Arm’s ADRs rallied sharply to a 12-month peak in mid-June, then pulled back significantly over the past four weeks. The question for shareholders is whether the pullback is a gift or a warning. Our proprietary model says the former.

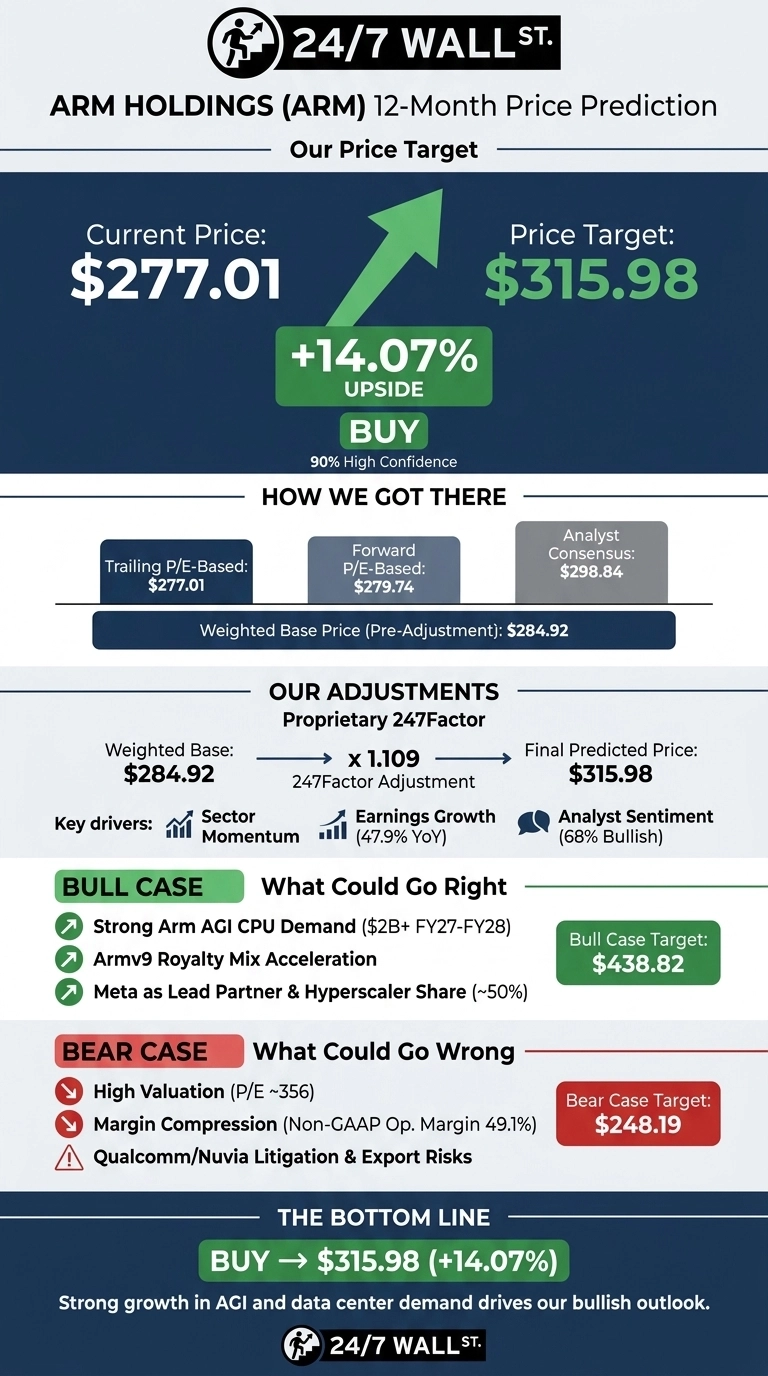

Arm (NASDAQ:ARM | ARM Price Prediction) currently trades at $277.01. Our 24/7 Wall St. price target for Arm is $315.98, implying roughly 14.07% upside over the next 12 months. We rate the stock a buy with a 90% confidence level.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $277.01 |

| 24/7 Wall St. Price Target | $315.98 |

| Upside | 14.07% |

| Recommendation | BUY |

| Confidence Level | 90% |

The Selloff After a Blowout Rally

Arm shares are down 7.74% over the past week and 32.85% over the past month after peaking at $412.55 in mid-June. Year to date, the stock is up 153.42%, and it has gained 88.3% over the past year. The 14-day RSI cooled from overbought readings above 82 in early June to 39.27, signaling exhausted momentum.

The catalyst was a strong fiscal 2026 close. Q4 revenue came in at $1.49 billion, up 20.06%, with non-GAAP EPS of $0.60 beating the $0.5793 consensus. License revenue jumped 29% and data center royalties more than doubled.

Why Bulls See a Path to $438

The bull case centers on Arm becoming the compute backbone of the AI era. Management flagged more than $2 billion in customer demand for Arm AGI CPU across fiscal 2027 and 2028, with Meta as lead partner. Arm holds roughly 50% CPU share at top hyperscalers, and the data center CPU TAM is projected above $100 billion by 2030. Google Axion, NVIDIA Vera, and Microsoft Cobalt all run on Arm.

Full-year FY2026 free cash flow of $882 million, up 395.51%, gives management room to reinvest. Our bull-case scenario sees Arm reaching $438.82 within 12 months if AGI CPU adoption and Armv9 royalty mix accelerate.

What Could Go Wrong

The bear case starts with valuation. Arm trades at a trailing P/E of 356, leaving no margin for error. Non-GAAP operating margin compressed from 52.8% to 49.1% as R&D scaled sharply.

RPO declined 7% year over year, and Polymarket traders assign only a 41% probability that Arm beats its late-July earnings report. The Qualcomm/Nuvia trial in Q4 calendar 2026 and BIS export rules add legal and geopolitical overhangs.

Bulls counter that margin compression reflects deliberate investment in the AGI CPU roadmap. Our bear-case scenario sees a drift to $248.19.

How Arm Compares to Qualcomm and NVIDIA

Qualcomm (NASDAQ:QCOM) is the most direct valuation contrast. QCOM is Arm’s largest licensing customer and the counterparty in the Nuvia litigation. Qualcomm trades at a P/E of 34 with a $187.59B market cap versus Arm’s $300.31B. That gap makes Arm’s multiple look aggressive, but bulls justify it with royalty-model economics QCOM can’t match.

NVIDIA (NASDAQ:NVDA) is the shared-catalyst comp. NVIDIA’s Vera CPU is Arm-based, meaning every Rubin-generation deployment is an Arm royalty event. NVIDIA trades at a P/E of 43 with Q1 FY2027 revenue of $81.61 billion, up 85.2%. Against that AI compute growth scale, Arm’s implied multiples on our target look reasonable.

| Company | P/E | Market Cap |

|---|---|---|

| Arm | 356 | $300B |

| Qualcomm | 34 | $188B |

| NVIDIA | 43 | $5.15T |

Arm Price Prediction 2026-2030

The 24/7 Wall St. price target of $315.98 with 90% confidence signals this pullback is an opportunity. I’d be a buyer here if Arm’s late-July earnings report confirms AGI CPU royalty ramp. I’d stay on the sidelines if margins compress another 300 basis points without a corresponding license bump. On balance, I lean buy.

Our model projects Arm could trade near $429.06 by 2030, with a bull case above $798, assuming current growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $316 |

| 2027 | $346 |

| 2028 | $375 |

| 2029 | $402 |

| 2030 | $429 |

These projections assume Arm continues executing on AGI CPU adoption and Armv9 royalty mix expansion. Significant upside or downside could come from the Qualcomm litigation outcome or a sharper China export regime.

Contact [email protected] for any questions or corrections.