While scrolling through Reddit, I recently came across a post by Amazing_Bobcat8560, who had just hit $5 million in retirement savings. While this was a huge milestone, he is beginning to see that living off of his $5 million is more complicated than he first considered. How can you live off of it without risking depletion?

Having a structured financial plan is vital not only to generate income but also to keep you from running out of money prematurely.

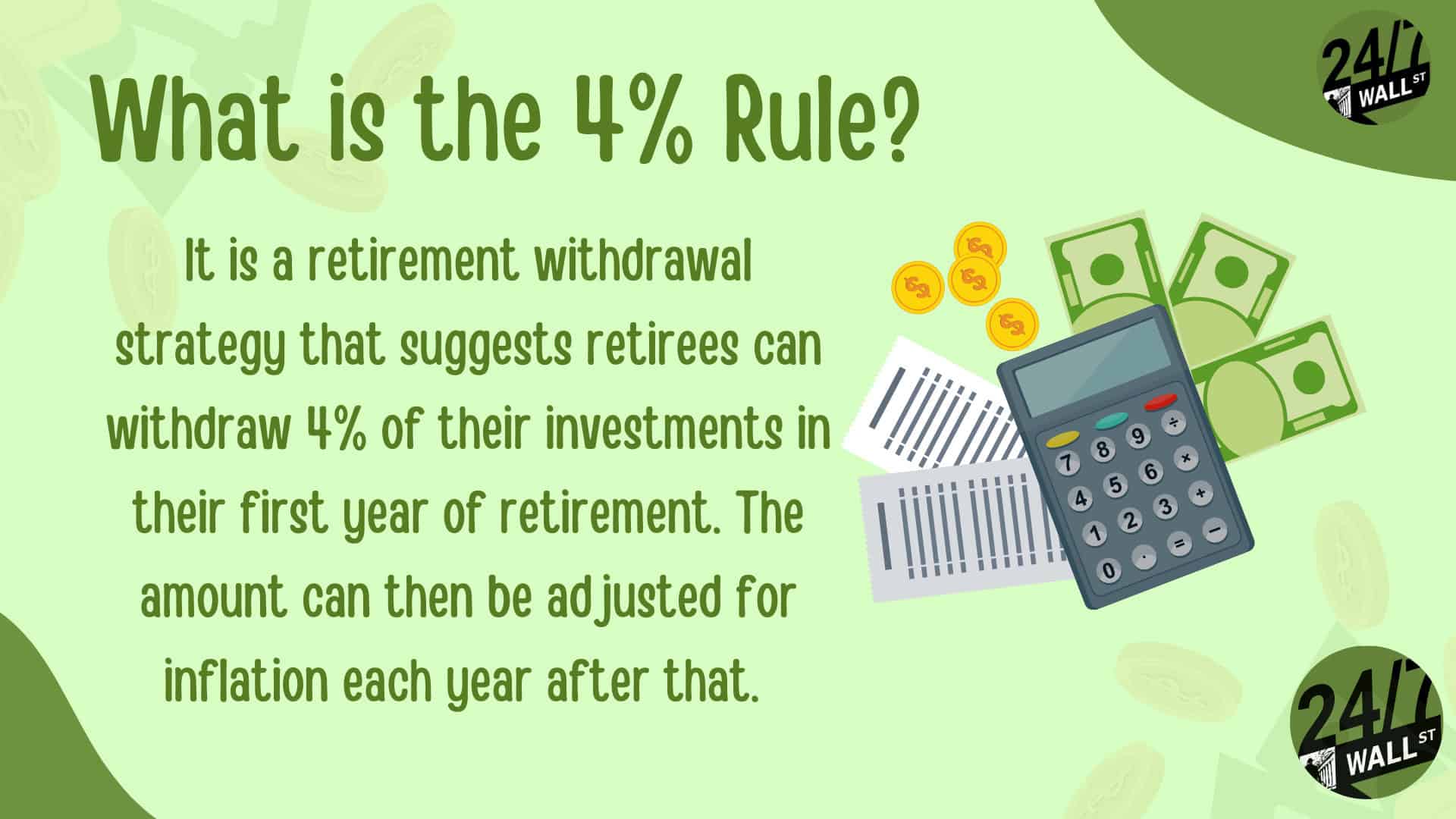

When you hit your financial independence number, it’s important to realize that how you generate your income is just as important as how much you withdraw each year. Our poster did mention the 4% rule, but how you implement that could mean all sorts of things – dividends, capital gains, or a mix of assets.

(That said, the 4% retirement rule may be dead.)

Let’s dive into my recommendations. These thoughts are just my opinion and shouldn’t be considered financial advice:

Key Points from 24/7:

- Diversification & Dynamic Withdrawals

- Avoid Panic Selling

- Tax-Efficiency & Healthcare Planning

Diversification & Dynamic Withdrawals

I would never recommend relying on one income stream. It’s wise to diversify. A balanced approach might look like using dividend-paying stocks while strategically selling equities to capture capital gains.

Rental properties can be another source of passive income, but it’s important to remember that they carry their own risks. You should never try to live solely off of rental income in retirement.

Instead of a rigid 4% withdrawal rate, retirees should also consider dynamic spending strategies like the Guyton-Klinger “guardrails” approach. This involves increasing your withdrawal rate during strong market years and tightening your belt—such as reducing discretionary spending on travel or luxuries—during sustained downturns. This flexibility directly addresses the fear of portfolio depletion.

Avoid Panic Selling

A common mistake that can seriously hurt your wealth is panic selling when the market drops. Yes, you want to avoid losing your hard-earned savings, but it’s important to stick to your investment plan.

A cash buffer of a year or two of living expenses can help keep you from selling off investments at the wrong time. However, instead of leaving this buffer in a standard savings account to lose purchasing power to inflation, consider building a rolling Treasury bill or fixed-income CD ladder. This secures a predictable yield while ensuring liquidity exactly when you need it, heavily mitigating sequence-of-returns risk.

Consider Tax-Efficient Withdrawals

Taxes play a big role in how long your $5M lasts, too. Dividend income can be taxed at a higher rate than capital gains, for instance. You may benefit from a blend of both, but the tax question should drive some of your financial decisions. Beyond simple asset sales, early retirees should look into Roth conversion ladders. The years between retiring and taking Social Security or RMDs are prime time to systematically convert traditional IRA funds to Roth accounts while sitting in a lower tax bracket.

Additionally, managing your Modified Adjusted Gross Income (MAGI) is critical for early retirees who rely on the Affordable Care Act (ACA) for healthcare. Strategically realizing capital gains can keep your MAGI low enough to qualify for ACA subsidies, while simultaneously preventing higher IRMAA surcharges once Medicare kicks in at age 65.

| Taxable Income Range | Income Tax Rate | Long-Term Capital Gains Tax Rate |

|---|---|---|

| $0 to $24,800 | 10% | 0% |

| $24,801 to $100,800 | 12% | 0% (up to $98,900) |

| $100,801 to $211,400 | 22% | 15% |

| $211,401 to $403,550 | 24% | 15% |

| $403,551 to $512,450 | 32% | 15% |

| $512,451 to $768,700 | 35% | 15% (up to $613,700) |

| $768,701 and above | 37% | 20% |

I recommend working with a tax professional to optimize your withdrawals for tax efficiency.

Editor’s Note: This article has been updated to incorporate the 2026 federal income and capital gains tax brackets. The text has also been expanded to detail the Guyton-Klinger guardrails approach for dynamic withdrawals, strategies for Roth conversions and healthcare MAGI management, and the use of Treasury and CD ladders to build yield-generating cash buffers.

Contact [email protected] for any questions or corrections.