Microsoft (NASDAQ:MSFT | MSFT Price Prediction) has become one of the most closely watched stocks in the S&P 500 as it grinds sideways through a rough first half of 2026. With 54 analysts rating shares Buy or Strong Buy and only three at Hold, sell-side conviction is nearly unanimous. Our proprietary model agrees, but with a more conservative destination than Wall Street’s consensus.

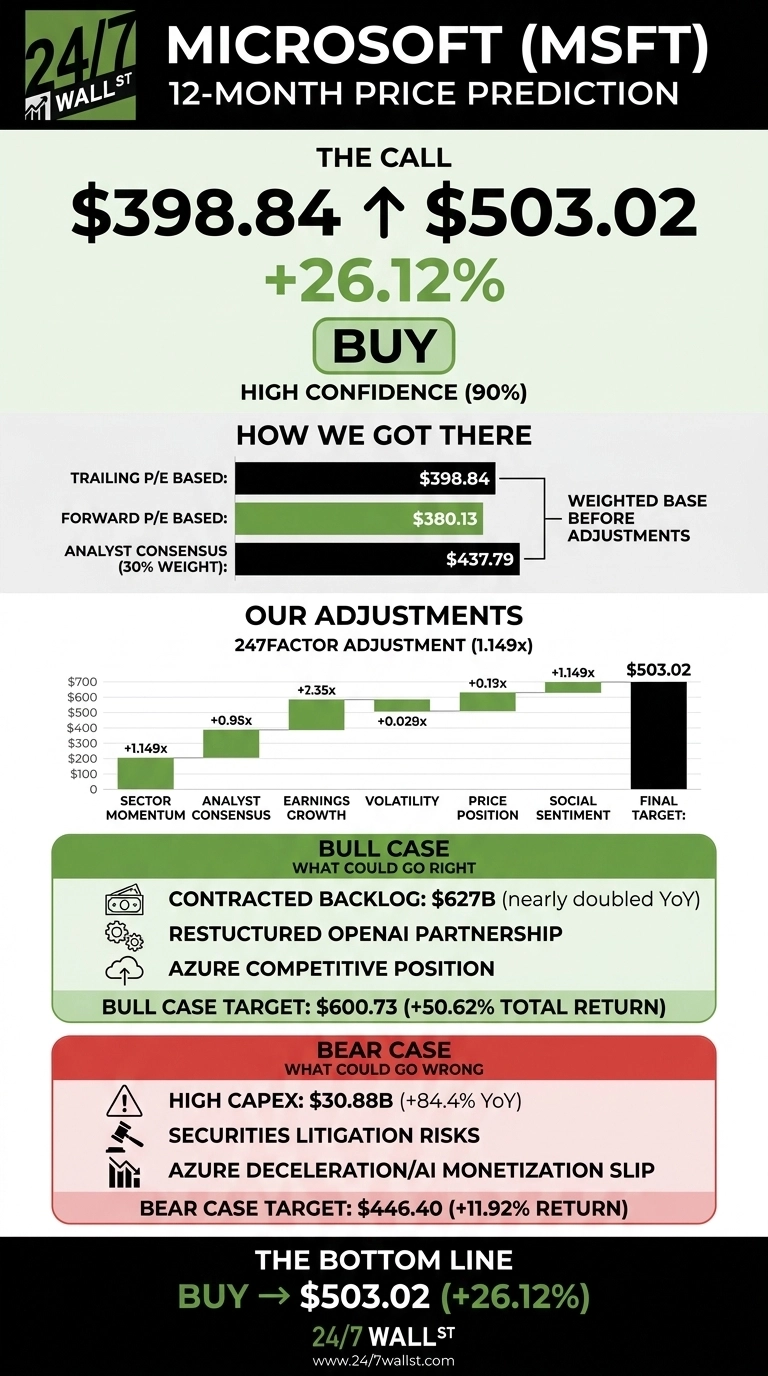

Our 24/7 Wall St. price target for Microsoft is $503.02 over the next 12 months, implying 26.12% upside from the current price of $398.84. We rate MSFT a buy with high confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $398.84 |

| 24/7 Wall St. Price Target | $503.02 |

| Upside | 26.12% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Painful Year Meets a Fortress Business

Microsoft has lagged in 2026. The stock is down 17.83% year to date and 21.16% over the past year, trading 2% below its 52-week high of $551.05 only because it recently bounced 3.21% in the past week off its $349.20 low.

Recent bearish coverage includes securities class action filings alleging misleading statements about Azure growth and Copilot functionality, which have weighed on sentiment ahead of the July 29, 2026 earnings report.

Fundamentals tell a different story. In Q3 FY2026, Microsoft delivered EPS of $4.27 against a $4.07 estimate on revenue of $82.89 billion, up 18.3% year over year.

Azure grew 40%, the AI business hit a $37 billion annualized run rate, up 123%, and commercial remaining performance obligations swelled to $627 billion. This is Microsoft’s fourth consecutive EPS beat.

Why Bulls See a Breakout Ahead

The bull case rests on three pillars: contracted backlog, the restructured OpenAI partnership, and Azure’s competitive position. Commercial RPO of $627 billion nearly doubled year over year gives Microsoft the deepest forward revenue visibility in software.

Microsoft’s IP rights extend through 2032. Azure surpassed Citi Q2 2026 CIO survey identified Microsoft as the top vendor enterprises plan to increase AI spending with, Amazon and Google.

If Azure sustains 40% growth and margins normalize as capex intensity peaks, the bull scenario points to $600.73 within 12 months, a 50.62% total return, aligning with the high end of Street targets.

What Could Go Wrong

Capex is the elephant. Q3 FY2026 capital expenditures reached $30.88 billion, up 84.4%, and full-year FY2025 free cash flow contracted. Bulls counter that this spending backs the $627 billion RPO and a Morgan Stanley projection of nearly 4x hyperscaler compute capacity by 2028.

Two active securities class actions cite these concerns, and analyst target trims have been noted. The bear case lands at $446.40, an 11.92% return, if Azure decelerates and AI monetization slips.

How Microsoft Compares to Alphabet and Amazon

Alphabet (NASDAQ:GOOGL) offers a sharper cloud comparison. Google Cloud has been growing faster than Azure’s 40%, and Alphabet trades at a similar forward multiple, making Microsoft’s premium narrower than it looks.

Amazon (NASDAQ:AMZN) provides counterpoint. AWS continues to trail Azure’s 40% growth but on a larger base. Amazon trades at a richer trailing P/E than Microsoft’s 23. On a growth-adjusted basis, MSFT looks reasonably priced.

| Company | Trailing P/E | Cloud Growth (Latest Q) |

|---|---|---|

| Microsoft | 23 | 40% |

| Alphabet | ~28 | 63% |

| Amazon | 35 | 28% |

The peer group makes our $503 target look conservative. MSFT is the cheapest hyperscaler on trailing earnings while running the second-fastest cloud growth rate.

Our Take on Microsoft Here

The 24/7 Wall St. price target of $503.02 and buy rating reflect our view that the current selloff has overshot fundamentals.

The setup strengthens if Q4 FY2026 earnings on July 29 confirm Azure guidance in the high 30s and show capex intensity beginning to plateau. The thesis weakens if securities litigation gains traction or Azure guides below 35%.

Microsoft Price Projection 2026-2030

Our model projects Microsoft could compound from here at a rate consistent with our five-year base case annualized return of 14.55%.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $503 |

| 2027 | $576 |

| 2028 | $660 |

| 2029 | $756 |

| 2030 | $866 |

These projections assume Microsoft continues executing on Azure and AI monetization. Significant upside could come from faster AI diffusion; downside would follow prolonged capex overhang or material AWS or Google Cloud share gain.

Contact [email protected] for any questions or corrections.