The Invesco AI and Next Gen Software ETF (NASDAQ:IGPT) has had the kind of stretch that turns a niche thematic fund into a portfolio anchor: shares are around $100, up roughly 68% year to date and 121% over the past year. The fund tracks the STOXX World AC NexGen Software Development Index, powered by a small cluster of mega-cap names whose earnings essentially are the AI infrastructure cycle. With IGPT now extended after a 31% gain in the past month alone, the question for holders is what specific signal would tell you the engine is shifting gears.

What IGPT actually owns right now

IGPT’s recent performance is a leveraged bet on hyperscaler capex landing in the right places. The fund’s six anchor holdings have each delivered earnings prints that reinforce the AI infrastructure thesis:

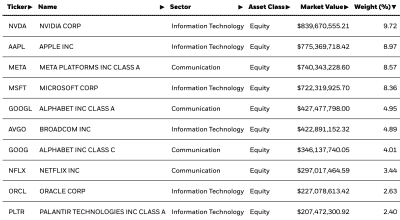

- NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) reported $81.6 billion in Q1 FY27 revenue, up 85% year over year, with data center networking up 199%.

- Microsoft (NASDAQ:MSFT) is running an AI business at a $37 billion annual run rate, up 123% YoY.

- Alphabet (NASDAQ:GOOGL) posted Google Cloud growth of 63% with a $460 billion backlog.

- Amazon (NASDAQ:AMZN) put up 28% AWS growth, its fastest in 15 quarters.

- Meta (NASDAQ:META) raised its 2026 capex guide to $125 to $145 billion.

- Tesla (NASDAQ:TSLA) reported 1.28 million active FSD subscriptions, up 51%.

Those six names plausibly account for the majority of IGPT’s weight.

The macro factor that matters: hyperscaler capex guidance

The single most important variable for IGPT over the next 12 months is the trajectory of hyperscaler capital expenditure guidance. The combined 2026 capex pipeline from Microsoft, Alphabet, Meta, and Amazon is approaching $400 billion, and NVIDIA is sitting on $119 billion in supply commitments that only make sense if those budgets hold.

What to watch is concrete: the FY2027 capex commentary that MSFT, GOOGL, META, and AMZN will deliver on their Q2 2026 earnings calls in late July and early August. Capex guides that flatten or get cut would be the first real evidence that AI infrastructure spend is decelerating. Alphabet’s capex already jumped 107% YoY in Q1, and Microsoft’s 84%. Those growth rates do not need to reverse to hurt IGPT. They just need to slow.

The fund-specific factor: NVIDIA concentration and China revenue

The fund-specific signal that matters most is the path of NVIDIA’s data center revenue, because NVDA is the largest single driver of the index’s recent returns and Jensen Huang’s commentary sets the tone for the rest of the basket. The one figure to monitor is China. NVIDIA reported zero H20 compute revenue from China in Q1, against $4.6 billion in the year-ago quarter, and its Q2 FY27 guide of $91 billion assumes no China data center contribution. Any easing of US export rules would unlock a billions-of-dollars tailwind that flows straight into IGPT’s largest holding.

The transmission to the fund is direct. NVIDIA shares fell about 6% from its May 20 earnings through May 29, even after a beat, on concerns about networking demand sustainability. With NVDA at $211 and a forward P/E near 24, modest disappointment on the next data center earnings report or a worsening of China policy would compress the multiple on the fund’s heaviest weight.

What would change the call

Track the Q2 hyperscaler capex commentary in late July for the macro signal, and NVIDIA’s August data center networking growth rate plus any change to its China assumption for the fund-specific signal. If capex guides hold and NVIDIA’s networking line stays north of triple digits, IGPT’s lead names remain in position. If either cracks, the same concentration that drove the 68% YTD move works the other direction.

Contact [email protected] for any questions or corrections.