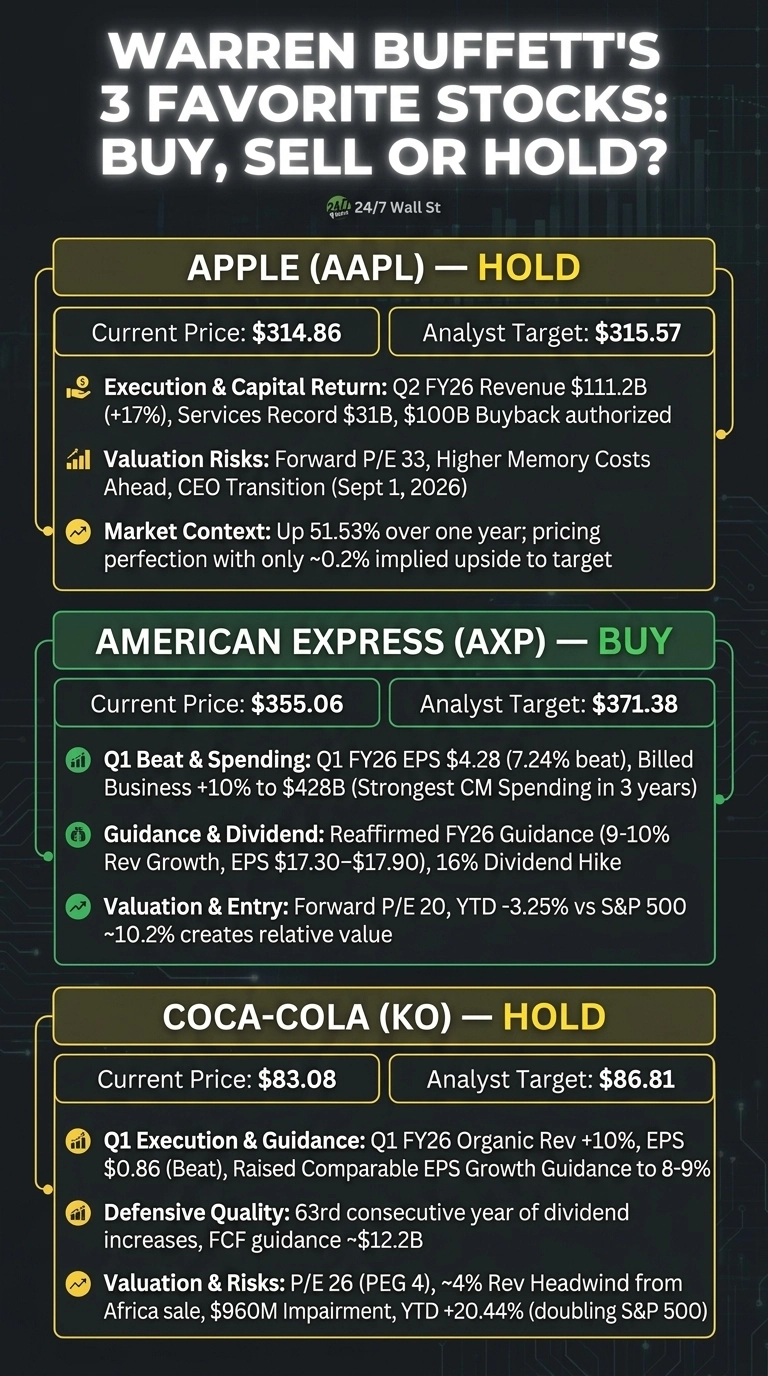

Three of Warren Buffett’s most iconic holdings sit at very different crossroads right now. Apple (NASDAQ:AAPL | AAPL Price Prediction) at $314.86 is a Hold, American Express (NYSE:AXP) at $355.06 is a Buy, and Coca-Cola (NYSE:KO) at $83.08 is a Hold.

Berkshire Hathaway has been reshaping this trio. Apple was trimmed heavily, Coca-Cola was surpassed by Alphabet as the fourth-largest holding, and American Express is closing in on Apple for the top slot. Each stock now has to stand on its own numbers.

Apple: Priced for Flawless Execution

The bull case is executing. Q2 FY26 revenue hit $111.2 billion, up 17%, iPhone revenue climbed 22% to $57 billion, and Services set an all-time record at $31 billion. Greater China grew 28% in the March quarter. The board authorized a fresh $100 billion buyback and raised the dividend 4%. Eight consecutive EPS beats back the momentum.

The bear case is valuation. Shares trade at a trailing PE of 38 and forward PE of 33, richer than the historical average. Tim Cook exits as CEO on September 1, 2026, and management flagged significantly higher memory costs ahead.

Apple is up 16.03% year to date and 51.53% over one year, versus roughly 10.2% for the S&P 500. The analyst target of $315.57 across 47 analysts implies just 0.2% upside. Targets are just one input, and the market is already pricing perfection. The setup argues for patience until a better entry emerges.

American Express: Momentum With Runway Left

AmEx delivered Q1 FY26 revenue of $18.91 billion and EPS of $4.28 versus $3.99 expected, a 7.24% beat. Billed business rose 10% to $428 billion, the strongest Card Member spending in three years. Management reaffirmed FY26 guidance of 9% to 10% revenue growth and EPS of $17.30 to $17.90, and hiked the dividend 16%. The net write-off rate improved to 2%.

Risks include tariff spillover, potential credit card rate caps, and elevated spending on the Platinum refresh. Yet AXP trades at a forward PE of 20 against a $371.38 target from 30 analysts, implying roughly 4.6% upside before dividends.

Shares are down 3.25% year to date while the S&P 500 sits near 10.2%, creating relative-value entry. The 15 Hold ratings represent an upgrade cushion if guidance holds, tilting the setup constructive.

Coca-Cola: Defensive Quality, Capped Upside

The bull case rests on execution. Q1 FY26 organic revenue grew 10%, EPS came in at $0.86 versus $0.81 consensus, and operating margin expanded to 35% from 32.9%. Management raised comparable EPS growth guidance to 8% to 9%. It is the 63rd consecutive year of dividend increases, and free cash flow guidance sits near $12.2 billion.

The bear case is the price. KO trades at a PE of 26 with a PEG of 4, and carries a pending Africa bottling sale worth roughly 4% revenue headwind alongside a $960 million BODYARMOR impairment. Shares are up 20.44% year to date, doubling the S&P 500.

The $86.81 target across 25 analysts leaves only 4.5% implied upside. At $83.08, Coca-Cola is a Hold. Here is why: the defensive earnings quality is real, but the recent run has borrowed forward returns, and the next catalyst worth acting on is either a valuation reset or a clean close to the Africa transaction.

Contact [email protected] for any questions or corrections.